AEPS Portal Company: Features, Benefits, Pricing & Business Opportunities in 2026

Are you looking for the best AePS portal company in India to start your online banking and digital payment business? If yes, then you are in the right place. Today, the demand for AePS online banking solutions is growing rapidly because customers want fast, secure, and easy banking services without visiting a bank branch.

The Aadhaar Enabled Payment System (AePS) allows retailers and businesses to provide services like cash withdrawal, balance enquiry and mini statement using Aadhaar authentication. This makes digital banking simple and accessible for customers in both rural and urban areas.

With the help of a trusted AePS API provider like Aeps india, retailers can offer secure banking services and earn commission on every transaction. This creates a strong opportunity to build a profitable AePS business in India with low investment and high earning potential.

One of the biggest advantages of using an AePS portal solution is that businesses can start with low investment and expand quickly in the growing fintech industry. AePS services also support financial inclusion by making banking accessible to people in remote areas.

A reliable Aeps platform like AEPS India provides advanced AePS portal solutions with secure Aeps API integration, high transaction success rate, fast processing, and user-friendly Aeps dashboard management. This helps retailers and businesses manage their online banking services smoothly while increasing customer trust.

Choosing the right AePS portal company is important for long-term business growth. Aeps india offers strong technical support, secure payment systems, and scalable Aeps solutions to help businesses grow faster in the digital banking industry.

At Aeps India, we provide advanced and secure AEPS portal development, AEPS API, white label Aeps software, and online Aeps banking API solutions designed for retailers, distributors, startups and fintech companies. Our Aeps solution focus on high transaction success rates, strong security, easy dashboard management, and smooth Aeps API integration for long-term business growth.

In this blog, you will learn everything about the best AePS portal company for online banking solutions, its features, benefits, business opportunities, and how to start AePS business successfully.

What is an AEPS Portal Company?

An AEPS Portal Company is a Aeps india that develops and manages Aeps software platform allowing agents, retailers and small businesses to offer basic banking services like cash withdrawals, deposits and balance inquiries using only a customer’s Aadhaar number and fingerprint.

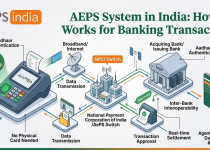

AEPS Portal Company Work

An Aadhaar Enabled Payment System portal is a Aeps banking platform that allows individuals to perform cardless transactions using only their Aadhaar number and biometrics (fingerprint or iris scan). It turns local shops into “micro ATM” helping agents earn commissions on transactions like cash withdrawals, balance inquiries and fund transfers.

How the Portal Works

The process connects local merchants to the national banking grid. Here is the step-by-step transaction flow:

- Initiation: The customer visits a local agent or Business Correspondent (BC) and provides their 12-digit Aadhaar number and bank name.

- Selection: The agent selects the required service on the Aeps portal or Aeps app (e.g., cash withdrawal or mini-statement).

- Authentication: The customer scans their finger or iris on a Aeps biometric device connected to the agent’s device.

- Verification: The portal sends the encrypted biometric data to the UIDAI (Unique Identification Authority of India) and the customer’s bank for instant verification.

- Completion: Once authorized, the transaction is completed, the agent dispenses the cash, and both parties receive real-time confirmation.

Services Offered Through AePS Portal

The Best Aadhaar Enabled Payment System (AePS) is a bank-led model that allows users to perform basic financial transactions at authorized banking correspondent outlets using just their Aadhaar number and biometric authentication (fingerprint or iris scan).

The core services offered through an Best AePS portal include:

- Cash Withdrawal: Allows customers to withdraw money directly from their Aadhaar-linked bank accounts via a local business correspondent or micro ATM device.

- Balance Enquiry: Enables users to check their current bank account balance in real-time.

- Mini Statement: Provides a quick overview of recent transactions, typically the last 5 to 10 entries in the account.

- Cash Deposit: Allows customers to deposit cash directly into their Aadhaar-linked bank accounts through an agent.

- Aadhaar to Aadhaar Fund Transfer: Facilitates direct transfers from one Aadhaar-linked bank account to another.

- Aadhaar Pay: Acts as a merchant payment solution, allowing customers to pay for goods and services directly from their bank account via biometric authentication.

Documents Required for AEPS Retailer Registration

To register AePS retailer, you will need to provide standard KYC (Know Your Customer) documents for identity, address and business verification.

Core Documents Required

- Identity Proof: Aadhaar Card and PAN Card.

- Address & Business Proof: Shop & Establishment Certificate, GST Registration, Udyam Registration, or a recent utility bill (electricity/water).

- Banking Details: A cancelled cheque, bank passbook front page, or a recent bank statement for commission settlements.

- Contact Information: An active, Aadhaar-linked mobile number and a working email address.

- Photographs: Recent passport-sized photographs.

Technical Equipment Needed

In addition to the paperwork, you will need to arrange specific hardware to operate the service:

- Smartphone/Computer: An Android device or PC with a stable internet connection.

- Biometric Device: A UIDAI/STQC-certified fingerprint scanner (e.g., Mantra).

Why Use AEPS Portal

An Best Aadhaar Enabled Payment System portal is a banking system that lets you perform basic transactions like cash withdrawals and balance checks using only your Aadhaar number and fingerprint, removing the need for debit cards or PINs.

Why Use an AEPS Portal?

The Aeps system is heavily used in India by both individuals for banking and local shop owners for business:

- Cardless & PIN-less Banking: You do not need to carry a physical debit card or remember a PIN. Your unique Aadhaar number combined with biometric (fingerprint) authentication serves as your digital signature.

