AePS Service in India: Complete Guide for Businesses

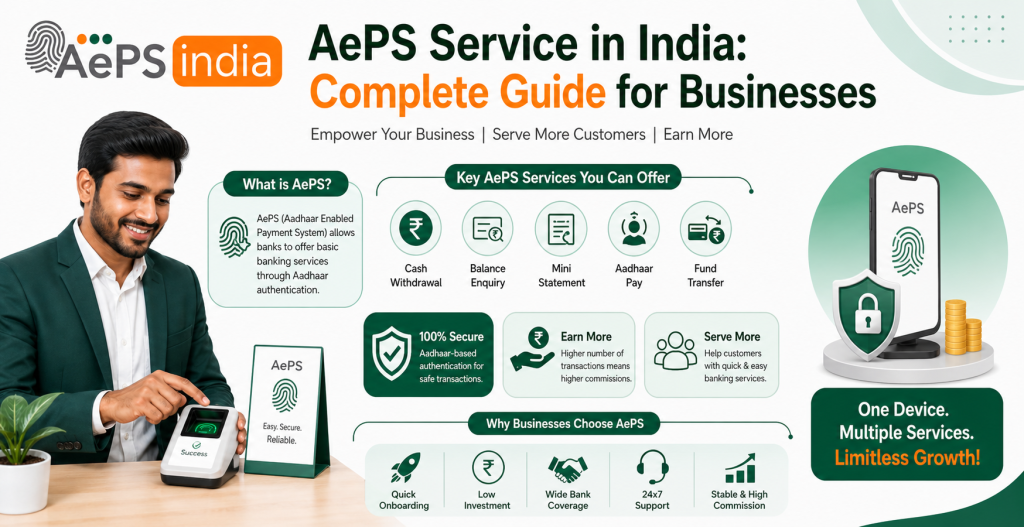

The AEPS service in India has made banking services simple, fast, and accessible for everyone. AEPS stands for Aadhaar Enabled Payment System, which allows people to use basic banking services with the help of their Aadhaar number and biometric verification. This system is especially helpful in rural and semi-urban areas, where bank branches and ATMs are limited.

AePS (Aadhaar Enabled Payment System) services allow users to perform basic banking like cash withdrawal, deposit, fund transfers, and balance inquiries using their Aadhaar number and biometric authentication (fingerprint/iris scan) at micro ATM or banking agents, primarily in rural India, promoting financial inclusion by eliminating the need for physical cards or PINs. Key services include: Cash Withdrawal/Deposit, Fund Transfer (Aadhaar to Aadhaar), Balance Inquiry, Mini Statement, eKYC, and Direct Benefit Transfers (DBT) for government schemes.

With AEPS services, customers can easily perform cash withdrawal, balance enquiry, and mini statement without using a debit card or visiting a bank. All transactions are completed securely using fingerprints, making AEPS a safe and trusted digital banking solution.

The AEPS service in India is widely used by banking correspondents, retailers, CSPs, and digital service centers to provide doorstep banking services. It helps agents serve more customers daily and earn commission on every successful transaction, making AEPS a profitable business opportunity with low investment.

This complete guide will help you understand what AEPS service, how AEPS service work in India, its benefits, features, and why AEPS is an important part of India’s digital financial ecosystem.

What is AEPS Service

AePS Aadhaar Enabled Payment System services are basic banking transactions performed using an Aadhaar number and biometric authentication (fingerprint/iris scan), allowing users to withdraw cash, deposit money, check balances, or transfer funds at micro ATM or PoS terminals, especially in rural areas, without needing cards, PINs, or smartphones, promoting financial inclusion. Developed by NPCI, it links directly to bank accounts for secure, convenient access to banking.

AEPS (Aadhaar Enabled Payment System) is a secure, bank-led system by NPCI that lets users access bank accounts for basic transactions (cash withdrawal/deposit, fund transfer, balance inquiry) using just their Aadhaar number and biometrics (fingerprint/iris) at authorized micro-ATM or agents, crucial for financial inclusion in rural India.

AEPS Service Work

AEPS (Aadhaar Enabled Payment System) service work involves using your Aadhaar number and biometrics (fingerprint/iris scan) at a micro-ATM or Business Correspondent (BC) to perform basic banking like cash withdrawal, deposit, balance inquiry, and fund transfer, enabling secure, cardless, and PIN-less banking, especially for rural areas, by linking users to their bank accounts for instant financial inclusion.

How AEPS Service Works

- Visit an Agent: Go to an AEPS-enabled micro-ATM or a Business Correspondent (BC) agent (like a local shopkeeper).

- Provide Details: Give your 12-digit Aadhaar number and select your bank name.

- Choose Transaction: Select the service you need (e.g., Cash Withdrawal, Balance Inquiry, Fund Transfer).

- Biometric Authentication: Authenticate your identity using your fingerprint or iris scan.

- Transaction Processing: The request is sent to your bank’s server for verification.

- Confirmation: Upon success, cash is dispensed or funds are transferred, and a receipt is provided.

Read Blog : Best AEPS Service Provider Company in India: Complete Guide

Who Can Use AePS Service

Anyone in India with an Aadhaar card linked to an active bank account can use AePS (Aadhaar Enabled Payment System) for basic banking services, requiring only their Aadhaar number, linked bank account, and biometric (fingerprint/iris) authentication at micro-ATMs or Business Correspondent (BC) points for services like cash withdrawal, deposits, and balance inquiries, making it great for rural areas.

Who is eligible?

- Indian Residents: Any citizen of India.

- Aadhaar Linked Bank Account: Must have an Aadhaar number linked to their bank account with a participating bank.

What do they need to use it?

- Aadhaar Number: Their unique 12-digit Aadhaar ID.

- Biometric Data: Fingerprint or iris scan for authentication.

- Aadhaar-Enabled Bank Account: An active bank account linked to their Aadhaar.

- AePS Outlet: Access to a micro ATM or Business Correspondent (BC) agent.

Who benefits?

