Why Businesses Should Integrate AEPS API in 2026

The digital banking industry in India is growing faster than ever, and businesses are constantly looking for better ways to offer secure and convenient financial services. One of the most effective ways to achieve this is by integrate AEPS API. Whether you are a fintech company, retailer, distributor, payment service provider, or digital Aeps banking platform, a top AEPS API Integration can help you expand your services, improve customer satisfaction, and increase business revenue.

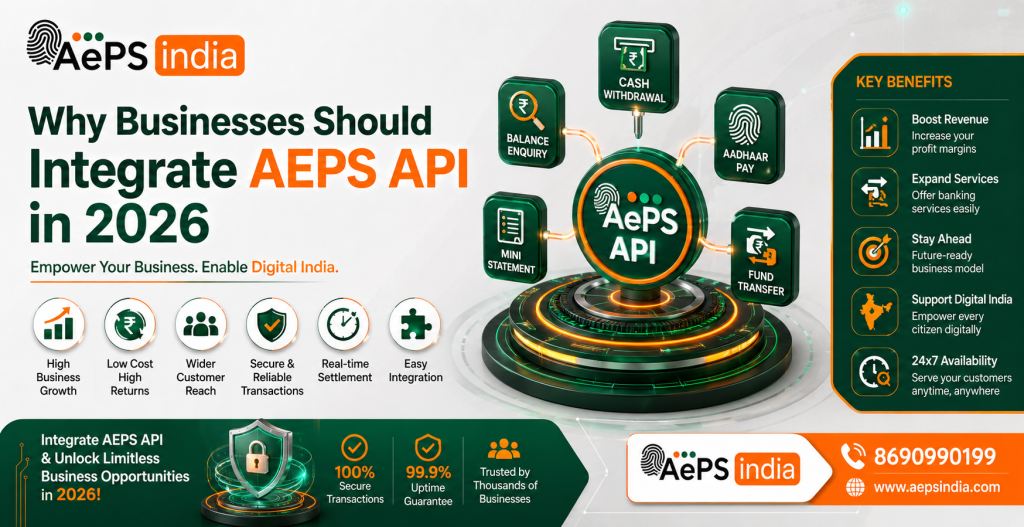

An AEPS API (Aadhaar Enabled Payment System API) allows businesses to provide essential banking services such as cash withdrawal, balance enquiry, mini statement, and Aadhaar Pay API using Aadhaar authentication. Customers can access basic banking services without visiting a bank branch or ATM, making AEPS an important part of India’s digital financial ecosystem.

Integrated AEPS API allows your app or website to offer cardless banking like cash withdrawals, balance inquiries, and mini-statements using only a customer’s Aadhaar number and biometric fingerprint.

The demand for AEPS Services continues to increase because they provide fast, secure, and accessible Aeps banking API solution for customers in urban, semi-urban, and rural areas. By integrating a modern AEPS API Solution, businesses can process transactions in real time, manage retailers and distributors, automate settlements, and deliver a smooth banking experience.

Aeps india one of the AEPS API Provider offers advanced features such as secure biometric authentication, real-time transaction processing, wallet management, commission tracking, retailer management, and easy Aeps API integration. These capabilities help businesses improve operational efficiency, reduce manual work, and support long-term growth.

Aeps india is an reliable AEPS API Provider also helps businesses automate transactions, improve service quality, increase transaction success rates, and generate commission-based income. Secure technology, real-time processing, and seamless integration make AEPS an ideal solution for businesses that want to grow in India’s digital banking and fintech sector.

Aeps India provides a secure and scalable AEPS API Solution designed for retailers, distributors, fintech companies, and digital banking businesses. With top Aeps API integration, advanced management tools, fast transaction processing, and dedicated support, businesses can confidently expand their AEPS services and build a strong digital banking network.

In this guide, you will learn why businesses should integrate an AEPS API, how it works, its key benefits, essential features, and how the right solution can help drive business growth in India’s rapidly evolving digital payments ecosystem.

What is an AEPS API?

An AePS API (Aadhaar Enabled Payment System Application Programming Interface) is a secure Aeps software bridge developed by the Aeps india that allows businesses to integrate biometric-based banking services directly into their Aeps apps or websites. It enables customers to perform transactions using only their Aadhaar number and biometric authentication (fingerprint).

How AEPS API Works

An Best AEPS API allows businesses to integrate cardless, biometric-based banking, such as cash withdrawals and balance inquiries, directly into their Aeps application. By utilizing a 12-digit Aadhaar number and a UIDAI-approved Aeps biometric device, this best Aeps system converts devices into secure, mobile ATMs.

The Step-by-Step Workflow

- Initiation: A customer provides their Aadhaar number and bank details to a merchant for services like cash withdrawals or mini-statements.

- Biometric Capture: The merchant captures the customer’s fingerprint using an approved Aeps biometric scanner.

- Encryption & Transmission: The top AEPS API securely encrypts and sends this data.

- Verification & Processing: The NPCI verifies the identity via UIDAI records, and the bank validates the transaction.

- Settlement & Confirmation: Real-time account updates occur, followed by immediate transaction confirmation.

Services You Can Offer Using an AEPS API

An AEPS admin API enables you to turn any web or Aeps mobile application into a banking kiosk. It uses a customer’s 12-digit Aadhaar number and biometric data to authenticate and process secure financial transactions in real-time. Primary Aeps services you can offer include:

- Cash Withdrawal: Customers can withdraw money directly from their Aadhaar-linked bank accounts using a biometric scanner (fingerprint or iris).

- Balance Inquiry: Allows users to check their real-time bank account balances securely.