- High Accessibility & Convenience: It brings essential banking services (cash withdrawals, balance inquiries, mini statements) directly to your local neighborhood, which is especially vital in rural or unbanked areas where ATMs are scarce.

- Government Benefit Transfers (DBT): It makes it incredibly easy to withdraw government subsidies, pensions, or MGNREGA funds directly from your Aadhaar-linked bank accounts.

- Interoperable: You can access your bank account at any authorized micro-ATM or banking correspondent, regardless of which bank your account is held with.

- High Security: Because transactions require a live fingerprint scan, it reduces the risk of fraud associated with lost physical cards or stolen PINs.

Who Can Use AEPS Portal

The Aadhaar Enabled Payment System (AEPS) can be used by two main groups: everyday banking customers needing basic transactions and authorized agents acting as micro-ATMs.

1. Bank Customers (As Users)

Any Indian resident can use best AEPS services to manage their finances without needing a debit card or PIN.

- Requirements: An active bank account that is linked to a 12-digit Aadhaar number, and registered biometric data (fingerprint or iris scan) with UIDAI.

- Who it benefits: Rural populations, underserved areas, and government beneficiaries receiving Direct Benefit Transfers (DBT) like pensions or MGNREGA wages.

2. Retailers & Agents (As Service Providers)

Small business owners and operators use dedicated top AEPS portal to provide banking services to their local communities, earning commissions on each transaction.

- Who can be an agent: Kirana store owners, pharmacists, Common Service Center (CSC) operators, and authorized Business Correspondents (BCs).

- Requirements: A valid PAN card, Aadhaar card, a registered mobile number, an approved buy Aeps biometric device (like a fingerprint scanner), and a stable internet connection.

To get started as a merchant, agents can register through authorized Aeps india such as those listed or other verified Aeps admin portal.

Top Use Cases of AEPS Portal Company

An AEPS portal company like Aeps india turns local retail shops into “mini-banks” by enabling secure, cardless transactions using biometric authentication. These Aeps platform primarily bridge financial gaps in unbanked regions, facilitate government subsidies and allow local merchants to process digital payments without hardware terminals.

The top use cases of an smooth AEPS portal include:

- Cash Withdrawals & Deposits: Enables customers to instantly withdraw or deposit funds into their Aadhaar-linked bank accounts at neighborhood stores, removing the need to travel long distances.

- Balance Inquiry & Mini-Statements: Allows users to check their real-time account balance and print or view recent transaction summaries via a simple fingerprint or face scan.

- Direct Benefit Transfer (DBT): Streamlines the distribution of government subsidies, pensions, and welfare funds so citizens can seamlessly access government payments.

- Aadhaar Pay (Merchant Payments): Empowers small local merchants to accept digital payments directly from a customer’s bank account using only their Aadhaar and biometrics, avoiding traditional point-of-sale (POS) machine fees.

- Aadhaar-to-Aadhaar Fund Transfers: Facilitates the secure movement of money from one Aadhaar-linked bank account to another.

- eKYC & Identity Verification: Provides paperless, instant Know Your Customer (KYC) verification for businesses and banking institutions to securely Aeps onboard customers.

Key Aspects of AEPS Portal Company

An Aadhaar Enabled Payment System portal company like Aeps india provides a secure, bank-led Aeps admin platform that allows customers to perform basic banking transactions using just their Aadhaar number and biometric authentication. It primarily empowers local merchants and rural agents to offer micro ATM services, driving financial inclusion across India.

Core Banking Services

- Cash Withdrawal: Allows customers to withdraw cash from their bank accounts directly at a local agent or Business Correspondent (BC) outlet.

- Balance Inquiry & Mini-Statements: Agents can instantly check a customer’s account balance and provide mini-statements to track recent activities.

- Cash Deposits: Select b2b Aeps portal allow customers to deposit cash into their Aadhaar-linked accounts at authorized agent points.

Technology & Security

- Biometric Authentication: Transactions are verified using unique fingerprint or iris scans, eliminating the need for physical debit cards, PINs, or OTPs.

- Nationwide Interoperability: Customers can transact with their specific bank accounts at any authorized agent point, regardless of the bank the agent is affiliated with.

- Certified Devices: Requires agents to use registered Aeps biometric L1 devices and smartphones/buy micro ATM compliant with NPCI and UIDAI security guidelines.

Agent Benefits & Business Models

- Commission Income: Agents and retailers earn attractive per-transaction commissions (ranging from ₹2 to ₹15+ depending on the transaction volume and provider).

- Instant Settlements: Aeps india offer instant (T+0) or same-day (T+1) fund settlements, ensuring agents maintain healthy cash flow and liquidity.

- White-Label Solutions: Aeps india offer white label Aeps portal development, enabling new businesses or banking facilitators to establish their own branded AePS platform and best Aeps API networks.

Online Banking Solutions with AEPS Portal

Online banking solutions with an high performance AePS portal allow merchants and agents to offer basic financial services such as Aeps cash withdrawal service, Aeps balance inquiry service and Aeps mini statement service using only a customer’s Aadhaar number and biometric authentication. These Aeps service portal are vital for rural financial inclusion.

Core Features of AePS Portals

- Biometric Authentication: Transactions are verified using a Aeps fingerprint scanner or IRIS scan.

- Cash Withdrawals: Customers can withdraw money from their Aadhaar-linked bank accounts without needing a debit card.