- Rural Populations: Especially those without easy access to bank branches or ATMs, as BCs provide doorstep banking.

- Smartphone/PIN Users: Individuals who prefer not to use smartphones or remember PINs, relying on biometrics instead.

Services Available Under AePS

The (AePS) Aadhaar Enabled Payment System provides a suite of basic, interoperable banking services to customers using their Aadhaar number and biometric authentication (fingerprint or iris scan) at a micro-ATM or banking correspondent (BC) point.

The primary services available under AePS include:

- Cash Withdrawal: Customers can withdraw cash from their Aadhaar-linked bank account. The maximum limit per transaction is typically ₹10,000, with monthly limits often set around ₹50,000 to ₹1,00,000, depending on the bank.

- Cash Deposit: Funds can be deposited into an Aadhaar-linked account through an AePS point.

- Balance Inquiry: Users can instantly check their available bank balance.

- Mini Statement: A summary of recent transactions can be generated and viewed.

- Aadhaar to Aadhaar Fund Transfer: Money can be transferred between two different bank accounts, provided both are linked to Aadhaar numbers. This does not require the beneficiary’s account number or IFSC code.

- BHIM Aadhaar Pay: This allows merchants to receive cashless payments from customers using Aadhaar authentication, extending digital payment acceptance to small businesses.

- Disbursement of Government Entitlements: AePS facilitates the direct and transparent transfer of government subsidies, pensions, and NREGA wages into the beneficiaries’ Aadhaar-linked accounts (Direct Benefit Transfer – DBT).

To use these services, a customer must have a bank account that is linked with their Aadhaar number. AePS is a key initiative by the National Payments Corporation of India (NPCI) to promote financial inclusion in remote and rural areas of the country.

Top Use Cases of Aeps Service

AePS (Aadhaar Enabled Payment System) use cases focus on financial inclusion, bringing banking to rural/unbanked areas via local agents (Business Correspondents or retailers) using Aadhaar biometrics for services like Cash Withdrawal, Deposit, Fund Transfer, Balance Inquiry, and Mini Statement, plus facilitating Government Direct Benefit Transfers (DBT) and Micro ATM services, essentially creating “mini-banks” at retail points.

Core Banking Services

- Cash Withdrawal: Users withdraw cash from Aadhaar-linked accounts using biometrics at retail outlets.

- Cash Deposit: Depositing cash into Aadhaar-linked accounts through these micro ATMs.

- Balance Inquiry: Checking account balances instantly using Aadhaar.

- Mini Statement: Getting a summary of recent account transactions.

- Fund Transfer: Sending money between Aadhaar-linked accounts (Aadhaar-to-Aadhaar).

Financial Inclusion & Government Services

- Direct Benefit Transfers (DBT): Governments disburse pensions, subsidies (like NREGA), and other benefits directly into beneficiaries’ accounts.

- Microfinance: Facilitating loan repayments for borrowers through local agents.

- eKYC: Enabling digital customer verification.

Merchant & Retailer Services

- Micro-ATM: Retailers act as Business Correspondents, offering banking services through micro ATM service.

- BHIM Aadhaar Pay: Allowing cashless payments at merchant stores using Aadhaar for verification.

- Utility Payments: Paying bills for electricity, water, and other services.

Read Blog : How AePS API Service Is Transforming Rural Banking in India

Documents Required for AEPS Activation

To activate AEPS (Aadhaar Enabled Payment System), you need your Aadhaar Card, PAN Card, and Bank Account details (passbook/cancelled cheque), plus a linked mobile number and photo, but the key is your Aadhaar must be linked to your bank for transactions, often requiring a biometrics device for agents. For a customer, just the Aadhaar & linked bank account + biometrics suffice at a Micro-ATM/BC point.

For Individual Customers (To Use AEPS)

You don’t need to “activate” AEPS specifically; you just need your details ready for use.

- Aadhaar Number: Your unique identification number.

- Linked Bank Account: Your bank account must be linked with your Aadhaar.

- Biometric Authentication: Fingerprint or iris scan.

- Optional: Your physical Aadhaar card isn’t always needed, but the number is.

For Agents/Retailers (To Offer AEPS Services)

To become an AEPS agent and provide services, you need more for setup and registration.

- Personal Documents: Aadhaar Card, PAN Card, Passport-sized Photograph.

- Bank Proof: Bank account details (cancelled cheque, passbook copy).

- Connectivity: Smartphone/Computer with Internet.

- Hardware: Biometric Device (fingerprint/iris scanner).

- Mobile Linkage: A functional mobile number linked to your Aadhaar.

- Registration: Complete an AEPS service provider like Aeps india registration form and Aeps Video KYC.

Key Step: Ensure your bank account is linked to your Aadhaar, which you can often do via your bank’s app, website, or branch.

How to Enable Aadhaar Enabled Payment System?

To enable the Aadhaar Enabled Payment System (AePS), you must first link your Aadhaar to your bank account, which can be done at your bank branch, via ATM, or through online banking; once linked, you can use AePS at micro-ATMs or banking correspondents by providing your Aadhaar number and biometric authentication (fingerprint/iris) for transactions like cash withdrawal or balance checks, as it uses your primary linked account.

Step 1: Link Aadhaar to Your Bank Account

- At the Bank Branch: Visit your bank, fill out an Aadhaar linking form, provide a copy of your Aadhaar, and get acknowledgment.

- Through ATM: Use your debit card, go to Services > Registrations > Aadhaar Registration, select your account, and enter your Aadhaar number.

- Via Internet/Mobile Banking: Log in and find the “Update Aadhaar” or similar option in the profile/services section to submit your Aadhaar number.

Step 2: Use the AePS Service (Once Linked)

- Find an AePS Point: Go to a bank branch, banking correspondent (BC), or micro-ATM (like those at small shops).

- Provide Details: Enter your 12-digit Aadhaar number and select your bank.

- Choose Transaction: Select the service (cash withdrawal, deposit, balance inquiry) and enter the amount if needed.