- Mini Statements: Fetches the last 5 to 10 recent transactions of the customer’s account for tracking purposes.

- Cash Deposit: Facilitates the direct deposit of cash into an Aadhaar-linked bank account.

- Aadhaar-to-Aadhaar Fund Transfer: Enables seamless money transfers between two bank accounts linked to Aadhaar numbers.

- Aadhaar Pay: Allows merchants to accept cashless, cardless payments directly into their business accounts using biometric authentication.

- eKYC Verification: Provides instant, paperless customer identity verification to help comply with banking and telecom regulations.

Types of AEPS API

An AePS service API empowers developers to integrate cardless, biometric banking into their Aeps application. These smooth Aeps API rely on a customer’s Aadhaar number and fingerprint or iris scan to authenticate transactions directly with their bank.

The primary types of AePS APIs available for integration include:

Core Banking APIs

- Cash Withdrawal API: Allows customers to withdraw money from their Aadhaar-linked bank accounts at agent locations or micro-ATMs using biometric authentication.

- Balance Enquiry API: Enables real-time checking of the available bank account balance via biometric verification.

- Mini Statement API: Fetches a secure summary of the user’s last 5 to 10 bank transactions.

- Cash Deposit API: Facilitates immediate cash deposits directly into a customer’s Aadhaar-linked account.

Specialized & Advanced APIs

- Aadhaar Pay (Merchant Payments) API: A biometric payment method that allows merchants to receive direct payments for goods and services without a debit card or PIN. It is often used for higher transaction limits.

- Fund Transfer API: Allows secure, interbank or intra-bank money transfers between two Aadhaar-linked accounts.

- eKYC/BFD Services API: Facilitates paperless, real-time electronic Know Your Customer verification using “Best Finger Detection” (BFD).

Documents Required for AEPS API

To integrate Aadhaar Enabled Payment System API, you must complete mandatory agent/merchant KYC. Required documents include your PAN card, Aadhaar card (linked to an active mobile number), bank settlement proof (cancelled cheque), and business proof (GST or Udyam registration).

To successfully apply for and set up an low cost AEPS API, you will need to prepare the following documents and fulfill specific requirements:

1. Mandatory KYC Documents

- PAN Card: Required for all financial and tax compliance.

- Aadhaar Card: Must be linked to your mobile number for secure OTP verification.

- Bank Settlement Proof: A cancelled cheque, bank passbook, or bank statement to link your settlement account.

- Passport-sized Photographs: Recent, colored photographs of the operator/director.

- Active Mobile & Email: Must be linked to your Aadhaar for OTPs and notifications.

2. Business & Address Proofs

- Business Registration: Proof such as a GST Certificate, Udyam Registration, or Shop & Establishment Act document.

- Business Address: Utility bill (electricity/water) or a rent/lease agreement not older than 3 months.

3. Technical & Regulatory Requirements

- L1 Certified Biometric Device: You must have a UIDAI and STQC Aeps certified biometric device (e.g., Mantra) to capture fingerprints.

- NPCI Compliance: All systems must adhere to UIDAI guidelines, including strict RSA encryption for data transmission and the “One Operator, One Bank” policy.

Requirements of AEPS API

To integrated Aadhaar Enabled Payment System API, you must comply with strict NPCI and UIDAI guidelines. The requirements are divided into three main categories:

1. Regulatory & Onboarding Requirements

- Agent KYC: Operators must complete full KYC verification (Aadhaar, PAN, and Bank details).

- One Operator, One Bank: Agents are restricted to linking with only one primary acquiring bank for settlements to ensure accountability.

- Re-KYC: Agents face a mandatory re-KYC process if their account is inactive for 3 months.

2. Hardware & Device Requirements

- L1 Biometric Devices: Only STQC-certified L1 Aeps Registered Devices (RD) are permitted (e.g., for fingerprint or iris scans) to ensure secure, end-to-end encrypted capture and liveness detection.

- Connection: A smartphone, tablet, or computer with an active internet connection running Android or Windows.

3. Technical & Security Integration Requirements

- Zero Biometric Data Storage: Aeps API system must never store biometric data (fingerprints/iris) on local servers.

- Encrypted PID Block: Data must be transmitted securely using encrypted PID (Personal Identity) blocks and AES-256/RSA encryption.

- Compliance: The most Aeps API must follow Aadhaar Authentication Application Security Standards (AAASS) and use secure protocols like mTLS/OAuth 2.0.

Top Use Cases of AEPS API

An Modern AEPS API is a secure, biometric-based Aeps banking API solution. It allows customers to access fundamental financial services using only their Aadhaar number and fingerprint, completely bypassing traditional debit cards and PINs.

- Micro-ATMs & Cash Withdrawals: Local retailers and Banking Correspondents (BCs) can use the AEPS Cash Withdrawal API to turn their storefronts into mini-banks, allowing customers to withdraw cash easily without a physical debit card.

- Balance Inquiry & Mini Statements: Customers can instantly verify their linked bank accounts and print or view their recent transaction history using just their biometric input.

- Aadhaar Pay (Merchant Payments): Merchants can use an best Aadhaar Pay API to accept cashless, PIN-less digital payments via customer fingerprint or iris, replacing traditional POS terminals.

- Direct Benefit Transfer (DBT): Streamlines the secure distribution of government subsidies, pensions, and welfare funds directly into beneficiaries’ Aadhaar-linked accounts.

- Electronic KYC (eKYC): Fintechs, banks, and businesses use Aadhaar biometric authentication for instant, paperless, and secure identity verification when Aeps onboarding new customers.

