Best AEPS Portal in India for Retailers – Complete Guide

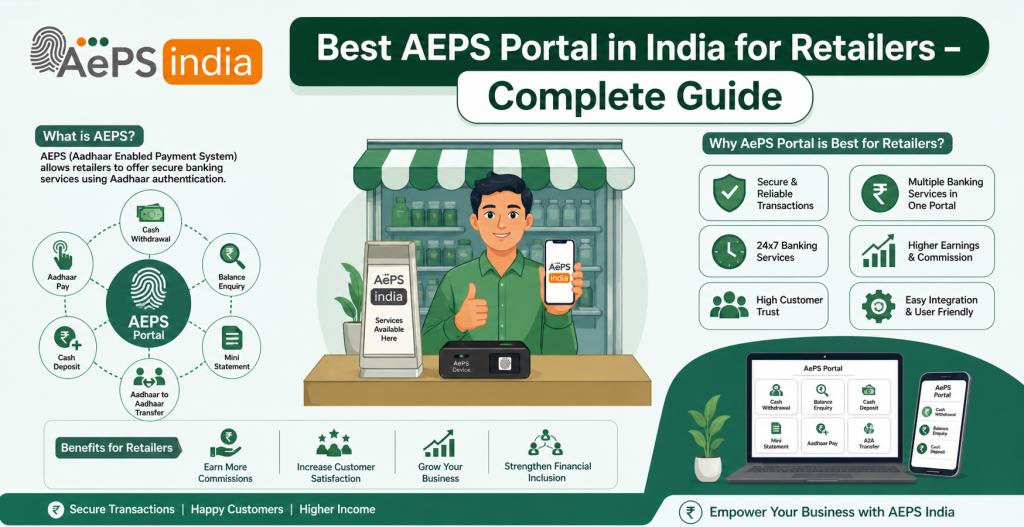

If you are searching for the best AEPS portal in India for retailers, you are exploring one of the fastest-growing opportunities in the digital banking and fintech industry. The Aadhaar Enabled Payment System (AEPS) allows retailers to provide essential banking services such as cash withdrawal, balance enquiry, mini statement, and Aadhaar-based fund transfer directly from their shop. Aeps india is the right AEPS portal provider, retailers can turn their store into a trusted mini banking service center and earn daily commission income.

An AEPS Aadhaar Enabled Payment System portal is a digital platform developed by the NPCI that enables secure, interoperable banking transactions using only an Aadhaar number and biometric authentication (fingerprint/iris). It allows users to perform cash withdrawals, balance inquiries, and mini-statements through Business Correspondents (agents), primarily benefiting rural, unbanked areas without needing a debit card or PIN.

AEPS portals allow retailers to turn their shops into mini-banks, enabling Aeps services like cash withdrawal, balance inquiry, and mini-statements using a customer’s Aadhaar and fingerprint. Top Aeps platforms for 2026 include Aeps India and Noble web studio offering high Aeps commissions up to ₹15+ per transaction.

A powerful AEPS portal solution helps retailers process transactions using Aadhaar authentication and biometric verification like fingerprint devices. This makes banking services simple and accessible, especially for customers in rural and semi-urban areas who may not have easy access to bank branches or ATMs.

Choosing the best AEPS portal for retailers in India is very important for smooth operations. A reliable Aeps platform should offer high transaction success rate, secure biometric authentication, real-time processing, multi-bank support, instant settlement, and an easy-to-use Aeps dashboard. These features ensure faster transactions fewer failures and higher earnings for retailers.

With the growing demand for digital financial services, many shop owners are adopting the AEPS retailer business model to increase their income and attract more customers. A trusted Aeps platform helps retailers manage transactions easily and build long-term customer trust.

Platforms like AEPS India provide advanced AEPS portal solutions for retailers, allowing them to start their digital banking services with simple registration and minimal investment. By joining a trusted AEPS service provider like Noble web studio, retailers can expand their services, attract more customers, and generate a steady income through AEPS transactions.

By partnering with a Aeps india one of the AEPS service provider in India, retailers can start a profitable AEPS business, expand their digital services, and become part of the rapidly growing digital payment ecosystem.

In this guide, you will learn everything about the best AEPS portal in India for retailers, how it works, its benefits, and how retailers can start AEPS business to earn regular commission from digital banking services.

What is AEPS Portal

An AEPS Portal is a secure digital platform developed by the National Payments Corporation of India (NPCI) that enables bank customers to conduct basic banking transactions such as cash withdrawals, balance inquiries, and mini-statements using only their Aadhaar number and biometric authentication (Aeps fingerprint/iris). It acts as a bridge, allowing Business Correspondents (agents) to offer Aeps banking services at the doorstep, specifically catering to rural and underbanked areas without requiring a debit card or PIN.

AEPS Portal Work

An AEPS portal enables secure, cardless, and PIN-less banking transactions cash withdrawal, deposit, balance inquiry, and mini-statement using a customer’s Aadhaar number and biometric authentication (fingerprint/iris). It allows Business Correspondents (BCs) or agents to provide Aeps banking services via a mobile Aeps app or Micro ATM, connecting to the NPCI network for real-time transactions.

Key Aspects of AEPS Portal Work:

- Core Services: Agents can perform Cash Withdrawal, Balance Enquiry, Mini Statement, and Aadhaar-to-Aadhaar Fund Transfers.

- Transaction Flow: The agent enters the 12-digit Aadhaar number, selects the bank, selects the transaction type, and the customer scans their fingerprint on a Aeps biometric device.

- Real-time Processing: The best Aeps portal sends data via the NPCI gateway to the bank for instant verification and transaction completion.

- Commission Model: Agents earn Aeps commission (roughly ₹7 to ₹10 per transaction) on successful transactions.

- Requirements: A valid smartphone/computer, an internet connection, a registered bank account, and a UIDAI certified Aeps biometric device.

Main Services Offered by an AEPS Portal

An Secure AEPS portal enables secure, biometric-based, and interoperable Aeps banking service, allowing customers to use their Aadhaar number and fingerprint/iris scan for transactions at local shops. Main Aeps services include cash withdrawal, balance inquiry, mini-statements, cash deposits, and Aadhaar-to-Aadhaar fund transfers, often without needing a debit card.

Key services offered by an AEPS portal:

- Cash Withdrawal: Enables customers to withdraw cash from their Aadhaar-linked bank account, crucial for rural and unbanked populations.

- Balance Inquiry: Allows instant, real-time checking of the available balance in a bank account.

- Mini Statement: Provides a quick view or printout of the last 5-10 transactions in the account.

- Cash Deposit: Enables secure, immediate depositing of cash into an Aadhaar-linked account.

- Aadhaar to Aadhaar Fund Transfer: Supports secure transfers directly between two Aadhaar-linked accounts.

- Aadhaar Pay: Allows merchants to accept payments from customers via biometric authentication, which can exceed normal withdrawal limits.

- Best Finger Detection (BFD): A best Aeps service used to identify the best fingerprint for successful authentication in case of issues.

- eKYC: Supports electronic Know Your Customer for paperless, real-time verification to open bank accounts.

These Aeps services are supported by Aeps India and other providers for high-volume transactions and secure, 24/7 banking access.

Types of AEPS Portal

AEPS portals in India are primarily classified by their business model White Label Aeps portal (own brand), Aeps B2B/Aeps Admin (managing networks), or Retailer/Agent and offer services like cash withdrawal, balance inquiry, mini-statements, and Aadhaar Pay. Top providers include Aeps India and Noble web studio.