- Balance Inquiry & Mini Statements: Quick real-time lookups to check account health.

- Agent Commissions: Retailers earn daily commission credits in their digital wallets for facilitating these services.

Key Transaction Limits & Security

- Transaction Cap: Transactions are typically capped at Rs. 10,000 per transaction, subject to a monthly limit of Rs. 50,000 (though limits can vary depending on individual bank policies).

- Security: Transactions are routed through the NPCI (National Payments Corporation of India), ensuring safety through mandatory multi-factor biometric matching.

Role of AEPS Portal in Financial Inclusion

The top AePS is a bank-led model that allows users to perform basic financial transactions using just their Aadhaar number and biometric authentication. It plays a crucial role in financial inclusion by bringing doorstep banking to rural, unbanked populations without requiring debit cards, PINs, or smartphones.

Key Pillars of AePS in Financial Inclusion

- Doorstep Banking: By operating through local Business Correspondents (BCs) and Best Micro ATM device, AePS eliminates the need for individuals in remote villages to travel long distances to reach physical bank branches.

- No Barrier to Entry: It provides banking access to the illiterate or digitally marginalized, as transactions are authorized using a fingerprint or iris scan rather than remembering complex passwords or carrying cards.

- Direct Benefit Transfers (DBT): AePS ensures that government subsidies, pensions, and welfare funds reach beneficiaries directly and securely, reducing leakages and delays.

- Essential Services: Users can easily perform core banking functions, including cash withdrawals, cash deposits, balance inquiries, and mini-statement generation.

- Enhanced Security: Relying on biometric data minimizes the risks of fraud and theft associated with traditional cash handling.

AEPS Portal for Retailers, Distributors & CSP Agents

An AEPS commission portal empowers local shops, distributors, and Customer Service Points (CSPs) to turn into “mini-banks”. By utilizing customer biometric data, these Aeps portal facilitate seamless financial transactions in local communities.

Essential Services Provided

- Cash Withdrawals: Customers can withdraw cash using their Aadhaar number and Aeps fingerprint scan.

- Balance Inquiry & Mini Statements: Fast and secure checking of linked bank accounts.

- Aadhaar Pay & Fund Transfers: Cardless and PIN-less merchant transactions and intra Aadhaar transfers.

- Bill Payments & Recharges: Additional utility services and recharges to increase footfall.

Business Tiers & Opportunities

- Retailers/Agents: Kirana stores, pharmacies, and local shop owners act as business correspondents, earning commissions (typically ₹7 to ₹15+ per transaction) directly into their wallets.

- Distributors: Manage networks of retail agents. They earn override Aeps commission on their agents’ transaction volumes and typically manage localized support and liquidity.

- Master Distributors & Fintechs: Aeps india looking to build their own brand can utilize White Label AEPS platform and Aeps API integrating to run their own comprehensive Aeps administrative portal.

Why AePS Portal is Important for Online Banking Solutions

An AePS earning portal is crucial for online banking solutions because it enables cardless, PIN-less, biometric-based banking. By eliminating the need for physical debit cards or smartphones, it empowers unbanked and rural populations to easily access basic financial services, including Aeps cash withdrawal API, Aeps balance inquiry api and Aeps mini statement API.

Key Reasons Why AePS Portals Are Important

- Drives Financial Inclusion: It bridges the digital divide by allowing individuals in remote, underserved areas to access formal banking at local agent outlets (Business Correspondents) without traveling to distant bank branches.

- Cardless & PIN-less Security: Transactions require only an Aadhaar number and a fingerprint or iris scan. This eliminates the risk of forgotten PINs, lost debit cards, or card fraud.

- Facilitates Government Subsidies: It ensures that citizens can instantly withdraw Direct Benefit Transfers (DBT) and welfare schemes as soon as the funds are credited to their Aadhaar-linked bank accounts.

- Empowers Local Businesses: Integrating AePS portal transforms local shops and retailers into mini-banks. Agents can provide financial services to their community while earning a steady stream of daily commissions per transaction.

Why Businesses Need an AePS Portal

An High volume AePS portal allows businesses to process banking and payment transactions securely using just an Aadhaar number and biometric authentication (like a fingerprint scan).

Businesses need an Highest earning AePS portal because it transforms local shops into mini-banks, driving higher footfall and unlocking the following advantages:

1. New Revenue Streams

Every AePS transaction (such as cash withdrawals or balance inquiries) generates a steady, commission-based income for the business owner. It turns routine banking into an additional source of daily revenue.

2. Cardless and PIN-less Convenience

Customers can make payments or withdraw cash without needing a physical debit/credit card or remembering a PIN. This is highly convenient for populations that lack access to traditional banking facilities or have misplaced their cards.

3. Increased Customer Footfall

By acting as a neighborhood best micro ATM system, a business naturally attracts a wider customer base. People visiting to check balances or withdraw cash are much more likely to purchase goods and services from the shop simultaneously.

4. High Security

AePS relies on live biometric verification (like fingerprint scanning) against the central UIDAI database. This drastically reduces the risk of identity theft, card skimming, or fraud compared to traditional card-based transactions.

5. Seamless Financial Inclusion

For small and micro-businesses operating in rural or semi-urban areas, AePS provides an essential service to the community. It helps the unbanked access basic financial services, such as checking mini-statements or doing Aadhaar-to-Aadhaar fund transfers, right at the counter.