- Aadhaar-to-Aadhaar Transfers: Facilitates direct, secure, instantaneous peer-to-peer money transfers between two individuals using only their Aadhaar numbers and biometric verification.

Key Aspects of AEPS API

An Professional AEPS API is a secure Aeps software interface developed by the Aeps india that allows businesses to embed core banking services like best Aeps cash withdrawal API, Aeps balance inquiry API and Aeps mini statement API into their best Aeps apps or websites. It processes transactions in real-time using only an Aadhaar number and biometric fingerprint authentication.

The essential aspects of an AEPS API include:

1. Core Financial Services

Allows any mobile or web application to function as a micro ATM. Key features include:

- Cash Withdrawal: Users can withdraw money from their Aadhaar-linked bank accounts via retail agents.

- Balance Inquiry: Real-time account balance checks without visiting a physical bank branch.

- Mini Statement: Retrieves the recent transaction history of an account.

- Aadhaar Pay: Enables merchants to accept cashless payments directly from a customer’s Aadhaar-linked account, bypassing standard UPI/card limits.

2. Authentication & Security

Eliminates the need for physical debit cards, PINs, or passwords.

- Biometric Verification: Uses UIDAI-compliant fingerprint or iris scanning for secure, user-friendly authentication.

- Registered Devices (RD): Integrates strictly with UIDAI-approved Aeps biometric devices to ensure secure, end-to-end encrypted data transmission.

3. Architecture & Connectivity

- Interoperability: Allows customers of any bank to transact at any enabled business correspondent (BC) outlet, regardless of where their account is held.

- NPCI Switch: Operates over secure Aeps API provided by the National Payments Corporation of India (NPCI) for seamless, multi-bank routing.

4. Processing & Settlement

- Real-Time Execution: Transactions take only a few seconds to complete with instantaneous success/failure confirmations.

- Instant Settlements: Supports immediate (T+0) or near-instant credit of commissions and funds to the agent’s or merchant’s digital wallet.

5. Regulatory Compliance

- UIDAI / RBI Mandates: Aeps india must rigorously adhere to all security and fraud prevention protocols mandated by regulatory bodies.

- Financial Inclusion: Aeps API Designed specifically to extend essential banking services to underbanked, rural, and non-tech-savvy populations.

Role of Integrate AEPS API

Integrating B2B AEPS API transforms your web, mobile, or POS application into a secure, portable micro ATM device. It allows customers to conduct core banking transactions such as cash withdrawals, balance inquiries, and mini-statements using only their Aadhaar number and fingerprint scan.

Why Integrate an AEPS API?

Integrating Aeps system allows you to build an interoperable bridge between unbanked populations and the formal banking sector.

- Cardless & PIN-less Banking: Removes the need for physical debit cards, making banking accessible for users who may forget PINs or lack traditional cards.

- Financial Inclusion: Expands access to financial services in rural and semi-urban areas by turning standard retail shops into active banking points.

- Enhanced Security: Biometric (fingerprint/iris) authentication significantly reduces the risk of fraud compared to traditional card transactions.

Why It Matters

- Zero Card/PIN Required: Eliminates the necessity for debit cards or passwords; users only need their Aadhaar identity and biometrics.

- Financial Inclusion: Brings essential banking services to rural and underbanked populations who lack traditional ATMs or bank branches nearby.

- Interoperability: Customers can access their accounts from any authorized banking correspondent, regardless of which bank holds their funds.

- Real-Time Settlement: Processes and settles transactions instantly, ensuring immediate confirmation for both the agent and the user.

AEPS API for Retailers and Distributors

An Best Aadhaar Enabled Payment System API allows Aeps platform, distributors, and retailers to integrate secure, biometric-based banking services directly into their apps or websites. Developed by the Aeps india, it transforms ordinary local retail shops into functional “micro ATM software” where customers can handle basic banking needs using only their Aadhaar number and fingerprint verification.

Core Banking Services Provided

Through an AEPS API integrate, retailers can perform real-time interoperable transactions for customers across multiple banks:

- Cash Withdrawal: Securely withdraw funds from an Aadhaar-linked bank account up to ₹10,000 per day.

- Balance Inquiry: Real-time checking of the available bank balance via biometric scanning.

- Mini Statement: Instantly fetch and view summaries of the last 5 to 10 account transactions.

- Aadhaar Pay: Process merchant payments that can bypass regular daily micro-ATM transaction limits.

Retailer vs. Distributor Business Model

The Best AEPS ecosystem operates on a structured, multi-tier hierarchy where participants earn profit-margins on a per-transaction Aeps commission structure.

| Feature / Capability | Retailer (Merchant/Agent) | Distributor (Network Manager) |

|---|---|---|

| Primary Role | Last-mile customer-facing merchant at physical stores (e.g., Kirana shops, pharmacies). | Aeps Onboard, manages, and funds a regional network of individual retail agents. |

| Core Workflow | Collects Aadhaar numbers and scans fingerprints using an L1 biometric device to dispense cash. | Monitors sub-agent volumes, distributes cash floats, and reviews performance analytics via a dedicated dashboard. |

| Hardware Required | Smartphone or PC, internet connection, and an STQC-certified L1 Aeps biometric scanner (e.g., Mantra). | High-end computer or server administration panel; no day-to-day point-of-sale biometric hardware required. |

| Earning Model | Earns a high flat or tiered commission on every single successful withdrawal processed. | Earns an overriding margin or automated “split commission” from every transaction made by their entire retailer base. |

| Average Earnings | Typically scales from ₹10,000 to ₹30,000+ in net monthly profit based on consumer footfall. | Dependent on total network size; handles high transaction volumes across hundreds of active shops. |

Commercials & Setup Costs

Fintech businesses or networks looking to purchase and deploy AEPS technologies experience varying cost structures depending on the integration type:

- Standard API Integration: A one-time Aeps API setup fee ranging from ₹12,000 to ₹35,000 to add banking capabilities into an existing Aeps app.