Types of AEPS Portals by Structure

- White-Label AEPS Portal: Aeps portal Designed for businesses that want to launch their own branded AEPS service, typically costing between ₹25,000 and ₹1.2 lakh+.

- B2B/Admin Portal: High-end, comprehensive Aeps admin portal solution for Aeps india managing a large network of agents, often costing over ₹1 lakh to ₹2.5 lakh+.

- Retailer/Agent ID: These are low cost Aeps portal, basic access Aeps portals for agents to conduct transactions.

- Mobile-First AEPS Apps: Aeps india focus on mobile-first, user friendly Aeps apps for quick, on-the-go transactions.

Documents Required to Become an AEPS Retailer

To become an AEPS retailer, you primarily need your Aadhaar card, PAN card, bank account details (for settlement), and proof of business address (shop registration or utility bill). Additionally, you must have a registered mobile number linked to Aadhaar, recent photographs, and an STQC-certified Aeps biometric device.

Essential Documents & Requirements:

- Proof of Identity: Original PAN Card (mandatory) and Aadhaar Card.

- Proof of Address/Business: Shop & Establishment Certificate, Udyam Registration, GST Certificate, or a recent utility bill (electricity/water, 2–3 months old).

- Banking Details: Cancelled cheque, bank passbook, or bank statement for Aeps commission settlements.

- Biometric Device: A UIDAI-registered, STQC-certified Aeps fingerprint or Aeps iris scanner (e.g., Mantra).

- Business Proof: Shop & Establishment Certificate, Udyam Registration GST Certificate or a utility bill (electricity/water, 2–3 months old).

- Personal Documents: Recent passport-sized photographs and an active mobile number.

- Others: Passport-sized photographs, smartphone/computer with internet, and a mobile number linked to Aadhaar.

- Technology: Android smartphone, tablet or desktop computer with a stable internet connection.

- KYC & Registration: Mobile number linked to Aadhaar for OTP, and completed eKYC with a Aeps india.

Who Can Use AEPS Portal

The Best Aadhaar Enabled Payment System portal can be used by any Indian resident who has an Aadhaar-linked bank account to perform basic Aeps banking services. It is designed for interoperable banking meaning a user can access their account through a Business Correspondent (BC) of any bank regardless of where they hold their account.

Users Who Can Utilize AePS Services (Customers)

- Aadhaar Holders: Any individual possessing a valid 12-digit Aadhaar number.

- Bank Account Holders: Individuals with a bank account that is linked (seeded) to their Aadhaar number.

- Rural & Underbanked Residents: Primarily Aeps portal design for individuals in rural or remote areas with limited access to traditional bank branches or ATMs.

- Government Beneficiaries: Individuals receiving direct benefit transfers (DBT) such as pensions, scholarships or MGNREGA wages.

- Minors: Generally available for minors above 10 years of age subject to the issuer bank’s policy.

Entities Who Can Operate AePS Portals (Agents)

Authorized agents, including Business Correspondents (BCs), Bank Mitras, retail shop owners (Kirana stores), and Common Service Centre (CSC) operators, can facilitate AePS services. Aeps india are also involved in the technical integration.

Requirements for Using the AePS Portal

- For Users: A bank account linked to an Aadhaar card, along with biometric verification (fingerprint/IRIS).

- For Agents: Authorized access and certified Aeps Biometric Devices (like Micro-ATMs or POS terminals).

Key Constraints and Rules (As of 2026)

- Transaction Limits: A cap of ₹10,000 per transaction usually applies.

- Security & Compliance: Agents are limited to one acquiring bank, must utilize STQC-certified Aeps L1 devices and inactive agents (3 months) must re-verify KYC.

Why Use AEPS Portal

The Aadhaar Enabled Payment System portal is used for secure, cardless, and PIN-less banking transactions (cash withdrawals, deposits, balance checks) using only an Aadhaar number and biometric authentication. It promotes financial inclusion, allowing rural, unbanked, and, elderly users to access banking services locally through retailers.

Key Reasons to Use the AEPS Portal:

- Convenience and Accessibility: Allows banking transactions at local, nearby shops, reducing the need to travel to bank branches or ATMs.

- High Security: Uses biometric (fingerprint/iris) authentication, minimizing the risk of fraud or unauthorized transactions associated with physical cards and PINs.

- Interoperability: Customers can use their Aadhaar-linked account at any bank’s AEPS-enabled micro-ATM or point-of-sale (PoS) terminal.

- Financial Inclusion: Enables easy doorstep banking for rural and underserved areas, ensuring access for daily wage earners and individuals with limited tech literacy.

- Direct Benefit Transfers (DBT): Facilitates direct receipt of government subsidies and welfare payments.

- For Retailers/Agents: Provides a business opportunity to earn commissions on transactions, increasing footfall at their shop, and allows them to serve their community.

- No Card/PIN Required: Eliminates the need to remember PINs or carry plastic cards.

AEPS acts as a crucial, secure, and accessible bridge for digital cashless banking in both rural and urban India.

Top Use Cases of AEPS Portal

AEPS portals enable secure cardless, and PIN-less banking for rural and underserved areas via biometric authentication. Key use cases include Micro ATM services (cash withdrawals/deposits), balance inquiries, mini-statements, Direct Benefit Transfers (DBT), Aadhaar-to-Aadhaar fund transfers, and merchant payments via Aadhaar Pay.

Key Use Cases of AEPS Portals:

- Micro-ATM Services: Agents act as “mini-banks,” allowing customers to deposit or withdraw cash without a debit card or PIN, often using Aeps India.

- Banking Services: Instant real-time access for checking balances obtaining mini-statements and performing eKYC verification.

- Government Disbursements: Secure direct transfer of government welfare payments pensions, and subsidies (DBT) directly to beneficiaries.

- Merchant Transactions (Aadhaar Pay): Enables small businesses to accept digital payments via biometric authentication.

- Interbank and Intrabank Transfers: Facilitates direct money transfers between Aadhaar-linked accounts.

- Value-Added Services: Retailers can offer utility bill payments and mobile recharges.

These best Aeps portals are essential for enhancing financial inclusion in remote areas.

Key Aspects of AEPS Portal

The High volume AEPS portal is a secure, interoperable Aeps platform enabling cardless, PIN-less banking (cash withdrawals, deposits, balance inquiries, mini-statements) using Aadhaar authentication. It facilitates financial inclusion in rural areas via local agents (Bank Mitras) and supports Direct Benefit Transfers (DBT). Key aspects include mandatory biometric authentication (fingerprint/iris) and, as of 2026, strict KYC compliance.

Key Aspects of the AEPS Portal

- Core Functions: Facilitates essential banking services: cash withdrawal, cash deposit, balance inquiry, mini-statement, and Aadhaar-to-Aadhaar fund transfers.

- Security & Authentication: Uses unique Aeps biometric verification (fingerprint or iris scan) to eliminate fraud risks associated with physical cards and PINs.

- Interoperability: Customers can use any bank-enabled agent regardless of their own bank, promoting a universal interbank system.

- Financial Inclusion: Enables banking services in remote or underbanked, rural areas allowing local shop owners to operate as business correspondents.

- Direct Benefit Transfer (DBT): Acts as a primary efficient channel for withdrawing government pensions and subsidies.

- Setup Requirements: Requires a smartphone or PC a buy Aeps biometric device (fingerprint/iris scanner), and a stable internet connection.