- Biometric Authentication: Place your finger on the biometric scanner (fingerprint or iris scan) for verification.

- Confirmation: The transaction processes, and you’ll get a receipt and an SMS confirmation if registered for alerts.

Key Requirement: Only your primary bank account linked to Aadhaar can be used for AePS transactions.

Read Blog : AEPS Services for Business Growth: A Step-by-Step Guide

Why AEPS Service is Important

The Aadhaar Enabled Payment System (AEPS) is important because it is a critical tool for financial inclusion, providing secure, accessible, and convenient banking services to millions of people in India, especially in rural and underserved areas.

Key Reasons Why AEPS Service Is Important

- Promotes Financial Inclusion: By offering basic banking services in rural areas through local correspondents, AEPS allows individuals without easy access to bank branches to participate in the formal financial system.

- Enhances Accessibility and Convenience: Transactions require only an Aadhaar number and biometric authentication, removing the need for cards or internet for users, making it easy to use for people with limited technical skills or literacy.

- Ensures Secure Transactions: Utilizing unique biometric data for verification makes transactions more secure and reduces risks associated with traditional methods like cards and PINs.

- Facilitates Government Benefit Transfers (DBT): AEPS enables the direct and transparent delivery of government benefits and pensions to beneficiaries’ Aadhaar-linked accounts, helping to minimize delays and corruption.

- Interoperability: This bank-led system allows customers of any bank to perform transactions at any AEPS service point, promoting a unified banking experience.

- Cost-Effective: AEPS provides a less expensive way for banks to extend services into remote regions compared to establishing physical branches and ATMs.

- Empowers Local Businesses: Local shops and retailers can act as banking correspondents, earning commissions and increasing customer traffic.

AEPS is a vital element of India’s digital transformation, making banking accessible, secure, and straightforward for citizens, supporting the goal of a digitally empowered and financially inclusive society.

How Retailers Earn Daily Income from AEPS

Retailers earn daily income from the Aadhaar Enabled Payment System (AEPS) primarily through commissions on each transaction they facilitate and by increasing overall customer footfall to their shops. By acting as local “micro-ATMs” or banking points, they attract customers needing essential financial services.

Primary Income Source: Commissions

Retailers partner with an Aeps india to offer services and, in return, receive a commission for every successful transaction processed.

- Transaction-Based Earnings: Commissions are the direct income source. The amount varies depending on the type and value of the transaction and the specific Aeps india commission structure.

- Tiered Structure: For cash withdrawals, which are the main service, commissions often follow a tiered model. Higher transaction amounts yield a higher commission (e.g., a few rupees for smaller withdrawals and up to ₹13 or more for transactions over ₹3,000).

- Daily Payouts: Commissions are typically credited to the retailer’s wallet or bank account daily, providing a consistent and predictable daily income stream.

| Transaction Type | Typical Commission (Approx.) |

|---|---|

| Cash Withdrawal | ₹5–₹15+ per transaction |

| Balance Inquiry | ₹1–₹5 per transaction |

| Mini Statement | ₹3–₹7 per transaction |

| Fund Transfer (Aadhaar-to-Aadhaar) | Commissions vary, generally ₹5–₹10 per transaction |

Secondary Income Streams: Increased Business

Offering AEPS services turns a local shop into a one-stop financial hub, which indirectly boosts income in several ways.

- Increased Customer Traffic: The ability to withdraw cash or check balances without traveling to a distant bank or ATM attracts new customers, especially in rural and underserved areas.

- Cross-Selling Opportunities: Once customers are in the store for banking services, they are more likely to purchase other goods or use additional services offered by the retailer, such as mobile recharges, utility bill payments (electricity, gas, water), or travel bookings.

- Enhanced Customer Loyalty: Providing a much-needed, reliable, and secure service builds trust and reputation within the community, encouraging repeat business.

By strategically promoting and combining these services, retailers can significantly boost their daily earnings, with some reports suggesting potential monthly incomes ranging from ₹10,000 to over ₹30,000, depending on location and transaction volume.

Read Blog : AEPS API Solution: Complete Guide to Choosing the Right API Provider

AEPS Registration and KYC Process

AEPS (Aadhaar Enabled Payment System) registration involves choosing a Aeps india, filling an application, and completing KYC by submitting documents (Aadhaar, PAN, bank details) for verification, followed by Aeps device setup (biometric scanner) and training to offer basic banking services like cash withdrawal, balance inquiry, and money transfers using Aadhaar and biometrics. The Aeps KYC process, especially crucial now with RBI’s stricter rules, ensures you’re a legitimate agent, requiring secure document submission and background checks before Aeps activation, with ongoing compliance needed.

AEPS Agent Registration & KYC Process

- Select a Provider: Choose a reliable AEPS provider like Aeps india offers secure Aeps software, support, and is government-approved.

- Application: Fill out the Aeps india registration form with your details and business information.

- Submit Documents (KYC): Provide copies of your Aadhaar Card, PAN Card, Bank Account details (with IFSC), and a photo for verification.

- Verification: The Aeps india and associated banks verify your documents and conduct a background check to ensure compliance.

- Hardware Setup: Install AEPS software on an internet-enabled device (phone/computer) and connect a compliant Aeps biometric device (fingerprint/iris scanner).

- Training: Receive training on the platform, transactions, and customer service.

- Activation: Your account gets activated after successful verification and training, allowing you to offer services like cash withdrawal, deposits, balance inquiries, and money transfers.

- Compliance: Maintain transaction records and follow regulatory guidelines, as audits are common.

Key Requirements

- Documents: Aadhaar Card, PAN Card, Bank Passbook/details, linked Mobile Number.

- Hardware: Biometric Device (fingerprint/iris scanner), Smartphone/POS machine.

- Internet: Stable internet connection for transactions.

Why KYC is Important

- Fraud Prevention: Stricter KYC, mandated by RBI, helps curb fraud in the AEPS network.

- Security: Ensures only legitimate agents provide services, protecting customer financial data.