Features AEPS Portal Company

An Secure AEPS portal allows merchants and agents to act as banking correspondents, enabling customers to conduct basic, cardless banking transactions using only their Aadhaar number and fingerprint or iris scan.

Core Financial Services

- Cash Withdrawal & Deposit: Allows customers to withdraw or deposit cash directly from their linked bank accounts instantly.

- Balance Inquiry & Mini-Statements: Provides real-time account balance checks and prints or displays recent transaction logs.

- Aadhaar Pay / Merchant Transactions: Enables customers to pay merchants directly through their Aadhaar number, often unlocking higher transaction limits than standard cash withdrawals.

- Aadhaar-to-Aadhaar Fund Transfers: Direct transfers between two Aadhaar-linked accounts.

Technical & Security Features

- Cardless and PIN-less: Eliminates the need for debit/credit cards, ATM PINs, or OTPs.

- Secure Biometric Authentication: Transactions are authorized using fingerprint or iris scans verified against UIDAI records, minimizing fraud risks.

- Interoperability: Customers can access their bank accounts through any authorized AEPS agent, even if the agent is affiliated with a different bank.

- Real-Time Processing & Instant Settlements: Provides immediate transaction confirmation and instantaneous settlement (T+0) of commissions into the agent’s digital wallet.

Admin & Business Features

- Multi-Bank Support: Compatible with hundreds of major Indian banks for inclusive, countrywide coverage.

- Role-Based Access Control: Allows white label Aeps admin panel to assign sub member IDs and distribute work plans to employees or downline agents.

- Analytics & Reports: Detailed dashboard tracking for daily sales, commission tracking and pending transaction queues.

- Value-Added Services (VAS): Often includes integrated utility features like mobile/DTH recharge API, BBPS API, and Micro ATM machine support.

Benefits AEPS Portal Company

An powerfull AEPS portal empowers businesses to turn retail shops into “mini-banks”. For Aeps b2b portal-owning Aeps india, key benefits include high per-transaction commissions (₹5–₹15+), increased customer footfall, and the ability to offer secure, cardless banking to underrepresented rural populations.

Key Benefits for AEPS Portal Companies & White-Label Providers

- Lucrative Revenue Streams: Companies earn Aeps commissions on every transaction (withdrawals, Aeps balance inquiry services, and Aeps mini statement API services). Higher-value transactions generate higher margins, making it a highly profitable enterprise.

- Instant Settlement & Liquidity: Modern Aeps portal feature instant

𝑇

+0 settlement, which drastically improves cash flow for micro-merchants and distributors under the Aeps india network.

+0 settlement, which drastically improves cash flow for micro-merchants and distributors under the Aeps india network. - Rapid Network Growth: Aeps india can rapidly expand their Aeps india network by offering best Aeps platform. This allows partners to build their own brand AEPS portal without heavy initial Aeps software development costs.

- Reduced Overhead Costs: For financial institutions and NBFCs, adopting AEPS reduces physical dependency on ATMs and branches, which cuts down operating and cash-handling expenses.

- Direct Benefit Transfer (DBT) Reach: Aeps india facilitate essential government subsidies, pensions, and MNREGA payouts, building massive trust and consistent utility among rural customers.

Key Benefits for Retailers (Agents)

- Guaranteed Income: Agents earn a stable, daily Aeps commission for every successful Aadhaar and fingerprint-authenticated transaction.

- Increased Customer Footfall: By providing critical banking services locally, retailers bring in a wider demographic, which boosts secondary sales at their primary retail shop.

- Zero Card & PIN Hassles: Customers only need their Aadhaar number and biometrics to transact, minimizing the risks and frustrations of lost physical debit cards or forgotten PINs.

- Unmatched Security: Biometric authentication (fingerprint or iris) minimizes the risk of digital fraud, preventing unauthorized access even if the customer’s mobile device is compromised.

- Interoperable Access: Customers can securely access any bank account via the agent’s purchase micro ATM or standard Aeps portal, regardless of the bank they are registered with.

AEPS API Integration and Software Solutions

AEPS API integration allows businesses to process biometric banking transactions such as cash withdrawals, balance inquiries, and mini-statements using an Aadhaar number. The Aeps integration involves partnering with an NPCI-certified Aeps india, passing compliance, linking hardware and writing code to securely capture and transmit biometric data.

Key Steps to Integrate AEPS API

Select a Certified AEPS Provider:

- Partner with an NPCI-certified Aeps india. Ensure they comply with current regulatory guidelines, including the mandatory “One Operator, One Bank” rule.

Business Registration & Full KYC:

- Submit your business documents (PAN, GST, and corporate bank details) to the Aeps india. Complete the mandatory full KYC verification for your business entity to get authorized.

Acquire & Register Biometric Devices:

- Purchase L1 certified Aeps Devices (RD) compliant with the Aeps india SDK (e.g., Mantra). Register the device on the respective RD best Aeps service portal before use.

Obtain API Credentials:

- Once approved, Aeps india will provide you with the necessary developer keys such as a Aeps Merchant ID (MID), Secure Aeps API Key, and detailed Aeps API documentation/SDKs.

Technical Integration (Frontend & Backend):

- Capture Stage: Trigger the RD Service on the user’s device (Windows or Android) to capture the customer’s fingerprint.

- Payload Construction: Format the captured biometric data into an encrypted payload (PidData).

- API Call: Send the payload via HTTPS POST to the Aeps india endpoint. Required parameters typically include the Aadhaar number, bank IIN (Identification Number), transaction type, and unique transaction ID.