- Regulatory Compliance: As of January 1, 2026, the RBI has mandated strict full Aeps KYC for all AEPS Touchpoint Operators (ATOs).

- Transactional Limits: Daily transaction limits are generally around ₹10,000 to ₹50,000, depending on the bank.

- Revenue Model: Retailers earn Aeps commissions on transactions, making it a low cost Aeps, high volume Aeps business model.

Why Retailers Should Use an AEPS Portal in India

Aeps Retailers in India should use an Highest commission AePS portal to transform their shops into mini-banking hubs, generating extra commission income (₹2–₹15+ per transaction) while increasing customer footfall. It offers secure, biometric-based, cardless transactions, reduces cash management risks, and provides instant (T+0/T+1) settlements, fostering financial inclusion in rural areas.

AEPS India are top contenders for the highest commission AePS portals in 2026, offering up to ₹15 per transaction for super-prime retailers. These Aeps platforms provide competitive Aeps Commission, tiered Aeps commission structures, with maximum payouts on high-value transactions (₹3,000-₹10,000).

Key Reasons to Use an AEPS Portal:

- Additional Revenue Stream: Retailers earn Aeps commissions on every transaction, including cash withdrawals, balance inquiries, and mini-statements, creating a steady, high-margin income source.

- Increased Customer Footfall: Providing banking services acts as a magnet, drawing in more customers, which boosts cross-selling opportunities for existing products.

- Enhanced Security & Convenience: Transactions are authenticated via Aadhaar-based fingerprint/iris scans, significantly reducing fraud risks compared to traditional cash handling.

- Low Setup & Operating Costs: The Aeps system only requires a smartphone or computer and a biometric scanner, making it accessible for small, local retailers.

- Improved Cash Management: Retailers can use the cash generated from daily sales to fulfill customer withdrawal requests, reducing the need to frequently travel to banks for deposits.

- Instant Settlements: Funds are generally credited to the retailer’s wallet instantly or within 24 hours (T+0/T+1), ensuring better cash flow and liquidity.

- Comprehensive Services: Beyond just cash, Aeps platform integrate additional services like Bharat Bill Payment System service (BBPS), Domestic Money Transfer service (DMT) and Micro ATM service.

Key AePS Commission Details for Retailers (2026):

- Commission Structure: Retailers often earn ₹2–₹15+ per withdrawal with higher slabs for larger amounts.

- Transaction Types: Aeps Commission earned on cash withdrawals balance inquiries (₹1–₹5), and mini-statements (₹2–₹7).

- Best Value Slabs: Transactions between ₹3,000–₹10,000 provide the highest Aeps commission (up to ₹13–₹15+).

- Income Potential: Active agents can earn ₹10,000–₹30,000+ monthly, including bonuses for high-volume transactions (e.g., 150–200+ transactions).

- Settlement: Retailers can choose between immediate (T+0) or next-day (T+1) settlement to maintain cash flow.

- Setup Requirements: A smartphone/computer, internet, and an L1 Aeps biometric fingerprint scanner are required.

By using an smooth AePS portal, retailers become crucial trusted and modern Aeps india in their community supporting the Digital India initiative.

Top High-Commission AePS Portals (2026):

- Aeps india: Aeps india Offers up to ₹15 per transaction for Super Prime Retailers and ₹12 for Normal Retailers.

- Noble web studio: Provides a high Aeps commission structure of up to ₹15+ for Prime Agents.

Key Commission Details:

- Highest Slab: Transactions between ₹3,000 and ₹10,000 generally yield the higher Aeps commission (₹13–₹15+).

- Mid/Low Slabs: Transactions below ₹3,000 provide lower commission, generally ranging from ₹2 to ₹7.

- Other Income: Fast Aeps platform offer additional incentives, such as ₹25 for Aadhaar-linked account openings or extra bonuses for high-volume transactions.

- Withdrawal Fees: While Aeps commission is high, always check for potential charges on bank settlements.

Features AEPS Portal for Retailers

AEPS portals allow retailers to become mini-bank branches, offering secure, biometric-authenticated banking services like cash withdrawals, balance inquiries, mini-statements, and cash deposits. Retailers benefit from instant (T+0) wallet settlements, high commissions (₹2–₹15+), increased customer footfall, and low cost Aeps portal setup using a smartphone and Aeps fingerprint scanner.

Key Features of AEPS Portals for Retailers

Core Banking Services:

- Cash Withdrawal: Enables customers to withdraw cash directly from their bank accounts.

- Balance Enquiry: Instant checking of account balances.

- Mini Statement: Generation of last few transactions.

- Aadhaar Pay: Enables merchant payments for higher transaction limits.

Operational & Financial Features:

- Instant Settlement (T+0): Modern Aeps platform offer same-day or real-time settlement of funds to the retailer’s wallet, ensuring continuous working capital.

- High Commission: Retailers can earn up to ₹15–₹20+ substantial High Aeps commission, particularly on higher-value transactions (e.g., ₹3,000–₹10,000).

- Interoperability: Customers can use their Aadhaar number to access accounts from any bank at any enabled retail outlet.

- Easy Onboarding: Simple quick, and digital Aeps KYC processes often allow for agent Aeps onboarding in minutes.

- High Success Rate: Top Aeps platforms boast 98%–99% transaction success rates, reducing failed transactions.

- Additional Services: Highest commission Aeps portal include Money Transfer API Service (DMT), utility bill payments and mobile recharges.

Technical & Security Features:

- Biometric Security: Transactions are authenticated using fingerprint or iris scans via L1 certified Aeps devices, significantly reducing fraud risks compared to traditional methods.

- L1 Device Support: Mandatory use of STQC-certified, secure Aeps L1 biometric devices.

- Dashboard Management: Easy-to-use digital Aeps portal/Aeps app to manage transactions.

- 24/7 Support: Continuous technical assistance for troubleshooting.

Benefits for Retailers

- Increased Revenue: Earn high Aeps commissions on transactions, particularly from underserved rural or semi-urban populations.

- Enhanced Customer Base: Acts as a trusted banking point, increasing footfall and driving sales for other retail products.

- Cash Management: Retailers can use collected cash for further transactions, reducing the need to deposit it into their own bank.

- Low Investment: Requires minimal infrastructure a smartphone/laptop and a purchase Aeps biometric device.

Ease of Setup:

- Low Infrastructure Cost: Requires only a smartphone/computer, an internet connection and a get Aeps biometric device.

Benefits AEPS Portal for Retailers

An AEPS portal allows retailers to turn their shops into mini-banking hubs, driving higher customer footfall and generating steady income through commissions (up to ₹15 per transaction). It offers secure, cardless, and PIN-less cash withdrawals, balance inquiries, and direct benefit transfers (DBT) using biometric authentication.

Key Benefits of AEPS Portal for Retailers:

- Additional Income Stream: Earn attractive Aeps commission, recurring Higher Aeps commission-based income on every transaction particularly for high-value cash withdrawals between ₹3,000–₹10,000.

- Financial Inclusion Impact: Allows retailers to service underbanked/rural populations and handle government pension or subsidy (DBT) withdrawals.

- Increased Customer Footfall & Sales: Aeps india offering banking services attracts more people to the store, providing cross-selling opportunities for existing retail products.

- Reduced Cash Management Risk: Instead of storing large amounts of cash, retailers can use daily cash collections to fulfill withdrawal requests, reducing the need for bank deposits.