- Legal Compliance: Fulfills regulatory requirements set by the Reserve Bank of India (RBI).

Benefits AEPS Service

AEPS (Aadhaar Enabled Payment System) benefits users by enabling secure, convenient banking services (cash withdrawal, deposit, transfer, balance check) in remote areas using only Aadhaar and biometrics, promoting financial inclusion, reducing travel to banks, and facilitating direct government benefit transfers, making banking accessible for the unbanked and underserved.

Key Benefits for Users

- Accessibility: Brings banking to rural areas via micro-ATMs and agents, eliminating long travel.

- Simplicity: Requires only your Aadhaar number and fingerprint/iris scan; no debit card or PIN needed.

- Security: Biometric authentication ensures secure, fraud-resistant transactions.

- Versatility: Perform cash withdrawals, deposits, fund transfers, and balance inquiries.

- Government Payments: Facilitates direct disbursement of welfare schemes (like pensions, MNREGA wages).

Benefits for Financial Inclusion & Economy

- Drives Inclusion: Extends formal banking to unbanked and underbanked populations.

- Digital Economy: Enables micro-merchants to accept digital payments easily.

- Cost-Effective: Reduces the need for extensive traditional banking infrastructure.

Read Blog : How to Choose the Best AEPS Portal Provider for Your Business

Features AEPS Service

AEPS (Aadhaar Enabled Payment System) features secure, bank-led basic banking services like cash withdrawal, deposit, fund transfer, balance inquiry, and mini statements, using just your Aadhaar number and biometrics (fingerprint/iris) for authentication, making it ideal for financial inclusion in remote areas without needing cards or PINs. It offers interoperability across banks, real-time processing, and facilitates government scheme payments, driving cashless transactions through micro-ATMs and banking correspondents.

Core Transaction Features

- Cash Withdrawal: Withdraw cash from your bank account.

- Cash Deposit: Deposit money into your linked account.

- Balance Inquiry: Check your account balance instantly.

- Mini Statement: Get recent transaction details.

- Fund Transfer: Transfer funds to other accounts.

- BHIM Aadhaar Pay: Facilitates payments using Aadhaar.

Key Security & Authentication Features

- Biometric Authentication: Uses fingerprint or iris scan for secure, fraud-resistant transactions.

- No Card/PIN Needed: Relies solely on your Aadhaar number and biometrics.

- Best Finger Detection: Enhances biometric accuracy.

Accessibility & Inclusion Features

- Interoperability: Access any bank account at any AEPS terminal.

- Rural Reach: Available at Banking Correspondents (BCs) and micro-ATMs in remote areas.

- Government Disbursement: Enables direct benefit transfers for welfare schemes.

Other Important Features

- Real-Time Processing: Transactions are processed instantly.

- eKYC & Aadhaar Seeding: Supports electronic Know Your Customer and checks seeding status.

- Tokenization: A security feature for data protection.

Steps to Start AePS Service

To start AEPS services, you need to register with a Aeps india, complete Aeps KYC verification (Aadhaar, PAN), get a compliant biometric device, integrate Aeps software/ Aeps app, and then you can offer services like cash withdrawal and balance checks by authenticating customers with their fingerprints, earning commissions on each transaction.

Here’s a step-by-step guide to becoming an AEPS agent:

1. Choose a Service Provider:

- Select a trusted and registered AEPS India .

2. Complete Registration & KYC:

- Fill out the AEPS India online form with your details, including bank info.

- Submit documents for KYC: Aadhaar, PAN, address proof, and a photo (ensure your Aadhaar is linked to a mobile number).

- AEPS India might require a Aeps video KYC or offer a free application process.

3. Acquire & Register Hardware:

- Obtain an approved biometric device (fingerprint scanner).

- Register the Aeps device with the Aeps india as instructed.

4. Integrate Software:

- Integrate the Aeps india AEPS admin platform/Aeps application into your mobile or POS system.

5. Start Transactions:

- Log in with your agent ID.

- For customers: Ask for their Aadhaar number, bank name, transaction type (withdrawal, balance inquiry), amount.

- Authenticate using the customer’s fingerprint (biometric authentication).

- Provide receipts and earn commissions.

Read Blog : AePS Advantages and Disadvantages: Complete Guide

Commission Structure in AEPS Service

AEPS commission structures offer retailers fixed amounts or percentages per transaction, Aeps india with higher earnings for larger cash withdrawals (e.g., ₹2-₹13+ per ₹100-₹3000+ withdrawal) and smaller fixed amounts for balance inquiries/mini statements (₹2-₹10). Aeps india offer tiered commissions, while some, like Airtel, offer higher percentages for premium plans, with commissions also available for fund transfers and other services.

Typical AEPS Commission Breakdown (Retailer Level)

Commissions are usually tiered and paid out per successful transaction, increasing with the transaction value.

Cash Withdrawal (Most Common)

- ₹100 – ₹999: Approx. ₹2.00

- ₹1,000 – ₹1,499: Approx. ₹3.00 – ₹4.50

- ₹1,500 – ₹1,999: Approx. ₹4.50 – ₹5.50

- ₹2,000 – ₹2,499: Approx. ₹5.50 – ₹7.00

- ₹3,000+: Can go up to ₹13 or more.

Other Services (Fixed Rates)

- Balance Inquiry: ₹2 – ₹10

- Mini Statement: ₹3 – ₹10

- Aadhaar to Aadhaar Fund Transfer: ₹5 – ₹15

Key Factors Influencing Commissions

- Service Provider: Best Aeps platforms Aeps India offer varying rates.

- Transaction Value: Higher value transactions generally yield higher commissions.

- Transaction Type: Cash withdrawal usually pays more than balance inquiry.

- Agent/Master Distributor Level: Distributors often earn a higher share.