Sandbox Testing:

- Thoroughly test all transaction workflows (Cash Withdrawal, Balance Enquiry) using dummy data in the provider’s Sandbox environment. Verify the security and callback URL handling for success/failure transaction statuses.

Go Live:

- Deploy Aeps application to production. Complete any final compliance checks mandated by the Aeps india and begin offering top AEPS services to your customers.

AEPS Portal Development and Setup Guide

Developing and setting up an High speed AEPS portal requires integrating with an NPCI-certified Aeps india, submitting business KYC, and sourcing UIDAI-certified Aeps biometric hardware. Follow this step-by-step guide to launch Aeps B2B or merchant AEPS platform.

1. Essential Prerequisites

Before starting Aeps portal development, ensure you have the following in place:

- Operating Device: Android smartphone (version 7.0+) or Windows PC/laptop.

- Connectivity: Stable internet connection (Broadband or 4G/5G mobile data).

- Hardware: STQC certified Aeps biometric device (e.g., Mantra) with functional Registered Device (RD) Service.

2. Choose an AEPS Service Model

You can build Aeps portal in two ways:

- White-Label AEPS Solution (Recommended): Partner with an established AEPS India. They provide pre-built, compliant Top Aeps platform with fast Aeps API integration, saving you months of Aeps software development company time and direct NPCI compliance costs.

- Direct API Integration: Build Aeps admin portal from scratch and integrate AEPS API directly from a Aeps india. This requires significant technical Aeps application development and strict regulatory clearances.

3. Registration and KYC Verification

Register your business entity with your chosen Aeps india. You will typically need to submit the following documents:

- Personal KYC: Aadhaar card and PAN card.

- Business Proof: Shop & Establishment Certificate, Udyam Registration, or GST Certificate.

- Financials: Cancelled cheque or bank passbook for daily settlement.

4. Technical Integration & Development (If building from scratch)

If you are developing Aeps software using an Aeps india, your technical team must implement:

- Secure API Keys: Implement secure communication protocols (HTTPS/SSL) and encrypt biometric data end-to-end to prevent data breaches.

- RD Service Integration: Integrate with the UIDAI RD Service to capture and encrypt fingerprints dynamically.

- Multi-Factor Authentication: Ensure each transaction requires the customer’s Aadhaar number, bank IIN (Issuer Identification Number), and fingerprint authentication.

5. Portal Activation

Once development or white label Aeps customization is complete:

- Test Aeps portal transaction flow (Cash Withdrawal, Balance Inquiry, and Mini-Statements).

- Install the hardware’s RD service on your devices.

- Activate Aeps Agent ID and Aeps Merchant Dashboard to begin offering doorstep banking services.

Aeps Portal Cost Structure

An AEPS portal cost depends on your business model. Retailers and sub-agents can start for free to ₹3,000. Businesses launching an independent powerfull Aeps platform (White Label Aeps api or custom Aeps API) typically pay ₹12,000 to ₹4,500,000+ in Aeps setup fees, alongside ongoing transaction and maintenance charges.

The specific cost structure breaks down by business type, hardware, software, and operational fees:

1. Business and Software Costs

- Retailer / Agent ID: Aeps india provided for free or for a nominal fast Aeps setup fee (₹99 – ₹3,000) by master distributors.

- White-Label Portal: A branded, pre made Aeps B2B portal costs between ₹15,000 and ₹1.2 Lakh+. This allows you to create your own sub-agents.

- Custom API Integration: Building a custom AEPS platform from scratch, including high-end direct Aeps bank API integrations (e.g., ICICI or Yes Bank), ranges from ₹1 Lakh to ₹4.5 Lakh+.

2. Hardware and Setup Fees

- Biometric Devices: You need an STQC-certified L1 or L2 fingerprint/iris scanner (e.g., Mantra). These cost ₹1,500 to ₹3,000.

- Setup/Integration Fees: One-time charges to integrated AEPS API into an existing system typically run ₹12,000 to ₹35,000.

3. Recurring and Maintenance Fees

- Annual Maintenance Charges (AMC): Aeps Software typically charge ₹10,000 to ₹1 Lakh+ per year for server upkeep, security and updates.

- Settlement Fees: Small flat charges or percentage fees applied when you transfer your daily earnings Aeps portal to your primary bank account.

4. Transaction Charges & Commissions

- Consumer Charges: End-users are generally charged ₹5 to ₹20 for cash withdrawals, depending on the transaction slab, while balance inquiries are usually free.

- Agent Commissions: As an agent, you earn a commission on successful transactions, typically ranging from ₹2 to ₹15 per withdrawal.

- Platform Transaction Fees: If you operate a best white label Aeps portal, the Aeps india may charge you a flat fee (e.g., ₹0.25 to ₹10) or a percentage (0.5% to 1%) per transaction.

AEPS Commission Structure & Daily Income Opportunities

The Aadhaar Enabled Payment System (AePS) allows retailers to earn daily commissions by facilitating basic Aeps banking API services like cash withdrawals, balance inquiries, and mini-statements using just an Aadhaar number and biometrics. Active Aeps agents can generate ₹10,000–₹30,000+ monthly by capitalizing on tiered commission slabs and driving high transaction volumes.