- Low Cost and Easy Setup: The best Aeps system only requires a smartphone, an internet connection, and a buy certified Aeps biometric device, making it a low-investment, high-return business model.

- Secure & Instant Transactions: Transactions are authorized via biometric data (fingerprint or iris scan), providing high security against fraud. Most Aeps platform offer instant (T+0) settlement.

- Instant Settlement: Aeps b2b portals offer instant (T+0) or same-day (T+1) settlement or fast, daily settlement of funds directly into the retailer’s bank account, ensuring a steady cash flow.

- Expanded Service Portfolio: Retailers can offer more services, including Aadhaar Pay API service, Domestic Money Transfer API service (DMT), and BBPS API service.

- Higher Customer Trust: Acting as a business correspondent for financial inclusion builds trust and community reputation.

- High Security: Transactions are authorized via biometrics (fingerprint/iris), which significantly reduces the risk of fraud compared to traditional card-based systems.

- Enhanced Customer Trust & Loyalty: Providing convenient secure cardless and PIN-less services in rural or underserved areas builds customer trust.

Operational Benefits:

- High Reliability: Aeps Systems often boast >98% transaction success rates and 99.9% uptime.

- Support for Government Schemes: Facilitates Direct Benefit Transfer (DBT) withdrawals for pensions and subsidies.

- White Label Solutions: Retailers can use customized Aeps portal for branding, as offered by Aeps india.

Aeps india include higher volume Aeps platform that offer user friendly Aeps app and 24/7 technical support ensuring high success rates for transactions.

Step-by-Step Process to Join an AEPS Portal

Registering AePS portal involves choosing an NPCI-approved Aeps india completing Aeps KYC with Aadhaar/PAN, passing biometric verification, and activate Aeps device to start Aeps banking services. The process requires a valid, bank-linked Aadhaar a smartphone/PC and a registered Aeps biometric device.

Prerequisites

Before starting the process, ensure you meet the following requirements:

- Eligibility: Must be an Indian citizen, at least 18 years old.

Documentation:

- A valid Aadhaar card (with a linked mobile number and bank account).

- A Permanent Account Number (PAN ) card.

- Proof of your business address (e.g., utility bill, shop rental agreement, or business registration like Udyam Registration).

- Bank account details for receiving commissions (a cancelled cheque or bank passbook copy).

- Passport-sized photographs.

Equipment:

- A smartphone or computer with a stable internet connection.

- A buying Aeps biometric device (fingerprint or iris scanner).

Step-by-Step Aeps portal Registration Process

Step-by-Step AePS Portal Registration Process

- Meet Eligibility Criteria: You must be at least 18 years old, own a shop or business and have a valid Aadhaar card, PAN card and a bank account for settlement.

- Choose an Authorized AEPS Service Provider: Select a reputable and NPCI-approved Aeps india to act as Aeps india. Best Aeps commission structures, Aeps services offered (e.g., cash withdrawal, balance inquiry, mini-statement, cash deposit), and customer support.

- Fill Registration Form & Submit KYC: Fill out the online Aeps registration form on the chosen top Aeps portal. Submit required documents, including:

- Aadhaar Card (linked to mobile number)

- PAN Card

- Bank Passbook or Cancelled Cheque

- Passport-sized photograph

- Proof of Address (Shop & Establishment License/Utility Bill)

- Complete Biometric Authentication (e-KYC): Purchase Aeps device as guided by Aeps india and install the necessary “Registered Aeps Device” (RD) Aeps service software on your smartphone or computer.

- Verification and Approval: Aeps India will verify your documents and bank details. This may include a physical or virtual visit to your location.

- Undergo Training and Receive Credentials: Once your documents and Aeps device are verified and approved, you will receive an Aeps agent ID and login credentials. The Aeps india will offer training on how to use their b2b Aeps portal/best Aeps app and handle transactions.

- Account Activation & Training: Once approved, your unique Aeps Merchant ID/Aeps ID will be generated. Download the app activate AEPS module and complete the training, if necessary.

- Start Offering Services: Log in to the highest earning commission AEPS portal and begin providing banking services to customers in your shop, earning Aeps commissions on each transaction. Ensure you maintain sufficient cash liquidity to facilitate customer withdrawals.

Key Requirements

- Biometric Device: A registered Aeps biometric scanner (Mantra) is mandatory.

- Aadhaar-Linked Bank Account: Your bank account must be linked to your Aadhaar for settlement.

- Stable Internet: A reliable internet connection for processing real-time transactions.

Key Considerations

- Charges: Aeps india offer free Aeps registration, while others may charge a fee.

- Safety: Ensure the Aeps biometric device is STQC certified for secure transactions.

- “One Operator, One Bank”: Ensure you follow the 2026 guidelines for agent banking regulations.

Aeps Portal Commission Structure

AEPS portal commission structures for 2026 are primarily tiered based on transaction volume, with agents earning approximately ₹2 to ₹15+ per cash withdrawal. Top Highest Aeps commissions are typically on transactions of ₹3,000–₹10,000, while smaller transactions ( ₹100–₹999) yield around ₹2. Additional earnings include ~₹1–₹5 for balance inquiries/mini-statements.

₹100–₹999) yield around ₹2. Additional earnings include ~₹1–₹5 for balance inquiries/mini-statements.

Highest AEPS commissions in 2026 reach up to ₹13–₹15+ per transaction for high-value withdrawals (₹3,000–₹10,000), offered by Aeps India and Noble Web Studio. The structure is usually tiered, with lower amounts (₹1–₹4) for smaller transactions, plus additional earnings from mini-statements (₹2–₹7) and Aadhaar Pay.

Typical 2026 AEPS Commission Slab Structure (for Retailers/Agents)

- ₹100 – ₹999: ₹2.00

- ₹1,000 – ₹1,499: ~₹3.00

- ₹1,500 – ₹1,999: ~₹4.50

- ₹2,000 – ₹2,499: ~₹5.50

- ₹2,500 – ₹2,999: ₹5 – ₹7

- ₹3,000 – ₹10,000: Up to ₹13–₹15+

- Balance Inquiry/Mini Statement: ₹0 – ₹5 per inquiry

- Aadhaar Pay: Up to 1% on transactions up to ₹50,000

Key Details

- Balance Inquiry/Mini-statement: Typically ₹1 – ₹5 per transaction.

- Aadhaar Pay: Up to 1% commission on high-value transactions, allowing for higher, non-standardized earnings.

- Payout Frequency: Commissions are often credited weekly, while bonuses may be monthly.

- Maximizing Earnings: High volume Aeps agents (100+ transactions monthly) often receive additional bonuses.

Key Details for 2026

- Maximum Commission: Best Aeps commission structure offer up to 0.40%–1% with a maximum cap of ₹25–₹30 per transaction.

- Settlement: Aeps portals provide T+0 (instant) or T+1 (next day) settlement.

- Bonuses: High-volume agents (100+ transactions monthly) can receive additional monthly bonuses, sometimes up to ₹2,000.

- Distributor Commission: Often includes a smaller commission (e.g., ₹1–₹2 per transaction) for agents network managers.

Key Features of High-Commission Providers

- High-Value Focus: Maximum earnings are locked at transactions between ₹3,000 and ₹10,000.

- Additional Revenue: Mini-statements and balance inquiries offer an extra ₹0.50 – ₹7 per check.

- Settlement: Aeps india offer instant (T+0) or next-day (T+1) settlement.

- Incentives: High-volume agents can earn an extra ₹2,000+ monthly.