Read Blog : AEPS Application: Complete Guide for Retailers and Businesses

AEPS Fund Transfer Using Aadhaar

AEPS (Aadhaar Enabled Payment System) allows you to transfer funds using just your Aadhaar number and biometrics (fingerprint/iris scan) at a banking correspondent or micro-ATM, linking your Aadhaar to your bank account for basic banking needs like fund transfers, cash withdrawal, and balance inquiry, facilitating financial inclusion without needing cards or PINs. To use it, visit an Aeps india, provide your Aadhaar, select ‘Fund Transfer’, choose the recipient’s bank/Aadhaar, enter the amount, and complete the transaction with a biometric scan for secure, real-time processing.

How AEPS Fund Transfer Works

- Link Aadhaar: Ensure your bank account is linked to your Aadhaar number.

- Visit Agent: Go to any AEPS-enabled shop or banking correspondent (BC) agent.

- Provide Details: Give the agent your Aadhaar number and select ‘Fund Transfer’ on their micro-ATM device.

- Select Transaction: Choose to transfer to another Aadhaar number (Aadhaar to Aadhaar) or account.

- Enter Amount & Bank: Input the amount and the recipient’s bank details.

- Biometric Authentication: Place your finger on the scanner for fingerprint or iris scan verification.

- Confirm: The system verifies your identity, processes the transaction, and provides a confirmation receipt.

Key Benefits

- Simplicity: No need for debit/credit cards, PINs, or internet banking.

- Security: Uses UIDAI’s secure biometric authentication.

- Accessibility: Available in remote areas via banking correspondents.

- Basic Banking: Offers cash withdrawal, deposit, balance inquiry, and mini statements too.

Aeps Cash Management Solutions

AePS Cash Management Solutions are services allowing secure, biometric-based banking (cash withdrawal, deposit, transfer, balance check) using only your Aadhaar number and fingerprint, especially crucial for rural/underbanked areas, enabling retailers to act as micro-ATMs for doorstep banking. These solutions, managed by Aeps india via AEPS payment API and POS devices, bring financial services closer to people, promoting financial inclusion by leveraging NPCI’s secure framework.

How AePS Cash Management Works (Merchant Perspective)

- Customer Approach: A customer visits an Aeps india website for banking needs.

- Transaction Selection: The merchant selects the service (e.g., cash withdrawal) on their Aeps admin portal/Aeps device.

- Biometric Authentication: Customer provides Aadhaar number, bank name, and authenticates with a fingerprint scan.

- Processing: NPCI processes the transaction securely.

- Cash Handled: Cash is dispensed (withdrawal) or accepted (deposit) by the merchant, who gets credited and earns commission.

Providers & Technology

- NPCI: The National Payments Corporation of India governs AePS.

- Agents/Distributors: Aeps India provide Aeps platforms (APIs, POS device) for retailers to offer these services.

Read Blog : How to Choose the Best AEPS B2B Software Provider for Your Business

Required Devices for AEPS Service

To offer AEPS (Aadhaar Enabled Payment System) services, you need essential devices: a smartphone/computer, a UIDAI-certified biometric device (fingerprint or iris scanner), a stable internet connection, and often a thermal printer, all running on a compatible Aadhaar Enabled Payment System application or Aeps panel to enable basic banking via Aadhaar authentication.

Essential Devices:

- Biometric Device: A STQC/UIDAI-certified fingerprint or iris scanner (like Mantra, Morpho) for customer identity verification.

- Internet-Enabled Device: A smartphone, laptop, or tablet to run the AEPS b2b software.

- Internet Connectivity: A reliable internet connection (Wi-Fi, dongle, or mobile data) is crucial for real-time transactions.

- AEPS Software/App: An Aeps admin application or Aadhaar Enabled Payment System portal from a Aeps india to access Aeps banking API.

Optional (but Recommended) Devices:

- Thermal Printer: For printing transaction receipts (often integrated Micro ATM).

- Micro ATM/POS Device: Compact machines combining biometric scanners, printers, and sometimes card readers for a complete Aeps setup.

Key Requirements for Agents:

- KYC Documents: Aadhaar, PAN, Bank Account, Photo.

- Established Location: A shop or business to serve customers.

- Bank Account Linked to Aadhaar: For the customer to perform transactions.

AEPS Service in Rural and Urban Areas

AEPS (Aadhaar Enabled Payment System) brings digital banking to rural areas by enabling cash withdrawals, deposits, and transfers via agents using just an Aadhaar card and fingerprint, promoting financial inclusion where banks are scarce. While primarily for rural access, it also serves urban users needing cardless, PIN-free banking, offering convenience and secure, biometric authentication for basic transactions at micro-ATMs or PoS terminals, bridging the urban-rural divide.

AEPS in Rural Areas (Primary Focus)

- Financial Inclusion: Bridges the gap by offering banking to remote locations without physical branches.

- Agent-Based Model: Banking correspondents (agents) in local shops provide services using micro-ATMs and biometric scanners.

- Services: Cash withdrawal, deposits, balance inquiry, fund transfers.

- Benefits: Reduces travel to distant banks, delivers government subsidies (like MGNREGA) directly, and boosts digital economy participation for small businesses.

AEPS in Urban Areas (Secondary Use)

- Convenience: Users without cards or PINs can access funds or make payments.

- Security: Biometric authentication (fingerprint/iris scan) offers enhanced security over PINs.

- Cardless Transactions: Eliminates the need to carry debit/credit cards for banking.

- Reach: Works anywhere with internet, extending basic banking beyond traditional urban ATMs.

Read Blog : Free AEPS Registration: Start Your Aadhaar Banking Business in 2025

AePS Service Challenges and Limitations

The Aadhaar Enabled Payment System (AePS) faces several challenges and limitations related to technology dependence, security vulnerabilities, limited services, and logistical issues in remote areas.

Service Challenges and Limitations

- Biometric Authentication Issues: A significant number of transactions fail due to poor fingerprint quality, especially among manual laborers or the elderly whose fingerprints may have worn down.

- Infrastructure & Connectivity Gaps: The system relies heavily on stable internet connectivity and a reliable power supply, which are often inadequate in the rural and remote regions where AePS is most needed.