- White-Label AEPS Portals: Pre-built, fully branded systems allowing customized logos, layouts, and hierarchical management ranging from ₹15,000 to over ₹1.2 Lakh.

- Per-Transaction Commissions: AEPS India offer high Aeps commission payouts, peaking around ₹13 to ₹15+ per transaction on high-value cash withdrawals (typically between ₹3,000 and ₹10,000).

- Settlements: Aeps india extend real-time, automated T+0 or instant wallet-to-bank settlements to keep cash fluid.

How AEPS API Improves Digital Banking Services

An High volume AEPS API allows Aeps fintech apps and best Aeps platform to securely connect with the National Payments Corporation of India (NPCI). It enables customers to perform core banking transactions such as cash withdrawals, balance inquiries, and mini-statements using only their Aadhaar number and biometric verification, without needing a debit card or PIN.

How AEPS API Improves Digital Banking

1. Drives Financial Inclusion

Seamless AEPS API bring essential Aeps banking API services to unbanked and rural populations. By turning local grocery stores and merchant shops into “best Micro ATM device“, customers in remote areas no longer need to travel miles to reach a physical bank branch.

2. Eliminates Cards and PINs

The Aeps API facilitates a cardless and PIN-free banking experience. Users simply provide their Aadhaar number and authenticate the transaction using a Aeps fingerprint scanner. This removes barriers for users who struggle to remember passwords or carry physical cards.

3. Enables Interoperability

An AEPS API integrates with multiple banks, allowing customers to access their accounts regardless of the specific bank the agent is affiliated with. A customer with an account at State Bank of India can use a local retailer’s Aeps india-linked Micro ATM seamlessly.

4. Secures Transactions via Biometrics

By bypassing traditional static passwords, Top AEPS utilizes secure, UIDAI-compliant biometric authentication (fingerprint or iris scanning). This multi-factor verification significantly reduces the risk of fraud and unauthorized account access.

5. Streamlines Government Subsidies (DBT)

The Aeps API create a direct channel for Direct Benefit Transfer (DBT) disbursements. Beneficiaries can instantly withdraw funds (such as welfare payments, pensions, or subsidies) credited by the government directly from their local banking correspondent.

6. Empowers Merchant Payments (Aadhaar Pay)

Beyond basic banking, the Aeps system API enables “Aadhaar Pay,” which allows merchants to accept digital payments from customers directly from their Aadhaar-linked bank accounts. This bypasses standard daily UPI or card limits, making it ideal for high-value rural transactions.

Why AEPS API Is Important for Businesses in 2026

An Instant AEPS API empowers businesses to instantly turn standard devices into “mini-ATMs” by verifying transactions through an individual’s Aadhaar number and biometric scan. It allows companies from rural mom-and-pop shops to large fintechs to offer cardless, pin-less banking like cash withdrawals and balance inquiries directly through their best Aeps application.

The integration is highly important in 2026 for several key reasons:

1. New Revenue Streams via Commissions

For local retailers and fintech agents, AEPS is a major profit driver. By acting as a banking correspondent, businesses earn a direct Aeps commission (typically ₹2 to ₹20+) for every cash withdrawal, balance inquiry, or mini-statement processed.

2. Increased Customer Footfall

Aeps india offering essential banking services at the counter drives heavy foot traffic into retail outlets. In rural or semi-urban areas, this ensures the unbanked and underbanked population visits your store, significantly increasing the cross-selling of your other products and services.

3. Facilitates Government Subsidies (DBT)

With millions of people relying on government schemes, pensions, and subsidies (Direct Benefit Transfer or DBT), having an fast AEPS API ensures your customers can instantly access those funds locally without traveling miles to find a physical bank branch.

4. Reduced Fraud with Biometric Security

Compared to traditional card-based transactions that can be compromised via stolen passwords or skimming, real time AEPS API use real-time biometric (fingerprint or iris) matching against UIDAI records. Integrating mandatory Level 1 (L1) Registered Devices ensures secure, “live” liveness detection to thwart fraud.

5. Cost-Effective, Scalable Infrastructure

Businesses avoid the prohibitive costs of setting up traditional brick-and-mortar branches or physical ATM networks. Aeps API architecture mean you can easily plug microservices into existing mobile Aeps apps, web dashboards, or kiosks, instantly scaling access to anyone with an Aadhaar-linked bank account.

Key Things to Consider for Integration

If you are planning to integrating AEPS API into your business, here is how the top approaches compare:

| Approach | Best For | Pros | Cons |

|---|---|---|---|

| White-Label AEPS Portal | Small Retailers / Agents | Ready-to-use, quick setup, minimal technical knowledge needed. | Less control over branding, higher dependency on the parent provider. |

| Direct API Integration | Established Fintechs / Large Platforms | Deep customization, total brand ownership, scalable backend. | Demands rigorous technical development, complex compliance, and NPCI audits. |

Features AEPS API

An Highest AEPS API empowers businesses to integrate core banking and financial inclusion best Aeps services into their Aeps admin platform. It utilizes Aadhaar-linked biometric authentication (fingerprint or iris scan) to allow users to perform cardless and PIN-less transactions directly from their bank accounts.

Core Banking Services

- Cash Withdrawal: Allows customers to withdraw cash from their Aadhaar-linked bank accounts at registered Business Correspondent (BC) or micro-ATM outlets.