- Top Platforms (2026): Aeps India and Noble Web Studio.

How AEPS Portal Helps Retailers Earn High Commission

AEPS portals help retailers earn high Aeps commissions typically ₹2 to ₹15+ per transaction by transforming shops into mini-banking hubs. Through secure, biometric-based cash withdrawals, balance inquiries, and mini-statements, retailers attract more footfall, creating a high-volume revenue stream with minimal investment especially on transactions between ₹3,000–₹10,000.

Here is how AEPS portals help retailers maximize earnings:

- Tiered Commission Structure: Retailers receive higher Aeps commissions for larger transactions. For example, withdrawing between ₹3,000 and ₹10,000 can yield commissions of ₹13–₹15+ per transaction.

- Additional Service Revenue: Beyond cash withdrawals, retailers earn fixed commissions (approx. ₹1–₹5) on mini-statements and balance inquiries.

- High-Volume Incentives: Aeps india offer bonuses (e.g., over ₹2,000 monthly) for hitting high transaction volume targets.

- Diverse Service Offerings: In addition to cash withdrawals, retailers earn commissions on balance inquiries, Aadhaar Pay (for transactions >₹10,000), and mini-statements.

- Increased Footfall & Sales: Aeps india offering banking services attracts more customers, allowing retailers to cross-sell their primary products, thereby boosting overall business profits.

- Instant Settlement and Low Costs: Reliable Aeps platforms offer instant, secure, (T+0 or T+1) settlement, ensuring high liquidity. The Aeps setup requires minimal investment (a smartphone, internet, and a biometric device).

- Incentives and Bonuses: High volume Aeps agents can receive additional monthly bonuses, sometimes exceeding ₹2,000, for hitting specific, targets.

- Aadhaar Pay for Large Amounts: Using Aadhaar Pay for transactions exceeding standard limits helps maintain high-value, high-commission transactions.

- Low Operational Costs: The Aeps model requires minimal investment, usually just a smartphone and a certified biometric device, making the high commission a significant return on investment.

Key Strategies to Maximize Income:

- Target High-Value Withdrawals: Focus on transactions in the ₹3,000–₹10,000 range to hit higher commission slabs.

- Use Reliable Providers: Aeps india one of the best AEPS service provider with high success rates, such as Aeps India to minimize failed transactions and increase trust.

- Advertise Services: Utilize signage like Aadhaar Banking Here to attract customers,.

- Maintain Cash Flow: Ensure sufficient cash is available to handle daily high-volume demand.

Top Aeps service provider in india like Aeps India often offer competitive rates with some enabling up to ₹15 per transaction.

Aeps Portal Cost and Price Structure

AEPS portal costs in India range from a ₹3,000–₹15,000 setup for basic, white label Aeps portal, or B2B Aeps portal solution to over ₹1,00,000 for advanced, custom-built Aeps API integration. Key expenses include hardware (₹1,500–₹3,000 for biometric scanners) and optional annual maintenance fees of ₹10,000–₹30,000+. Agents typically earn ₹2–₹15+ commission per transaction.

AEPS Portal Setup Cost & Investment

- Setup/Integration Fees: ₹12,000 – ₹35,000.

- Basic/White-Label Portal: ₹5,000 – ₹35,000 (pre-built, branded).

- Advanced/Custom API Integration: ₹45,000 – ₹1,20,000+.

- Agent/Retailer ID Registration: Free to ₹3,000, sometimes around ₹99.

- Biometric Device: ₹1,500 – ₹3,000 (e.g., Mantra MFS100).

- Registration/KYC: Free to ₹3,000.

- Maintenance Fees: ₹10,000 – ₹1,00,000 per year.

- Recurring Fees: Annual Maintenance Charges (AMC) often range from ₹9,999 to ₹30,000+.

- Hardware: Biometric (fingerprint) scanners generally cost ₹1,500 – ₹3,000.

- Transaction Fees & Commissions (Agent Focus):

- Withdrawal Commission: Agents can earn ₹2–₹15+ per transaction, depending on volume.

- Platform Fees: Aeps india charge a flat fee of ₹0.25–₹10 per transaction.

- Agent Registration: Usually free to ₹3,000.

AEPS Customer Charges (End-User Fees)

While often free at own-bank BC points, third-party transactions generally incur fees:

- Cash Withdrawal: ₹5 – ₹20 per transaction.

- Cash Deposit: ₹15 – ₹25 per transaction.

- Balance Inquiry/Mini Statement: Usually free, sometimes ₹5 – ₹10.

Key Factors Affecting Price

- Customization: Full, white label Aeps solutions with branded interfaces cost more than standard, ready-made portals.

- API Provider: High-volume Aeps india offer lower, fixed transaction charges (around ₹12–₹13).

- API Type: Direct Aeps API integrations with Aeps india and Noble web studio are low costing, ranging.

- Support & Maintenance: Aeps india include support in the Aeps portal setup fee, while others charge annual fees.

- Security: High-security, encrypted systems may have higher initial Aeps setup costs.

- Support: Higher maintenance fees often include dedicated support.

Devices Required to Use an AEPS Portal

To use an AePS portal as a merchant or Business Correspondent (BC) in India, you need specific hardware and connectivity to facilitate secure, cardless transactions. As of 2026, regulations mandate the use of advanced, secure Aeps devices to ensure compliance with RBI and NPCI standards.

Here are the essential devices and requirements to use an AePS portal:

1. Mandatory Technical Equipment

- STQC-Certified L1 Biometric Device: As of Jan 1, 2026, Level 1 (L1) compliant fingerprint or iris scanners are required to support Registered Device (RD) services for secure authentication.

- Processing Unit: An Android smartphone/tablet (with USB OTG) or a Windows PC is required to connect the biometric scanner and run the Android AePS application.

- Stable Internet: Reliable 4G/5G, Wi-Fi, or broadband connection for real-time validation.

2. Recommended Equipment

- Thermal Printer: Recommended for providing transaction receipts to customers.

- Power Backup: Power bank or inverter to ensure continuous operation.

3. Required Software and Registration

- AePS App & RD Drivers: The fast Aeps app and specific manufacturer drivers must be installed.

- Documentation: Aadhaar card (bank-linked), PAN card, and business proof (e.g., Udyam Registration) are required for Aeps agent onboarding.

4. Key 2026 Compliance Notes

- L1 Security: L0 devices are obsolete; Aeps L1 devices are mandatory.

- Operational Rules: Agents are restricted to one bank mapping and must perform re-KYC if inactive for three months.

Cash Withdrawal Using AEPS Portal

Cash withdrawal via the Aadhaar Enabled Payment System (AePS) allows secure, cardless transactions using biometric authentication at registered banking points or through BC agents. Users enter their 12-digit Aadhaar number, bank name, and fingerprint to withdraw up to ₹10,000 per transaction, often with daily limits of ₹10,000 to ₹50,000, without needing a PIN or ATM card.

Steps for Cash Withdrawal Using an AEPS Portal (for Agents):

- Login & Setup: Log in to the best AEPS android application and connect the biometric device.

- Select Service: Choose the “Cash Withdrawal” option on the Aeps service portal.

- Enter Details: Enter the customer’s 12-digit Aadhaar number, select their bank name, and input the required amount.

- Authentication: The customer places their finger on the Aeps biometric scanner for secure verification.

- Completion: Upon successful biometric match, the transaction is processed, cash is dispensed by the agent, and a receipt is generated.