- Security and Fraud Risks: Cybercriminals have exploited loopholes by using leaked biometric details to perform unauthorized transactions, raising concerns about data privacy and the security protocols at certain service points.

- Limited Awareness & Digital Literacy: Many potential users, particularly in rural areas, are unaware of the AePS service or lack the digital skills to use it safely, making them vulnerable to fraud or errors.

- Transaction Failures and Redressal Delays: High transaction failure rates, sometimes due to technical glitches or system errors, lead to customer frustration. In many cases, funds are debited but not disbursed, and the reversal process can take a significant amount of time (sometimes up to a month).

- Dependence on Aadhaar Number: Only individuals with an Aadhaar number linked to their bank account can use the service, which excludes those who do not possess this identification or have not linked it correctly.

Operational Limitations

- Basic Services Only: AePS is limited to fundamental banking services such as cash withdrawals, cash deposits, balance inquiries, and fund transfers. It does not support more complex financial needs like loan applications, insurance, or opening new accounts.

- Reliance on Business Correspondents (BCs): The availability of AePS services depends on a network of local agents or BCs equipped with micro-ATMs. The inconsistent availability of these agents in some areas can be a hurdle.

- Transaction Limits: Banks impose daily and per-transaction limits (typically ₹10,000 per transaction and around ₹50,000 daily) to prevent large-scale fraud, which may be restrictive for some users.

- Cost for Agents: Local agents bear the costs of purchasing and maintaining the necessary equipment (biometric scanners, micro-ATMs), which can sometimes lead to unofficial higher fees for users, especially in underserved locations.

Ongoing efforts to address these issues include stricter regulations, multi-factor authentication for high-value transactions, and the potential integration of advanced technologies like blockchain to enhance security and reliability.

Read Blog : Best AEPS API Providers in India for Startups and Retailers

Security and RBI Guidelines for AePS Service

The Reserve Bank of India (RBI) has significantly tightened security for AePS (Aadhaar Enabled Payment System) with new guidelines effective January 1, 2026, focusing on strict KYC for agents, continuous risk-based monitoring, stronger tech integration (EFRMS/SIEM), and exclusive b2b Aeps API use for AePS, all to curb fraud, enhance accountability, and build user trust through thorough agent due diligence, transaction surveillance, and mandatory Re-KYC for inactive operators.

Key RBI Security Guidelines (Effective Jan 1, 2026)

For AePS Operators (Agents/ATOs)

- Mandatory Full KYC: Banks must perform thorough KYC and background checks before onboarding any operator.

- Re-KYC for Inactive Agents: Operators inactive for 3 continuous months require a fresh KYC before resuming services.

- One Operator, One Bank: Each operator can now be linked to only one acquiring bank to prevent misuse.

- Strict API Control: Aeps Cash Withdrawal API used by operators must be exclusively for legitimate AePS operations, preventing unauthorized access.

For Acquiring Banks

- Enhanced Risk Monitoring: Implement risk-based controls, monitoring transaction volume, location, and patterns to flag suspicious activities.

- Tech Integration: Integrate AePS with Enterprise Fraud Risk Management Systems (EFRMS) and Security Information & Event Management (SIEM) for real-time alerts.

- Continuous Surveillance: Actively monitor ATO activities for anomalies and potential fraud.

- Grievance Redressal: Establish strong mechanisms for customer complaints and transparency.

For Customers

- Verify Service Points: Use only authorized, reliable AePS points.

- Secure Aadhaar Data: Keep your Aadhaar number and biometric data safe.

- Monitor Account: Regularly check bank statements for unauthorized transactions.

- Double-Check Details: Verify transaction details before confirming.

Why These Rules?

- Fraud Prevention: To address increasing fraud in biometric-based transfers.

- Accountability: To increase transparency and hold operators and banks responsible.

- Integrity: To maintain trust in the digital financial inclusion ecosystem.

How to Start AEPS Business

To start an AEPS business, you need to register with an approved AEPS software provider, complete your KYC with documents (Aadhaar, PAN, Bank details), obtain and install compliant hardware (biometric device/micro-ATM), and then integrate Aeps app to offer services like cash withdrawal, deposits, and balance checks, earning commissions while ensuring security and compliance.

Here are the step-by-step instructions:

1. Choose a Service Provider (BC/Aggregator)

- Select a reliable AEPS partner or Business Correspondent (BC) like Aeps India approved entities.

- Check their success rates, support, and compliance with UIDAI (Unique Identification Authority of India) and RBI (Reserve Bank of India) guidelines.

2. Complete Registration & KYC

- Fill out the Aeps india application form with your details.

- Submit required documents for KYC: Aadhaar, PAN card, Bank Account details, and sometimes a photo/Aeps video verification.

- Ensure your bank account is linked to your Aadhaar for transactions.

3. Acquire & Register Hardware

- Purchase a compliant biometric device (fingerprint scanner) or micro-ATM/POS terminal.

- Register Aeps device with your chosen Aeps india platform.

4. Software & Integration

- Install the AEPS b2b application on your computer or smartphone.

- This integrates Aeps system with your device for processing transactions.

5. Start Offering Services

- Authenticate Customers: Use their Aadhaar number and a thumbprint/iris scan.

- Provide Services: Offer cash withdrawal, deposits, balance inquiry, and potentially other services like bill payments and mobile recharge.

- Cash Management: Maintain your own cash float to disburse, as the Aeps india reimburses you later (T+1/T+2).

6. Ensure Compliance & Security

- Security: Protect customer data and use secure Aeps platforms.

- Receipts: Provide printed receipts for every transaction.

- Record Keeping: Maintain accurate transaction records.

- Training: Get trained on compliance and Aeps technology.

7. Market Your Services

- Promote locally via posters, social media, and word-of-mouth in your shop or area.

- Educate customers on the convenience and security of AEPS.

Support and Training Provided by AEPS India

Aeps India is the best AEPS service provider offer comprehensive support and training to individuals and businesses (retailers/agents) looking to provide AEPS services. This support helps agents set up and manage their AEPS business effectively.