- Balance Inquiry: Provides real-time account balance checks instantly using the Aadhaar number and biometric verification.

- Mini Statement: Retrieves recent transaction history for any Aadhaar-linked account.

- Cash Deposit & Fund Transfers: Enables users to deposit cash or transfer money directly between Aadhaar-linked accounts.

Security & Authentication

- Biometric Authentication: Uses secure, UIDAI-compliant fingerprint or iris scanning for identity verification.

- Interoperability: Customers can access their bank accounts from any registered outlet, regardless of where their account is held.

- High Security & Encryption: Protects sensitive user data during transit and authentication using standard encryption protocols.

Business & Integration Features

- Aadhaar Pay (Merchant Payments): Enables merchants to accept cashless payments directly from a customer’s bank account using their Aadhaar number and biometrics.

- Real-Time Processing: Delivers instantaneous transaction confirmation (typically within 2-3 seconds) through the NPCI (National Payments Corporation of India) network.

- Instant Settlement (T+0): Immediately credits funds to the merchant’s wallet, ensuring quick access to capital.

- White-Labeling: Aeps india offers customizable Aeps API and Aeps admin panel that seamlessly integrate into Aeps B2B apps, Aeps retail software, or mobile Aeps application.

Benefits AEPS API

An AEPS business API allows businesses to integrate secure, cardless, and PIN-less banking services like cash withdrawals, balance inquiries, and mini-statements using only a customer’s Aadhaar number and biometric authentication.

Integrating an AEPS API provides crucial advantages categorized by the target user:

For End-Users & Customers

- Cardless & PIN-less Banking: Customers do not need to carry physical debit cards or remember secure PINs. Transactions require only their Aadhaar number and a fingerprint scan.

- Hyper-Local Accessibility: Transforms local grocery shops, pharmacies, and general stores into functional “micro-ATMs,” saving users from traveling long distances to a physical bank branch.

- Interoperability: Customers can perform transactions using any Aadhaar-linked bank account at any AEPS-enabled terminal, regardless of which bank they belong to.

- Easy Access to Government Funds: Provides a streamlined way for beneficiaries to instantly withdraw Direct Benefit Transfers (DBTs), pensions, and welfare payments.

For Businesses & Agents

- New Revenue Streams: Agents and merchants can earn attractive per-transaction commissions, turning spare cash-in-hand into profit.

- Increased Customer Footfall: Aeps india offering basic banking services brings more people into local stores, which organically boosts sales for the primary retail business.

- High Security & Fraud Reduction: Biometric authentication ensures that only the actual account holder can access the funds, significantly reducing the risk of unauthorized transactions compared to traditional PIN systems.

- Seamless Scalability: New Aeps API use simple JSON/XML formats that embed easily into existing websites or mobile Aeps admin application. They offer instant settlement and high success rates exceeding 98%.

Easy AEPS API Integration Process

Integrating Aadhaar-Enabled Payment System API involves choosing a certified Aeps india, completing mandatory KYC, and connecting your system’s backend with the Aeps API endpoints (JSON/XML) to securely process real-time biometric transactions like cash withdrawals and balance inquiries.

The integration process follows a streamlined, secure workflow:

1. Aeps india Selection and Onboarding

- Choose a Partner: Select an NPCI-certified Aeps india.

- Registration & KYC: Complete your business KYC. You will typically need to submit your Business PAN, Aadhaar, company bank account details, and incorporation proof.

- Credentials: Upon approval, you will receive your BEST Aeps API keys, Aeps Merchant ID (MID), and comprehensive technical Aeps API documentation.

2. Biometric Hardware Setup

- Device Procurement: Purchase Aeps L1 biometric fingerprint scanner (e.g., Mantra).

- RD Service Setup: You must install the hardware manufacturer’s Registered Device (RD) service software. This ensures that the user’s biometric capture is securely encrypted before being transmitted.

3. Technical Integration & Development

- Frontend Design: Build your user interface to capture the customer’s Aadhaar number, bank name (or IIN code), and transaction type (Withdrawal/Balance/Mini-Statement). You must configure the frontend to trigger the biometric scan via the RD service.

- Backend Implementation: Connect your server using the AEPS API Services endpoints (JSON/XML). You will need to implement end-to-end encryption (e.g., AES-256) for the biometric PID block.

- Callback URL: Set up a secure HTTPS callback URL to receive real-time transaction success or failure statuses from the NPCI switch.

4. Sandbox Testing

- Test Environment: Before going Aeps API live, process dummy transactions in your Aeps india sandbox/staging environment.

- Verify Responses: Test all use cases, including successful withdrawals, incorrect fingerprints, and server timeouts, to ensure trusted Aeps system handles Aeps API responses correctly.

5. Go Live

- IP Whitelisting: Once testing is successful, the Aeps india will request your static server IP to whitelist it for production.

- Production Deployment: Swap your sandbox keys with live Aeps API production keys and deploy your updated web or best Aeps software.

AEPS API Integration Cost Structure

AEPS API integration cost generally include one-time Aeps setup fees ranging from ₹12,000 to ₹35,000, and annual maintenance charges (AMC) of ₹10,000 to ₹40,000. White label Aeps portal cost between ₹15,000 and ₹1.2 Lakhs, while direct Aeps bank API can cost up to ₹4.5 Lakhs.

1. One-Time Integration & Software Costs

- Standard Aeps API Integration: ₹12,000 to ₹35,000 for integrating endpoints into an existing Aeps admin software or website.

- White Label Aeps Portal: ₹15,000 to ₹1.2 Lakhs for a ready-made, fully branded Aeps admin portal (allowing you to create sub-distributors and retailers).