Key Features of AEPS Cash Withdrawal:

- Requirements: A bank account linked with Aadhaar.

- Transaction Limits: Generally ₹10,000 per transaction, with daily limits often ranging from ₹10,000 to ₹50,000 depending on the bank.

- Security: High-security biometric authentication makes it fraud-resistant.

- Accessibility: Allows rural/underprivileged communities to withdraw cash locally without visiting a bank branch.

Important Considerations:

- Always ensure you receive a receipt for the transaction.

- Some banks may have lower transaction limits (e.g., ₹2,000 to ₹5,000).

- The service is available at micro ATM service and retail stores.

Compliance in AEPS Portal Solutions

Compliance in Aadhaar Enabled Payment System portal solutions is mandatory to ensure secure, legal transactions, requiring strict adherence to NPCI/RBI guidelines. Key requirements include mandatory agent KYC (Aadhaar/PAN), using STQC-certified Aeps biometric L1 devices, “One Operator, One Bank” policies, and no-data-storage policies for customer biometric/PIN data.

Key Compliance & Security Pillars

- Agent KYC & Registration: All agents/Business Correspondents (BCs) must complete rigorous KYC, including PAN, Aadhaar, and business verification (e.g., Udyam, GST).

- “One Operator, One Bank” Policy: As of 2026, agents are restricted to working with only one acquiring bank to reduce fraud.

- Biometric Security (L1 Devices): Mandatory use of STQC-certified Aeps L1 Registered Device (RD) Service for fingerprint/iris scanning to prevent spoofing.

- Data Non-Storage Policy: Compliant Aeps b2b software must never store sensitive customer data like PINs, Aadhaar numbers, or biometric data on the device.

- Transaction Limits & Monitoring: Daily transaction limits (e.g., ₹50,000) are enforced, with real-time monitoring to detect suspicious activity.

- Re-KYC: Agents inactive for three consecutive months must undergo a fresh KYC process.

- Audit Trails: Systems must maintain detailed logs of all transactions for at least two years.

Operational Compliance

- Transparency: Clearly display service charges before any transaction.

- Receipts: Always provide a digital or printed receipt for every transaction.

- Device Safety: Use secure, dedicated devices, and consider CCTV for physical locations.

Security and NPCI Guidelines for AEPS Portal Services

NPCI and RBI guidelines for affordable AePS portal focus on high-security, mandatory biometric authentication (fingerprint/iris) using STQC-certified devices, and rigorous KYC for agents, including “One Operator, One Bank” policies. Effective 2026, agents inactive for three months require re-KYC, and portals must not store sensitive user data.

Key Security and Compliance Measures

- Biometric Authentication: Mandatory, real-time biometric matching via UIDAI for every transaction.

- Certified Devices: Only STQC-certified fingerprint or Aeps iris scanners are permitted.

- No Data Storage: Portals must not store user biometric data; data must be encrypted.

- Agent Onboarding & KYC: Rigorous, mandatory KYC for all Business Correspondents (BCs/agents).

- “One Operator, One Bank” Policy: Agents can only associate with one acquiring bank to reduce fraud risk.

- Transaction Limits: Maximum limits (often ₹10,000 per transaction, ₹50,000 daily) are enforced.

- Active Monitoring: As of 2026, banks must conduct continuous, risk-based monitoring of agents.

Operational Guidelines for Agents & Portals

- Receipt Requirement: Digital or printed receipts must be provided to customers for every transaction.

- Transparency: Any fees charged must be displayed before the transaction.

- Inactive Agent Rule: Agents with no transactions for three months must undergo re-KYC.

- Transaction Alerts: Immediate SMS alerts must be generated for all transactions.

- Secure Infrastructure: Devices must have updated software, use secure networks, and not be left unattended.

For Users (Safety Measures)

- Identity Check: Always verify the agent’s credentials.

- Fingerprint Safety: Never allow agents to use their own finger or any other object on the scanner.

- Monitor Accounts: Check SMS alerts immediately and report unauthorized activity.

These measures ensure secure, cardless, and PIN-less transactions while enhancing security against fraud.

Why Retailers Prefer a Trusted AEPS Portal Platform

Retailers, particularly those in rural or semi-urban areas, prefer a trusted AEPS portal platform because it transforms their shops into mini-banks driving high-frequency customer traffic and providing a secure, reliable, and high-margin revenue stream. A Aeps b2b platform ensures that transactions are safe, compliant with NPCI and RBI standards, and result in immediate, 24/7, T+0 (same-day) settlements.

Here is a detailed breakdown of why retailers prefer a trusted AEPS portal platform:

1. Reliability and High Transaction Success Rates

- 99.9% Uptime: Trusted Aeps platforms offer high uptime, minimizing failed transactions and “server down” issues, which are crucial for maintaining customer trust.

- High Performance: AEPS India boast >98% success rates, crucial for avoiding financial losses and maintaining a positive reputation in the community.

2. Increased Revenue and High Commissions

- Attractive Earnings: Retailers can earn up to ₹13–₹15+ per transaction for high-value withdrawals (₹3,000–₹10,000).

- Additional Income: Besides withdrawals, agents earn via balance inquiries, mini-statements (approx. ₹1–₹5), and Aadhaar Pay.

- Incentives: Aeps india offer monthly bonuses of ₹2,000+ for high-volume active retailers.

3. Enhanced Security and Trust

- Biometric Authentication: Transactions require unique fingerprint or iris scans, minimizing fraud risks compared to traditional, password-based, or card-based transactions.

- Compliance: Trusted Aeps portals are NPCI/RBI-certified and adhere to strict, 2026-mandated security, such as “One Operator, One Bank” rules, liveness detection, and Buy L1 Aeps devices.

4. Instant Settlements (T+0) and Cash Management

- Liquidity: Immediate (T+0) or same-day (T+1) settlement ensures that working capital is never blocked, allowing agents to reinvest in their business quickly.

- Cash Recycling: Retailers can use cash from daily sales to fulfill withdrawal requests, reducing the risk and cost of transporting cash to banks.

5. Increased Customer Footfall and Business Growth

- One-Stop Shop: Aeps india offering essential banking services (cash withdrawal, balance inquiry) attracts more customers, especially in unbanked areas, leading to increased impulse purchases of other, everyday items.

- Service Expansion: Trusted Aeps b2b portal often integrate additional services like Best Micro ATM, Best BBPS (bill payments), and Domestic Money Transfer (DMT), making the shop a comprehensive financial hub.

6. User-Friendly Technology and Support

- Simple Interface: Intuitive, 24/7 accessible Aeps b2b apps allow even tech-illiterate shop owners to process transactions with minimal training.

- 24/7 Technical Support: Immediate support via WhatsApp or phone helps resolve failed transactions instantly, avoiding customer disputes and losses.

How AEPS Portal Helps Grow Digital Banking Services

An Highest earn AEPS portal drives digital banking growth by enabling secure, cardless, and PIN-less transactions (cash withdrawal, deposit, balance inquiry) via biometrics, bridging the rural-urban gap. It promotes financial inclusion, facilitates government subsidies (DBT), and converts local Kirana shops into functional, interoperable, and, 24/7 banking micro-ATMs.

How AEPS Portals Grow Digital Banking Services:

- Financial Inclusion & Rural Access: AEPS allows individuals in remote or underserved areas to access banking services at local retail shops, eliminating the need to travel long distances to bank branches.