Standard Commission Structure

Aeps Agent commission are typically tiered based on the transaction amount, with higher withdrawals yielding the best returns.

| Transaction Slab (₹) | Typical Retailer Commission |

|---|---|

| 100 – 999 | ~₹2.00 |

| 1,000 – 1,499 | ~₹3.00 |

| 1,500 – 1,999 | ~₹4.50 |

| 2,000 – 2,499 | ~₹5.50 |

| 2,500 – 2,999 | ₹5.00 – ₹7.00 |

| 3,000 – 10,000 | ₹13.00 – ₹15.00+ |

Additional Income Opportunities

- Balance Inquiry & Mini-Statements: Earn a small, fixed fee of ₹0.50 – ₹1.00 per successful inquiry. While the payout is low, this drives daily customer footfall.

- Aadhaar Pay: Accept merchant payments for high-value transactions (up to ₹50,000), offering commissions around 1%.

- Monthly Volume Bonuses: High volume Aeps agents who hit monthly transaction targets (e.g., 150–200+ transactions) can earn additional performance bonuses of ₹2,000 or more.

Realistic Daily Earnings Scenario

If a rural or semi-urban agent averages 50 transactions a day with an average commission of ₹15, the daily income is around ₹750.

- Withdrawals: 50 ×× ₹15 = ₹750/day

- Balance Inquiries: 20 ×× ₹0.50 = ₹10/day

- Total Daily Income: ₹760

- Total Monthly Income (26 days): ~₹19,760

Setup Requirements

To get started, you must register with a recognized best AePS service provider like Aeps india and meet the following basic requirements:

- Hardware: A smartphone/computer with a stable internet connection and an L1 Aeps certified biometric fingerprint scanner.

- Credentials: Valid Aadhaar, PAN card, and a bank account linked to your Aadhaar.

How Retailers Earn Money Using AePS Portal

Retailers earn money through AePS by acting as mini-bank branches. They generate income via commissions on cash withdrawals, balance inquiries, and mini-statements, and boost their primary store sales through increased customer footfall.

1. Cash Withdrawal Commissions

This is the primary source of income. When a customer withdraws cash using their Aadhaar and fingerprint, the retailer earns a tiered, slab-based commission from their Aeps india.

- Low-value transactions (₹100 to ₹1,000): Earns a flat ₹2 to ₹3.

- High-value transactions (₹3,000 to ₹10,000): Earns the highest Aeps commission, typically ranging from ₹10 to ₹15+ per transaction.

2. Balance Inquiries & Mini-Statements

Retailers charge small, consistent fees for providing instant, on-the-spot banking services.

- Balance Enquiry: Often yields a flat fee or commission of ₹0.50 to ₹3 per request.

- Mini-Statements: Yields around ₹1 to ₹5 every time a customer checks their recent account history.

3. Aadhaar Pay Services

For customers who have exceeded their daily AePS cash withdrawal limit, retailers can use best Aadhaar Pay to process cardless, biometric payments for good Aeps services. The retailer generally earns roughly a 1% commission on the transaction amount.

4. Cross-Selling & Increased Footfall

By acting as a localized “Aadhaar ATM”, retailers attract significantly more people to their shops. This increased footfall directly leads to higher cross-selling of the retailer’s primary products (e.g., groceries, mobile recharges, utility bills).

5. Monthly Bonuses

Aeps india offer monthly performance bonuses. Retailers who hit high transaction volume targets (such as processing over 150-200 successful transactions a month) can earn additional bonuses or cash rewards.

Security Features in AePS Online Banking Solutions

AePS secures online transactions through a multi-layered framework mandated by the NPCI. Its primary safety mechanism eliminates traditional passwords in favor of dual-factor biometric authentication (fingerprint or iris scan) mapped to your 12-digit Aadhaar number.

Key security features include:

- Biometric Liveness Detection: Advanced scanners use liveness checks to distinguish genuine, live fingerprints or iris scans from silicone molds or copied images, preventing artificial impersonation.

- End-to-End Encryption: Buying Micro ATM and get Aeps biometric devices capture and immediately encrypt scan data before transmission, ensuring sensitive biometric information cannot be intercepted by fraudsters.

- Cardless & PIN-less Processing: By relying exclusively on your Aadhaar identity and biometrics, the system removes the risks associated with lost physical debit cards or leaked PINs.

- Tokenization & Masking: During authentication, unique tokens are used rather than exposing raw Aadhaar numbers, and only masked bank details are visible.

- Real-Time SMS Alerts: Instant transaction alerts and mini-statements help users immediately detect and report unauthorized banking activity.

- Aadhaar Locking: Users can lock and temporarily disable their biometric data via the official highest volume Aeps portal to prevent unauthorized account access.

For comprehensive official guidelines on secure AePS banking, refer to the National Payments Corporation of India (NPCI) AePS Overview.

White Label AEPS Portal Development Guide

White Label AEPS Portal Development involves creating a ready-to-use, customize Aeps platform that allows businesses to offer Aadhaar Enabled Payment System services like cash withdrawals, balance inquiries, and fund transfers under their own brand, logo, and domain without building complex infrastructure from scratch.

Key Features of a White Label AEPS Portal

- Brand Customization: Your own domain, company name, color schemes, and logos across web and mobile interfaces.

- Admin Control Panel: Manage and monitor an unlimited network of Master Distributors, Distributors, and Retailers.

- Multi-Layer Security: Biometric and OTP-based Aadhaar authentication ensuring secure transactions.

- Real-Time Settlement: Instant processing and settlement of funds and commission payouts.

- Extensibility: Often bundled with other High speed Aeps API like BBPS (Bharat Bill Payment System API), and mobile recharge api.