- Direct Bank API: ₹2.5 Lakhs to ₹4.5 Lakhs for direct enterprise-level tie-ups with banks like ICICI or Yes Bank.

2. Annual Maintenance Charges (AMC)

- Ongoing technical support, security patches, and server hosting generally cost between ₹9,999 and ₹40,000+ per year, depending on the Aeps india and transaction volume.

3. Transaction Charges & Commissions

Pricing models vary by Aeps india, falling into two primary structures:

- Per-Transaction Fee: Providers charge a flat fee per cash withdrawal (₹0.50 – ₹1.50).

- Commission Sharing: Retailers/agents earn Aeps commission of 0.5% to 1% (or up to ₹15 per successful transaction depending on the slab).

4. Hardware Requirements

- Biometric Devices: L1 Aeps certified fingerprint scanners (e.g., Mantra) cost roughly ₹1,500 – ₹3,000 per unit.

- Micro ATMs: If your service includes card-swiping, these micro atm machines cost ₹10,000 – ₹15,000+.

Aeps API Commission Structure

An Aadhaar Enabled Payment System service API commission structure is a tiered, slab-based model. Retailers and agents typically earn between ₹2 to ₹15+ per transaction, with the highest payouts on withdrawals between ₹3,000 and ₹10,000.

Typical Retailer Commission Slab

Highest Aeps Commissions scale directly with the amount withdrawn or processed:

| Transaction Slab | Approximate Commission to Retailer |

|---|---|

| ₹100 – ₹999 | ₹2.00 |

| ₹1,000 – ₹1,499 | ₹3.00 |

| ₹1,500 – ₹1,999 | ₹4.50 |

| ₹2,000 – ₹2,499 | ₹5.50 |

| ₹2,500 – ₹2,999 | ₹5.00 – ₹7.00 |

| ₹3,000 – ₹10,000 | Up to ₹13.00 – ₹15.00+ |

Non-Withdrawal Services

- Balance Inquiry: ₹1.00 to ₹5.00

- Mini-Statement: ₹1.00 to ₹7.00

- Aadhaar Pay: Up to 1% commission on high-value transactions (up to ₹50,000).

B2B Hierarchy & Commission Splits

If you are integrating a B2B AEPS API, commissions are typically distributed across a multi-level hierarchy (Admin → Master Distributor → Distributor → Retailer). The exact commission credited to the bottom-tier retailer depends on the margins set by the Aeps india.

Settlement Types

- T+0 (Instant) Settlement: You receive the Higher Aeps commission and withdrawn funds in your settlement account immediately. This often attracts a small transfer fee/charge.

- T+1 (Next Day) Settlement: Settled the following business day, usually at zero extra cost.

How AEPS API Helps Increase Business Revenue

An faster AEPS API allows businesses to transform standard retail locations or digital apps into “mini-banks”. By processing transactions using just an Aadhaar number and biometrics, it drives revenue by generating direct commissions and boosting in-store footfall.

How an AEPS API Generates and Grows Revenue

- Direct Transaction Commissions: Businesses and agents earn a tiered Top Aeps commission (typically ₹2 to ₹15+) for every successful cash withdrawal, balance inquiry, or mini-statement processed. Higher withdrawal amounts usually yield higher Aeps commissions.

- Increased Store Footfall & Cross-Selling: Operating as a local micro ATM service brings customers directly into your storefront. This spike in foot traffic directly leads to increased sales for your primary retail or top Aeps service offerings.

- Expanded Customer Base: Branded AEPS connects you with unbanked or underbanked rural populations who lack physical debit cards or access to distant bank branches, opening up a massive demographic.

- Interoperable Revenue Streams: Because the Best Aeps system is interoperable, you can serve customers holding accounts with any Aadhaar-linked bank in the country, broadening your potential client base.

- Improved Cash Flow & Liquidity: Aeps india offer real-time or same-day (T+0) settlements, ensuring your working capital remains consistent and available.

Core Dimensions to Consider

| Dimension | AEPS API Approach | Traditional Banking Approach |

|---|---|---|

| Authentication | Biometric (fingerprint/iris scan) | Card and PIN required |

| Setup & Cost | Low investment (requires only a smartphone/POS and biometric scanner) | High infrastructure costs (ATM machines, branch building) |

| Target Market | Unbanked/rural sectors, highly accessible | Urban-centric, requires travel |

How AEPS API Helps Increase Customer Footfall and Revenue

Integration Aadhaar Enabled Payment System API transforms a standard storefront into a localized “mini-ATM” or banking point. This allows businesses to attract more local foot traffic and generate direct income through transaction commissions without heavy infrastructure investments.

How AEPS API Drives Customer Footfall

- Turns Shops into Banking Hubs: By offering essential services like cash withdrawals, balance inquiries, and mini-statements directly in local neighborhoods, retailers attract individuals who would otherwise have to travel long distances to reach a physical bank branch.

- Boosts Cross-Selling Opportunities: Increased foot traffic means more eyes on your primary inventory. Data shows that providing micro-banking services directly results in up to 20% higher sales of daily retail, telecom, or utility products.

- Wider Demographic Reach: The branded Aeps API allows you to serve rural, semi-urban, and unbanked populations that rely purely on Aadhaar biometrics for their financial needs, significantly expanding your regional customer base.

How AEPS API Increases Revenue

- Transaction Commissions: You earn a direct, attractive Aeps commission for every successful transaction (often up to ₹10–₹15 per high-value withdrawal) processed through most Aeps system.

- Low Operational Costs: Becoming an Aeps india requires minimal investment usually just a smartphone and a low-cost, registered biometric device.