Training Provided

Aeps india offer extensive training to ensure agents are well-versed in the system’s operation and compliance requirements. Key training areas include:

- AEPS Transaction Processes: Step-by-step guidance on how to perform various transactions like cash withdrawals, balance inquiries, and fund transfers.

- Biometric Device Handling: Instruction on acquiring, installing, and using UIDAI-certified Aeps biometric devices (fingerprint/iris scanners or face recognition technology) for authentication.

- Customer Service: Best practices for assisting customers, explaining the service’s benefits, and building trust in the community.

- Platform/Software Usage: Training on using the Aeps india specific web portal, mobile Aeps application, or Aeps admin dashboard for managing transactions, tracking commissions, and generating reports.

- Regulatory Compliance: Education on adhering to guidelines from the Reserve Bank of India (RBI) and the National Payments Corporation of India (NPCI) to ensure legal operation.

Support Offered

Aeps india offer ongoing support to minimize service disruptions and assist with any challenges. This support typically includes:

- 24/7 Technical Assistance: Accessible help (via phone, chat, or email) for troubleshooting technical glitches or device issues.

- Integration Support: Assistance with integrating AEPS API into existing Aeps business platforms or Aeps applications.

- KYC and Onboarding: A streamlined process for initial registration and Know Your Customer (KYC) verification, including document submission and background checks.

- Marketing Assistance: Aeps india offer promotional materials and guidance on marketing services locally to attract customers.

- Real-time Monitoring and Reporting: Access to Aeps dashboards for monitoring transactions, settlements, and agent performance.

By leveraging this support and training, individuals and small businesses can become authorized banking correspondents (BCs) or agents, offering essential financial services to underserved populations and generating a consistent income through commissions on each transaction.

Read Blog : Best AEPS Portals in India for Retailers and Startups

Get Aeps India Franchisee and Transform Banking Services with Aadhaar Micro ATM

To become a franchisee offering Aadhaar Micro ATM and banking services, you must partner with an authorized Aeps India business correspondent (BC) program. This low-investment business allows you to provide essential financial services in your community and earn commissions.

Steps to Become an Aadhaar Micro ATM Franchisee

- Meet the eligibility criteria: You must be an Indian national, at least 18 years old, and have a valid Aadhaar card and PAN card.

- Choose a service provider: You cannot connect directly to the National Payments Corporation of India (NPCI) system; you need to partner with a registered Aeps India.

- Register and complete KYC: Visit the Aeps India website or app, fill out the application form, and submit necessary documents like your Aadhaar card, PAN card, address proof, bank details, and a passport-sized photo for verification.

- Acquire and set up equipment: Purchase a compatible, STQC/Aadhaar certified biometric device (fingerprint or iris scanner) and the micro ATM terminal from Aeps India. You also need a smartphone/computer and internet connectivity.

- Receive training: The Aeps India will offer training on how to operate the device and manage transactions.

- Stock cash: You will need to have sufficient physical cash on hand to meet customer withdrawal demands.

- Start providing services: Once your account is activated and verified, you can begin offering services like cash withdrawals, balance inquiries, and fund transfers to customers.

Services Offered via Aadhaar Micro ATM

As a franchisee, you can offer crucial banking services, primarily under the Aadhaar Enabled Payment System (AEPS):

- Cash withdrawals

- Balance inquiries

- Cash deposits (offered by some platforms)

- Aadhaar-to-Aadhaar fund transfers

- Mini statements

- Utility bill payments and mobile recharges (often available as additional services from the provider).

Benefits of the Franchise Model

- Income generation: Earn attractive commissions on every successful transaction.

- Low investment: Compared to traditional ATMs, micro ATMs require minimal initial investment.

- Financial inclusion: Bring essential banking services to underserved, remote, and rural communities.

- Increased business: Offering banking services can increase foot traffic to your existing shop or business, potentially boosting sales of other goods/services.

- Security: Transactions use secure biometric authentication, building trust in the financial system.

For more information, you can explore the Aeps india website or app.

Read Blog : How to Activation Aeps Service in India: Step-by-Step Guide

How to Choose AePS Service Provider

Aeps india is an AEPS Aadhaar Enabled Payment System provider, prioritize NPCI/RBI certification, security (biometrics, encryption), and high transaction success rates for reliability, alongside a user-friendly platform, transparent commissions, multi-bank support, and excellent 24/7 customer support, ensuring they offer good reporting and scalability for your business needs.

Key Factors to Consider

Regulatory Compliance & Security:

- NPCI/RBI Certified: Must be an authorized Aeps india is an Aeps Payment System Provider or Business Correspondent (BC) with direct NPCI certification.

- Security Features: Look for Aadhaar biometric authentication, end-to-end encryption, and strict data privacy protocols.

Performance & Reliability:

- High Success Rate: Aim for 98%+ transaction success rates and minimal downtime.

- Multi-Bank Support: Ensure they support a wide range of banks for better customer reach.

Cost & Commission:

- Transparent Structure: Understand the commission earned and any associated fees clearly.

- Competitive Rates: Compare commission rates for better earnings.

Platform & Technology:

- User-Friendly Interface: Easy for agents and customers to use.

- Seamless Integration: Good documentation for Aeps API integration if needed.

- Scalability: Can the Aeps b2b platform grow with your business?.

Support & Reporting:

- 24/7 Support: Responsive technical and customer support is crucial for resolving issues quickly.

- Detailed Reporting: Real-time transaction reports, settlement summaries, and commission statements.

Why Choose a Aeps India for AePS Service solution

Choosing an AEPS solution in India offers deep financial inclusion by bringing banking to rural areas via biometric security, eliminates the need for cards/PINs, supports diverse transactions (cash withdrawal, deposit, transfer), and provides cost-effective Aeps india, making it ideal for the underbanked, agents, and small businesses to access digital finance securely and conveniently.

For Customers & Rural Users:

- Financial Inclusion: Banks reach remote villages where ATMs and branches are scarce, serving the unbanked population.