Benefits of the White Label Model

- Quick Launch: Pre-tested, ready-to-deploy Aeps b2b platform can get your business live in just 1 to 2 working days.

- Low Investment: Significantly more cost-effective than building custom Aeps API integration and complying with NPCI frameworks in-house.

- Revenue Generation: Earn steady income through retailer commission slabs and service convenience fees.

How to Select Best AePS Portal Service Provider Company

Aeps india is the best AePS portal provider, you must prioritize liquidity, security, and profitability to ensure smooth operations for your customers.

Prioritize these key factors to ensure a profitable, secure, and seamless banking experience:

1. Security and Regulatory Compliance

- NPCI Authorization: Ensure the Aeps india is authorized by the National Payments Corporation of India and fully compliant with RBI and UIDAI guidelines.

- Biometric Security: The reliable Aeps portal should support L1-certified biometric RD devices (fingerprint/iris) and include 2FA (Two-Factor Authentication) to prevent fraud.

2. Transaction Success Rate & Uptime

- Choose a Aeps india with a high transaction success rate (ideally

≥98

%) and over

99.9

% server uptime. High reliability is crucial for building trust, especially in rural or semi-urban areas with frequent footfall.

3. Settlement Speed and Cash Flow

- Instant Settlements: Look for Aeps india offering instant (

𝑇

+0) or same-day (

𝑇

+1) settlement of funds to your bank account. This ensures your working capital remains liquid so you don’t run out of cash to dispense.

4. Commission Structure and Transparency

- Check for competitive and transparent Aeps commission structures. You should aim to earn between ₹5 to ₹15+ per transaction, with higher payouts typically on withdrawals exceeding ₹3,000. Ensure there are no hidden deduction fees.

5. Customer and Technical Support

- AEPS can involve biometric/server glitches. Dedicated 24/7 technical support via phone, email, or WhatsApp is essential to immediately resolve failed transactions or connectivity issues.

6. Additional Services (Value Add)

- Choose a Aeps service platform that serves as a one-stop-shop by offering additional integrated Aeps services like Micro ATM software, BBPS software and fast mobile recharge api to maximize your daily income streams.

7. User-Friendly Interface

- The web portal or mobile Aeps app should be intuitive and require minimal technical expertise to operate. Quick and easy KYC for Aeps onboarding is also a major advantage.

Why Choose Aeps India for AePS Portal Solutions

Aeps india is an professional AEPS portal provider ensures secure, seamless, and compliant banking services. It allows businesses to offer essential financial services like cash withdrawals, balance inquiries, and mini-statements. Key advantages of partnering with a Aeps india include:

- Bank-Grade Security & Compliance: Aeps india are fully authorized by the NPCI, RBI, and UIDAI. They utilize highly encrypted biometric (fingerprint/iris) authentication to prevent fraud and protect sensitive customer data.

- High Success Rates & Uptime: By utilizing stable backend infrastructure, they guarantee 99.9% uptime. This minimizes transaction failures and builds trust with rural or unbanked customers.

- Maximum Earnings: Trusted Aeps platform offer highly competitive Aeps commission structures, allowing retail agents, kirana stores, and CSCs to earn up to ₹15 to ₹16 per successful transaction.

- Instant Settlements (T+0): Aeps india offer same-day or instant settlement of funds, ensuring your working capital is never blocked and your cash flow remains fluid.

- Comprehensive Service Bundling: Aeps india scales with your business, allowing you to seamlessly integrate services like Micro ATM software solution, BBPS API service (Bill Payments) on a single Aeps platform.

- 24/7 Technical Support: Round-the-clock support guarantees quick troubleshooting and dispute resolution, protecting you from financial losses during network downtime.

Future Trends AEPS Portal Company

AEPS portal company such Aeps india are rapidly evolving from basic cash-withdrawal tools into comprehensive, AI-driven rural financial hubs. Major industry trends for 2026 center around hyper-secure biometric authentication, expanded micro-banking services for local retailers, and real-time fund settlements.

1. Advanced Security & Regulatory Compliance

To counter cybersecurity threats, the Reserve Bank of India (RBI) and NPCI are implementing stricter regulations.

- L1 Certified Devices: All biometric devices must be STQC-certified, Level 1 (L1) compliant to encrypt data at the hardware level.

- AI & Liveness Detection: Artificial Intelligence is utilized for real-time risk scoring and to prevent spoofing through fingerprint or photo cloning.

- One Operator, One Bank: Agents are increasingly restricted to linking their credentials with only one acquiring bank to improve transaction accountability.

2. Evolution into “Phygital” Financial Hubs

Local “Kirana” stores and merchants are upgrading from basic cash-out systems to full-fledged micro-banking touchpoints.

- Expanded Services: Retail agents can now offer embedded finance, including micro-loans, insurance, digital gold, and UPI-ATM services directly to unbanked populations.

- Multi-Modal Biometrics: Portals are transitioning to accept face and iris scans. This provides an alternative for rural customers whose fingerprints have worn down.

- Voice Payments: Customers can authorize transactions or check balances via voice commands in their regional languages.

3. Retailer-Friendly Operations and Profitability

- Higher Commissions: Tiered structures allow merchants to earn attractive commissions (up to ₹15 to ₹20 per high-value transaction).

- Instant Settlement: Same-day (

𝑇

+0) and immediate (

𝑇

+1) settlement features are becoming standard, providing agents with higher daily liquidity.