- Instant Liquidity: Modern Aeps API feature instantaneous or same-day (T+0) settlement of funds. This rapid capital rotation keeps your working capital flowing smoothly, allowing you to sustain high-volume transactions daily.

- Aadhaar Pay Options: Businesses can accept customer payments for retail goods simply through biometric authentication, which is secure, cardless, and eligible for merchant commissions on higher-ticket sales.

Security Features of a Reliable AEPS API

A reliable Aadhaar Enabled Payment System API must utilize end-to-end encryption (like AES-256) for data in transit, mandate L1 Aeps certified biometric devices, and ensure strict adherence to NPCI guidelines (such as encrypted PID blocks and no local storage of biometric data) to prevent fraud.

The following features are vital for maintaining a secure, compliant, and fraud-resistant AEPS infrastructure:

Core Security Features

- Encrypted PID Blocks: The Digital Aeps API must accept only encrypted Personal Identity Data (PID) blocks from registered devices. It should process this data strictly through secure server-to-server communication without allowing any raw biometric traces to be exposed.

- Mandatory L1 Biometric Devices: Ensures that the online Aeps API integrate exclusively with STQC-certified, UIDAI-registered Level 1 (L1) biometric devices to eliminate spoofing and fingerprint replication.

- End-to-End (E2E) Encryption: Secures the entire payload (Aadhaar number, PID block, and bank details) from the point of capture on the client application up to the host banking server.

- Real-Time AI Fraud Detection: Analyzes behavioral patterns, velocity checks, and geolocation tracking to flag unauthorized access, velocity abuse, or duplicate transaction attempts.

- Two-Factor Authentication (2FA): Secures the agent or merchant portal by requiring multi-factor authentication (e.g., agent biometric login + OTP) before any transaction session can be initiated.

Regulatory & Compliance Pillars

- NPCI & UIDAI Guidelines: The online Aeps API must enforce current NPCI mandates, including the “One Operator, One Bank” mapping policy and strict adherence to agent KYC protocols.

- No Raw Data Storage: A High sucess Aeps API strictly forbids caching or saving user biometric data (fingerprint or iris scans) in local device memory or server databases.

- Data Localization: Guarantees all sensitive financial and Aadhaar-linked data remains stored on servers physically located within India, in compliance with RBI data protection frameworks.

System Reliability & Integrity

- Multi-Bank Failover: Ensures high availability by dynamically routing failed or timeout-prone requests to secondary banking switches to maintain over 98% transaction success rates.

- Tamper-Proof Audit Trails: Logs every request and response, including terminal IDs and device serial numbers, to create non-repudiation records for regulatory audits and dispute resolutions.

- Consent Management: Explicitly captures user consent for processing Aadhaar authentication, usually integrated into the agent workflow, leaving a digital footprint for every query.

Real-Time Banking Transactions with AEPS API

An multi service AEPS API empowers developers to embed real-time, cardless banking such as cash withdrawals, balance inquiries, and mini-statements into Aeps b2b application. It relies on a customer’s 12-digit Aadhaar number and biometric authentication (fingerprint or iris scan) to securely connect with the NPCI (National Payments Corporation of India).

Key Features of AEPS API

- Interoperable Access: Customers can securely access their Aadhaar-linked bank accounts through any registered agent or retail outlet, regardless of their home bank.

- Real-Time Processing: Transactions are usually processed within 2-3 seconds, with instant (T+0) settlement of funds directly into the merchant’s or agent’s business wallet.

- Security & Compliance: Transactions bypass physical debit cards and PINs, relying on UIDAI-verified biometric authentication and fully encrypted data.

- Financial Inclusion: A highly accessible solution for rural and unbanked populations that lack access to physical ATMs or smartphones.

Technical Requirements for Integration

To successfully deploy AEPS API, your top Aeps application must meet several critical prerequisites:

- STQC-Certified Biometric Devices: You need compliant fingerprint or iris scanners (registered with Registered Device (RD) services) to securely capture customer biometrics.

- API Developer Stack: Integration is typically achieved using lightweight formats like JSON or XML via RESTful Aeps API.

- Regulatory Compliance: Your business must comply with NPCI and RBI guidelines, which require strict agent KYC verification, data encryption, and adherence to UIDAI guidelines.

- Testing Environment: Aeps india offer secure sandbox environments to test transaction flows before going live.

Why Businesses Prefer White Label AEPS API Solutions

Businesses prefer white label AEPS API solution because they bypass expensive, time-consuming software development and regulatory compliance. By using a pre-built, ready-to-deploy best Aeps API solution, Aeps india can instantly offer banking services like cash withdrawals and balance inquiries under their own brand name.

Top reasons why this model is preferred:

- Zero Development Time: Avoid months of coding and security auditing by using pre-built API documentation that gets Aeps platform live in hours.

- Regulatory Exemption: Bypass direct, complex NPCI and UIDAI compliance approvals, as the Aeps india handles the foundational legal requirements.

- Brand Authority: Establish market trust by customizing the front-end interface, Aeps service app, and Aeps dashboard with your own logos and color schemes.

- Network Management: Built-in admin panels allow you to easily manage distributor hierarchies, sub-agents, and transaction margins.

- Automated Commissioning: Automatically split and distribute Aeps agent commissions and ledger management in real-time.

- Instant Settlements: Supports wallet-to-bank settlements for retailers to maintain daily liquidity.

How to Choose the Best AEPS API Provider in India

Aeps india one of the best AEPS API provider in India, prioritize Aeps india that guarantee NPCI compliance, high transaction success rates (99%+ uptime), and instant (T+0) settlements to maintain your agents’ liquidity.