- Ultimate Convenience: Just need your Aadhaar number and fingerprint/iris scan; no cards, PINs, or smartphones required.

- Enhanced Security: Biometric authentication is highly secure, preventing fraud and PIN theft.

- Versatile Services: Perform cash withdrawals, deposits, balance checks, and fund transfers at local agents.

For Agents & Businesses (Retailers/Entrepreneurs):

- New Revenue Stream: Earn commissions on every transaction (withdrawal, deposit, etc.).

- Low Investment: Requires minimal capital (smartphone, internet, biometric device) to start.

- Easy to Operate: User-friendly interface, minimal training needed to offer banking services.

- Attracts Customers: Adds value to your shop, bringing more footfall and business.

For Banks & Providers:

- Cost-Effective Expansion: Reduces the need for expensive physical branch networks.

- Increased Reach: Leverages existing networks of Business Correspondents (BCs) for last-mile delivery.

- Secure & Compliant: Utilizes NPCI-certified Aeps india, encrypted Aeps platforms, ensuring safe transactions.

Read Blog : Best AEPS Integration Providers in India 2025

Future Trends of AePS Service

The future trends for the Aadhaar Enabled Payment System (AePS) are primarily focused on enhanced security measures, deeper integration with the broader digital finance ecosystem (like UPI), and an expansion of services to drive further financial inclusion across India.

Key trends shaping the future of AePS include:

Technological Advancements & Security

- Advanced Biometrics and Liveness Detection: To combat fraud, future AePS will likely incorporate more sophisticated biometric methods, potentially including AI-enhanced fingerprint matching and multi-modal biometrics, along with mandatory liveness detection.

- AI and Machine Learning (AI/ML): AI and ML are expected to be used for real-time fraud detection and analysis of user behavior patterns.

- Blockchain Integration: Exploration of blockchain technology is underway to enhance transparency and security in transaction records.

- Improved User Experience: Aeps software Development will focus on creating mobile friendly Aeps interfaces to make the system easier to use for everyone.

Service Expansion and Integration

- Integration with UPI and Digital Wallets: AePS is anticipated to integrate more closely with UPI and digital wallets, aiming for a more connected financial system.

- Multi-Service Hubs: Retail agents are expected to offer a broader suite of services beyond just basic banking, potentially including utility bill payments (BBPS) and mobile recharges.

- Embedded Finance: There is a potential for AePS functions to be integrated into non-financial applications to make financial services more accessible.

Regulatory and Market Shifts

- Stricter RBI Regulations: New regulations from the RBI, effective January 1, 2026, will require enhanced due diligence and stricter KYC procedures for AePS operators.

- Expansion of Rural Infrastructure: Growth in micro-ATMs and business correspondent networks is anticipated to extend banking services to underserved populations.

- Government Initiatives: AePS will continue to be important for distributing government benefits directly to Aadhaar-linked accounts.

Overall, AePS is evolving beyond a simple withdrawal system to become a key element in India’s digital economy, driven by technological advancements, regulatory changes, and an expanded range of integrated financial services.

Conclusion

The AePS service in India has become an important part of the country’s digital banking system. It allows people to access basic banking services like cash withdrawal, balance enquiry, and mini statement using only their Aadhaar number and biometric authentication. This makes banking simple, fast, and accessible, especially in rural and semi-urban areas where bank branches are limited.

AePS (Aadhaar Enabled Payment System) Services allow users to perform basic banking transactions like cash withdrawal, deposit, fund transfer, and balance inquiry using only their Aadhaar number and biometric (fingerprint/iris) authentication, making banking accessible at micro-ATMs or agent points without needing cards or PINs, primarily benefiting rural and unbanked populations.

For retailers, CSPs, and banking correspondents, AePS services offer a strong opportunity to start a low-investment and steady-income business. By providing Aadhaar-based banking services, agents can serve more customers daily, build trust in their locality, and earn regular commission on every transaction.

The AePS system in India is secure, RBI-compliant, and supported by NPCI, ensuring safe transactions and real-time settlements. When used with a reliable Aeps platform, AePS helps improve financial inclusion and strengthens digital payment infrastructure across the country.

Aeps india is the right AePS service provider in India is key to long-term success. With the right technology and support, AePS can help businesses and agents offer seamless digital banking services, grow their customer base, and succeed in India’s fast-growing fintech ecosystem.

Frequently Asked Questions (FAQs) – AEPS Service in India

AEPS service in India stands for Aadhaar Enabled Payment System, which allows customers to access basic banking services using their Aadhaar number and biometric authentication. It helps people perform cash withdrawal, balance enquiry, and mini statement services without visiting a bank branch.

AEPS services can be used by bank customers, retailers, CSPs, banking correspondents, and digital service centers. Any customer with an Aadhaar-linked bank account can use AEPS services easily.

The AEPS system offers services like cash withdrawal, balance enquiry, mini statement, and Aadhaar-based fund access. These services work in real time and support multiple banks across India.

Yes, AEPS service in India is safe as it uses biometric verification and encrypted data. Transactions are processed under NPCI guidelines, ensuring high security and protection against fraud.

To start an AEPS service business, agents need Aadhaar card, PAN card, a linked bank account, a registered mobile number, and a biometric device with a stable internet connection.

Agents earn commission on every successful AEPS transaction, especially on cash withdrawals and balance enquiries. Higher transaction volume leads to higher daily income.

Yes, AEPS service supports most major banks in India as long as the customer’s Aadhaar is linked with their bank account.

AEPS service in India brings banking services to remote areas where bank branches and ATMs are limited. It improves financial inclusion and saves time for customers.

Yes, AEPS services are widely used in rural and semi-urban areas, where banking access is limited. It helps people access money easily.

Yes, a stable internet connection is required to complete AEPS transactions smoothly.

Retailers can start by registering with AEPS India, completing KYC, and activating their AEPS account to begin offering services.

Best AEPS Provider in India for Retailers

Biometric AEPS API: Complete Guide