- Cardless & PIN-less Transactions: Transactions require only an Aadhaar number and fingerprint/iris scan, making banking accessible to non-tech-savvy users.

- Direct Benefit Transfer (DBT): It enables secure and direct receipt of government subsidies, pensions, and wages, reducing corruption and delays.

- Interoperability: Customers can use their bank account at any AEPS-enabled agent, regardless of the bank, fostering a unified digital ecosystem.

- Empowering Local Retailers: Local shopkeepers, acting as Business Correspondents (BCs) or agents, earn commissions while increasing customer footfall, turning their shops into mini-banks.

- Enhanced Security: Biometric authentication reduces fraud risks associated with physical cards and PINs.

- Low Cost & High Efficiency: Provides a cost-effective alternative for banks to expand their reach without needing physical infrastructure.

Aeps india – High Commission Aeps Portal Provider

High Commission AEPS portals in India such as Aeps India and Noble Web Studio, offer up to ₹15–₹17 per transaction for agents in 2026, particularly on high-value withdrawals (₹3,000-₹10,000). These platforms provide instant (T+0) settlement, 99% uptime, and require minimal investment a smartphone/PC and a biometric device.

Aeps india one of the stand No.1 Top AEPS portal providers in India for 2026, offering high commissions up to ₹15–₹17 per transaction and99% uptime, include Aeps India and Noble Web Studio. These Aeps platform provide secure, NPCI-certified Aeps solutions with instant (T+0) settlement for retailers, featuring L1 Aeps certified biometric device support.

Key Features & Benefits

- High Earnings: Aeps india offer tiered Aeps commissions, with up to ₹13–₹15+ for ₹3,000–₹10,000 withdrawals and ₹0.50–₹5 for balance inquiries/mini-statements.

- Instant Settlement: Options for T+0 (instant) or T+1 (next-day) settlement for better cash flow.

- Diverse Services: Beyond cash withdrawal, fastest Aeps portal offer Aadhaar Pay services, best Micro ATM services, and best BBPS Services.

- Simple Registration: Aeps india and Noble web studio free, instant, or low-cost activation for retailers.

- Support & Security: 24/7 technical support, 98%–99% uptime, and NPCI/RBI compliance.

- Requirements: Smartphone/PC, L1-certified biometric device, and KYC documentation (Aadhaar, PAN).

For maximum earnings Aeps India and Noble Web Studio are considered top choices for 2026 due to their high speed Aeps API secure and high commission Aeps structures.

How to Choose the Best AEPS Portal Provider in India

Aeps india is the best AEPS portal provider in India involves prioritizing high transaction success rates (>98%), instant (T+0) settlement, and transparent, high-commission structures (₹5–₹15+ per transaction). Ensure the leading Aeps platform is NPCI-compliant, offers 24/7 technical support, and supports multiple Aeps services like Micro ATM and DMT service to maximize revenue.

Key Factors to Evaluate When Choosing an AEPS Provider:

- Transaction Success Rate & Uptime: Look for a Aeps india promising over 98-99% success rates and minimal downtime to ensure reliable daily service particularly for rural clients.

- Commission Structure & Transparency: Choose a Aeps admin panel with a clear, competitive Aeps commission structure (up to ₹15+ per transaction) without hidden fees.

- Settlement Speed (T+0/T+1): Ensure the Aeps india offers instant (T+0) or same-day (T+1) settlement to maintain cash flow.

- Security & Compliance: The secured Aeps portal must be Authorized by the National Payments Corporation of India (NPCI) and compliant with RBI/UIDAI, supporting L1-certified Biometric RD devices.

- Customer Support: 24/7 technical support via phone, WhatsApp, or email is crucial to resolve failed transactions instantly.

- User-Friendly Interface: The top Aeps app/web portal should be intuitive and ideally, support local languages for easy operation.

- Additional Services: Select aeps banking platform offering, at minimum, top AEPS service, Micro ATM, Domestic Money Transfer (DMT), and BBPS service provide comprehensive banking services.

Why Choose Aeps india for AEPS Portal Solution

Aeps india one of the professional AEPS portal provider is crucial for securing high-speed, 99.9% uptime, and compliant financial transactions (cash withdrawals, balance inquiries, mini-statements). Aeps india ensures maximum commissions (₹5–₹15+ per transaction), instant (T+0) settlements, robust security (NPCI/RBI compliance, L1 devices), and 24/7 technical support, which are vital for increasing retail income and trust.

Here are the key reasons to choose a professional AEPS portal solution provider:

- High-Security Standards & Compliance: Aeps india ensure 100% adherence to NPCI, RBI, and UIDAI guidelines, utilizing L1-certified Registered Devices (RD) and biometric liveness detection to prevent fraud.

- Superior Reliability & Performance: Aeps India guarantee high uptime (99.9%), ensuring a high success rate and minimizing failed transactions, which is crucial for customer trust.

- Maximum Earnings & Fast Settlements: Aeps india offer competitive commissions (often ₹12–₹15 per transaction) and instant (T+0) or same-day (T+1) settlements, allowing for better cash flow management.

- Comprehensive Service Offerings: Beyond cash withdrawals, quality providers offer integrated, multi-service platforms including Micro-ATM (Mini ATM), Bharat Bill Payment System (BBPS), and Domestic Money Transfer (DMT).

- 24/7 Technical Support: Instant round-the-clock, technical assistance is available for troubleshooting and to avoid financial losses.

- User-Friendly Interface & Reporting: A professional Aeps dashboard provides detailed, real-time transaction reports, making it easy to track earnings and manage operations.

Partnering with a Aeps India and Noble Web Studio is essential for building a profitable secure and efficient digital banking business.

Future Trends AEPS Portal

The future of Aadhaar Enabled Payment System (AEPS) portals is transitioning towards becoming secure, AI-driven, and comprehensive rural financial hubs by 2026, with an estimated 3.5 billion transactions projected annually. Key trends for 2026-2030 focus on enhanced security, multi-modal biometric authentication, and deep integration with the wider digital financial ecosystem.

Here are the key future trends of AEPS portals:

1. Enhanced Security and Regulatory Compliance

- L1 Device Mandate: From Jan 1, 2026, all devices must be STQC-certified and Level 1 (L1) compliant to ensure secure, encrypted data and lower fraud.

- AI-Driven Liveness Detection: To combat spoofing, AI-based, real-time liveness checks for biometrics are becoming standard.

- Stricter Agent Controls: Policies like “One Operator, One Bank” and mandatory re-KYC for inactive agents are enhancing accountability.

2. Advanced Technology and Settlement

- Multi-Modal Biometrics: Integration of iris and facial recognition is improving success rates, especially for users with worn fingerprints.

- Instant Settlements (T+0): Instant or same-day (T+0) settlement is becoming the norm, improving liquidity for agents.

- AI and Blockchain: AI is enhancing risk scoring, while blockchain is being explored for secure, immutable transaction records.

3. Transformation into Financial Hubs

- Expanded Services: Local agents are evolving into “mini-banks,” offering micro-loans, insurance, and BBPS services.

- Deep UPI & Aadhaar Pay Integration: Enhanced convergence with UPI-ATM and expansion of Aadhaar Pay for transactions up to ₹50,000.

4. Improved User/Agent Experience and Income

- Digital Interfaces: Mobile-first, Android Aeps app, and voice-based payments are simplifying transactions for rural users.

- Higher Earnings: Tiered commission models and performance-based incentives for high-volume agents are significantly increasing potential income.