Evaluate potential Aeps india on these key factors:

1. Security & Compliance

- Regulatory Adherence: Ensure the develop Aeps API is fully compliant with RBI, NPCI, and UIDAI guidelines.

- Data Encryption: The Aeps india must utilize L1-certified Registered Devices (RD) and end-to-end encryption for biometric (fingerprint/iris) authentication to prevent fraud.

2. Transaction Success Rate & Uptime

- High Success Rates: Look for Aeps india boasting 𝟗𝟖%+ success rates to prevent transaction failures.

- Redundant Architecture: Aeps india should have backup banking routes to maintain near-perfect uptime, which is critical in remote or rural markets.

3. Commission Structure & Settlements

- Competitive Earnings: Compare the per-transaction slab rate. Aeps india offer margins ranging from ₹10 to ₹15 depending on the withdrawal amount.

- Instant Settlement: Ensure the Aeps india offers T+0 or instant, same-day settlement so your retailers’ working capital isn’t locked overnight.

4. API Integration & Tech Support

- Developer Friendly: Opt for Developer Friendly Aeps API with clear Aeps API documentation, sandbox testing environments, and ready-to-use SDKs to fast-track your launch.

- White-Label Support: If you want to build your own brand, ensure the Aeps india offers a white label Aeps dashboard (with web and Aeps app versions) and robust agent management tools.

5. Multi-Service Ecosystem

- All-in-One Platform: Choose a Aeps india whose AEPS integrate smoothly with BBPS API and Micro ATM services to build a complete digital banking hub.

Why Choose AEPS India for AEPS API Solution

Aeps india one of the top AEPS API provider is critical because it turns your business or retail outlet into a mini-bank, enabling cardless, PIN-less cash withdrawals, balance inquiries, and mini-statements using only a biometric scan and Aadhaar number.

Selecting a Aeps india ensures seamless transactions, compliance, and steady Aeps commission revenue.

Key Reasons to Choose a Top-Tier AEPS API Provider

- Security & Compliance: Aeps india ensure 100% adherence to RBI, UIDAI, and NPCI guidelines. They use heavy data encryption during biometric capture to prevent fraud and secure user data.

- High Reliability & Uptime: Aeps india guarantee 99.9% uptime and transaction success rates exceeding 98% through multiple bank switchovers, minimizing customer frustration.

- Instant Settlements (T+0): Aeps india offer instant or same-day settlements, meaning your working capital and daily cash flow are never locked up when agents process withdrawals.

- Competitive Commissions: Aeps india offers lucrative per-transaction payout structures (often ranging from ₹10 to ₹16 for agents) and transparent billing.

- Multi-Service Platforms: Aeps india bundle AEPS API with other essential financial APIs like best Micro ATM software and BBPS software, allowing you to diversify your revenue streams.

- White-Labeling & Easy Integration: They provide seamless, ready-to-integrated Aeps admin API and white label Aeps admin panel, making it fast for top Aeps software, fintechs, and retail networks to deploy.

- 24/7 Technical Support: Around-the-clock technical assistance helps resolve transaction disputes (e.g., failed transactions where money is deducted) instantly.

Factors to Evaluate

When selecting an aggregator, weigh these criteria:

- Success Rate: Ask for exact Aeps API success metrics; higher is always better to keep agents using your platform.

- Per-Transaction Cost: Compare the setup fees, maintenance costs, and actual commission splits.

- Settlement Terms: Confirm whether settlements are instant (T+0) or next-day (T+1) and if there are associated transfer charges.

Conclusion

Integrating an AEPS API is a smart choice for businesses that want to expand their digital banking services and create new revenue opportunities. With the growing demand for Aadhaar-based banking across India, a reliable AEPS API enables businesses to offer essential services such as cash withdrawal, balance enquiry, mini statement, and Aadhaar authentication through a secure and easy-to-use platform.

A professional AEPS API Integration helps retailers, distributors, fintech companies, and payment service providers deliver fast, secure, and reliable banking services while improving customer satisfaction. It also simplifies business operations with real-time transactions, secure processing, and high transaction success rates.

Integrating an Aadhaar Enabled Payment System (AEPS) API allows your app or website to process secure, biometric-based banking transactions (like cash withdrawals, balance inquiries, and mini-statements) without a debit card or PIN.

One of the biggest advantages of AEPS API Integration is automation. Businesses can process transactions in real time, manage retailers and distributors efficiently, monitor settlements, track commissions, and reduce manual work. This improves operational efficiency while helping businesses scale faster.

Security is equally important in digital banking. A trusted AEPS API Provider offers secure biometric authentication, encrypted data transmission, real-time transaction monitoring, and reliable API connectivity. These features help protect customer information, reduce fraud risks, and build long-term trust.

Choosing a trusted AEPS API provider like AEPS India gives businesses access to advanced technology, secure banking infrastructure, scalable solutions, and dedicated technical support. These features help simplify operations, improve service quality, and create long-term business growth opportunities in India’s rapidly expanding digital payment ecosystem.

Aeps India provides a powerful and secure AEPS API Solution designed for businesses of all sizes. With easy API integration, high transaction success rates, advanced management tools, fast processing, and dedicated technical support, businesses can confidently expand their digital banking network and improve customer satisfaction.

As India’s digital banking and financial inclusion continue to grow, businesses that invest in a trusted AEPS API Provider can strengthen their market presence, increase transaction volume, and build a profitable long-term business.

Connect with AEPS India today to integrate a secure, scalable, and high-performance AEPS API solution and take your digital banking business to the next level.

Complete Guide to AEPS API Integration for Businesses and Retailers

Top AEPS Provider in India: Complete Guide for 2026