4. Technological Backbone

- Mobile-First Platforms: High performance Android Aeps apps and cloud-based frameworks are replacing traditional desktop interfaces, allowing agents to operate seamlessly from a smartphone.

- Blockchain Adoption: Aeps india are exploring blockchain technology to create immutable and highly secure transaction ledgers.

Conclusion

Choosing the best AEPS portal company for online banking solutions is one of the most important decisions for retailers, distributors, CSP agents, and fintech businesses looking to grow in the digital payment industry. A secure AEPS portal solution helps businesses provide essential banking services like cash withdrawal, balance enquiry, mini statement, and Aadhaar Pay quickly and safely through Aadhaar-based authentication.

Today, the demand for AEPS portal services in India is increasing rapidly because customers want fast and convenient banking access without visiting bank branches. This has created a strong opportunity for businesses to build profitable digital banking services with the help of reliable AEPS software and top Aeps API integration.

A professional AEPS portal company such Aeps india offers secure transaction systems, high Aeps API uptime, fast processing, user-friendly dashboards, and advanced reporting features that help retailers and businesses manage operations smoothly. With the right AEPS solution, businesses can generate daily commission income and expand their reach in both urban and rural areas.

The biggest advantage of using a trusted AePS online banking solution is low investment with high earning potential. Retailers and business owners can easily manage transactions, provide better customer service, and grow their digital payment business smoothly.

The popularity of AEPS business solutions, white label AEPS portal, and AEPS API services is also growing because they support financial inclusion in India by making banking services accessible to everyone. As digital banking adoption continues to rise, investing in a fast AEPS platform can help businesses achieve long-term growth in the fintech sector.

By choosing a reliable Aeps b2b platform like AEPS India, businesses get secure Aeps API integration, high transaction success rate, advanced Aeps dashboard features, and strong technical support. This helps retailers build customer trust and expand their business faster in the competitive fintech market.

Aeps India provides a secure and advanced AePS portal solution in India designed for retailers, agents, and fintech companies. With features like fast transaction processing, secure Aadhaar authentication, easy integration, and dedicated technical support, businesses can efficiently manage online banking services and grow faster in the fintech industry.

If you are planning to start or expand your AEPS online banking business, now is the best time to choose a trusted and scalable AEPS portal company. With the right technology and business strategy, you can build a successful and profitable digital banking platform for the future.

Looking for the best AEPS portal company in India for secure online banking solutions? Contact Aeps India today for advanced AEPS portal development, AEPS API integration, white label AEPS software, and digital banking solutions to grow your fintech business successfully

FAQ – Best AePS Portal Company for Online Banking Solutions

An AePS portal (Aadhaar Enabled Payment System portal) is an online banking platform that allows retailers and businesses to provide banking services like cash withdrawal, balance enquiry, mini statement, and Aadhaar-based transactions using biometric authentication.

An AePS portal works through Aadhaar number verification and fingerprint authentication. Once the customer is verified, the banking transaction is processed securely in real time.

Anyone can start, including:

Retail shop owners

Agents & distributors

Small businesses

Fintech startups

A trusted AePS portal provider in India offers:

Cash withdrawal

Balance enquiry

Mini statement

Aadhaar-enabled banking services

You generally need:

Aadhaar card

PAN card

Bank account

Mobile number

Biometric device

AePS online banking solutions help provide easy and secure banking access in rural and urban areas without requiring debit cards or bank visits.

The best AePS portal company should provide:

Secure biometric authentication

High transaction success rate

Instant settlement

Real-time reporting

Easy dashboard management

Fast Aeps API integration

Main benefits include:

Low investment business

High earning potential

Fast banking transactions

Secure biometric authentication

Better customer service

You need:

Smartphone or computer

Internet connection

Biometric fingerprint device

Yes, a trusted AePS portal solution uses secure biometric verification and encrypted banking systems to ensure safe and reliable transactions.

AePS business requires low investment, making it a profitable opportunity for retailers and startups.

Yes, you can operate AePS business from home or shop using internet and biometric setup.

AEPS helps people access banking services easily, especially in rural and semi-urban areas where ATM and bank access may be limited.

Aeps india is a trusted AEPS portal provider offering secure transactions, fast processing, multi-bank support, and easy-to-manage banking solutions.

It helps businesses attract more customers by offering digital banking services and increasing commission-based income.

Yes, top AEPS API integration allows businesses to add banking services to best mobile Aeps apps and websites easily.

AePS portals make banking services easy, secure, and accessible for customers without visiting bank branches.

Retailers earn commission on every successful transaction processed through the AePS portal.

You can start AePS business by registering with a Aeps india, completing Aeps KYC verification, and setting up biometric devices and Aeps portal access.

The future is very strong because digital banking and Aadhaar-based services are growing rapidly across India.

Yes, AePS business is highly profitable due to increasing demand for digital payment and online banking services.

A white label AEPS portal allows businesses to launch their own branded online Aeps banking platform without building Aeps software from scratch. It is ideal for fintech startups and digital payment companies.

Before selecting an AEPS portal company, check:

Security and encryption system

Transaction success rate

Aeps API performance and uptime

Technical support quality

User-friendly admin dashboard

Commission structure

AEPS India provides:

Secure API integration

High transaction success rate

Fast processing system

User-friendly dashboard

Reliable customer support

Yes, the AePS business in India is profitable because retailers earn commission on every successful banking transaction and can increase daily customer traffic.

Trusted AEPS Provider in 2026: Features, Benefits & Business Opportunities

Best AEPS API for High Profit in India 2026