These trends are transforming local shops into essential, secure, and technologically advanced rural financial hubs.

Conclusion

The AEPS portal in India has become an important digital Aeps banking solution for retailers who want to provide easy financial services to their customers. With the help of an advanced AEPS service portal, retailers can offer services like cash withdrawal, balance enquiry, mini statement, and Aadhaar-based transactions directly from their shop. This makes banking services more accessible for customers, especially in rural and semi-urban areas where bank branches and ATMs may not be easily available.

An Powerfull AEPS Portal is a digital Aeps platform that allows bank customers to perform basic banking transactions such as cash withdrawals, deposits, and balance inquiries using their 12-digit Aadhaar number and biometric authentication (fingerprint/iris scan). Developed by the National Payments Corporation of India (NPCI), it facilitates secure, cashless banking for rural or underserved areas via business correspondents (BCs) without needing a debit card or PIN.

The Aadhaar Enabled Payment System (AEPS) is a NPCI-developed Aeps platform allowing secure, instant banking (cash withdrawal, balance inquiry, mini-statement) using only Aadhaar authentication and biometrics. It operates 24/7 via Banking Correspondents (BCs) micro ATM and High commission Aeps app.

AePS portals allow retailers to turn their shops into mini-banks, offering cash withdrawals, balance inquiries, and mini-statements using Aadhaar authentication. Top Aeps service platforms include Aeps india and Noble Web Studio with commissions ranging from ₹2 to over ₹15 per transaction. Registration typically requires PAN, Aadhaar, bank details, and a biometric device.

Aeps india one of the high quality AEPS portal provider offers important features such as secure biometric authentication, real-time transaction processing, multi-bank support, high transaction success rate, instant settlement, and a user friendly Aeps dashboard. These features help retailers complete transactions quickly and provide a smooth banking experience for customers.

With the help of a trusted AEPS portal software, retailers can easily offer services like AEPS cash withdrawal service, Aeps balance enquiry service, Aeps mini statement service, and Aadhaar-based money transfer. These Aeps services are especially valuable in rural and semi-urban areas where many people rely on local shops for quick and convenient banking access.

Before choosing an AEPS service platform, retailers should check the Aeps india reliability, uptime Aeps portal performance, security standards, commission structure, and technical support. A strong and stable Aeps platform ensures fewer transaction failures and better earnings for agents and retailers.

As digital financial services continue to expand in India, investing in the best AEPS portal solution for retailers can help shop owners turn their stores into trusted mini banking centers. With the right technology partner and a reliable AEPS system, retailers can grow their customer base, increase transaction volume, and build a steady source of income in the rapidly growing fintech market.

A reliable platform like AEPS India provides a secure and easy-to-use AEPS portal solution designed for retailers and fintech businesses. With features such as fast transaction processing, high success rates, and reliable technical support, retailers can manage their AEPS banking services smoothly and grow their customer base.

Starting AEPS retailer business is a smart opportunity for entrepreneurs who want to enter the digital financial services sector. By using a trusted AEPS portal platform, retailers can expand their services, build customer trust, and generate consistent income through Aadhaar-based banking transactions.

FAQ – Best AEPS Portal in India for Retailers

An AEPS portal is an online platform that allows retailers to provide Aadhaar Enabled Payment System (AEPS) services to customers. Through this portal, retailers can offer services like cash withdrawal, balance enquiry, mini statement, and Aadhaar-based money transfer using biometric authentication.

To start an AEPS business for retailers, you need to register with a Aeps india, complete the KYC process, use a certified biometric device, and get access to a secure AEPS dashboard. After activation, retailers can start processing transactions and earning commission.

The AEPS portal for retailers works through Aadhaar authentication. A customer enters their Aadhaar number, selects the bank, and verifies the transaction using a fingerprint Aeps biometric device. After successful authentication, the requested service such as cash withdrawal or balance enquiry is completed instantly.

To start using an AEPS portal for retailers, you need to register with a trusted AEPS service provider in india like AEPS India. After completing the KYC verification and Aeps registration process, the Aeps india will give you access to the AEPS retailer portal to start offering services.

A reliable AEPS service portal provides multiple banking services, including:

Cash Withdrawal

Balance Enquiry

Mini Statement

Aadhaar to Bank Transactions

Basic Aeps Banking Services for Customers

These services help customers access banking facilities without visiting a bank branch.

Anyone interested in providing digital banking services can start AEPS retailer business. Common users include:

Retail shop owners

Mobile recharge and bill payment shop owners

Fintech service providers

Small entrepreneurs in rural and urban areas

They can use the best AEPS portal in India to offer convenient financial services to customers.

To operate an AEPS portal, retailers usually need:

A smartphone, computer, or laptop

A biometric fingerprint scanner

Stable internet connection

Access to a trusted AEPS portal platform

These tools allow retailers to perform secure Aadhaar-based transactions.

Retailers get many benefits from using a secure AEPS portal, such as:

Opportunity to earn high commission per transaction

Provide banking services without a bank branch

Increase daily customer visits

Simple and easy transaction process

Support for financial inclusion in rural areas

To start AEPS services, retailers usually need:

Biometric fingerprint scanner

Smartphone, tablet, or computer

Internet connection

AEPS portal login provided by the Aeps india

These tools help retailers perform secure biometric AEPS transactions easily.

Retailers earn commission on every AEPS transaction completed through the Aeps b2b portal. Each service, such as cash withdrawal or balance enquiry, generates a small commission, which becomes a steady source of income as the number of transactions increases.

Yes, AEPS portals are secure because they use biometric authentication and Aadhaar verification for every transaction. The system follows the guidelines of the National Payments Corporation of India (NPCI) to ensure safe and reliable digital banking services.

The commission in AEPS services depends on the service provider and transaction volume. Retailers usually earn commission on cash withdrawal, balance enquiry, and other banking transactions, which helps them generate a steady extra income.

Using the best AEPS portal in India helps retailers provide reliable digital banking services in their shop. It also helps them earn commission on every AEPS transaction, increase customer traffic, and grow their business with secure Aadhaar-based payment services.

Yes, the Aadhaar Enabled Payment System is designed with strong security features. Transactions are verified through Aadhaar authentication and biometric verification, which makes the system secure and reliable for both retailers and customers.

The AEPS system plays an important role in rural areas where banking infrastructure is limited. Through local retailers using an AEPS portal, customers can access essential banking services without traveling long distances to a bank or ATM.

To register for an AEPS portal in India, you need to connect with a Aeps india that offers AEPS portal solutions, retailer registration, and technical support. After completing the registration process, you can start providing Aadhaar-based banking services.

A trusted platform like AEPS India offers one of the best AEPS portal solutions for retailers, providing secure transactions, fast processing, easy dashboard management, and reliable support to help retailers grow their digital banking service business.

After completing registration and KYC verification, the AEPS retailer portal is usually activated within 24 to 48 hours. Once activated, retailers can immediately start providing AEPS services to customers.

Before selecting an Aeps india, retailers should check:

Platform reliability and uptime

Security and NPCI compliance

Transaction success rate

Commission structure

Technical support availability

Choosing the right portal helps retailers run a successful AEPS business.

AEPS India is a trusted platform that provides a reliable AEPS portal for retailers. It offers secure transactions, high success rates, fast processing, and dedicated support. Retailers can easily start their AEPS business and provide digital banking services to customers with confidence.

AEPS Software Free Demo — Try It Now

Free AEPS Registration Online in India