AEPS Business with Biometric & Face Authentication: Earn More Commission

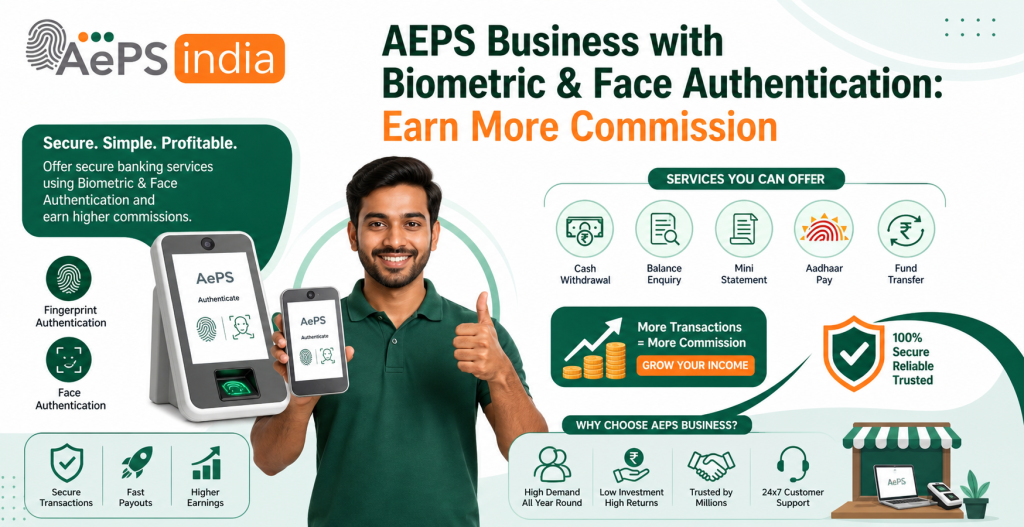

Are you looking to start a profitable AEPS business in India with advanced security features like biometric authentication and face authentication? If yes, this is the right time to enter the fast-growing digital banking market. The Aadhaar Enabled Payment System (AEPS) allows retailers and agents to provide essential banking services such as cash withdrawal, balance enquiry, mini statement, and Aadhaar to Aadhaar fund transfer using Aadhaar verification.

AEPS business is a bank-led model that allows financial transactions at micro-ATMs or via smartphones using Aadhaar authentication. It enables retailers and Business Correspondents (BCs) to turn their shops into mini-banking hubs, offering essential services cash withdrawal, balance inquiry, and mini-statements without the need for debit/credit cards or PINs. As of 2026, this system is heavily upgraded with mandatory Aeps biometric (fingerprint/iris) and advanced face authentication to enhance security and prevent fraud.

With the introduction of biometric AEPS authentication and face authentication AEPS service, transactions have become more secure, faster, and more reliable. This increases customer trust and helps agents perform more successful transactions every day. A higher transaction success rate directly means more commission income for retailers and distributors.

If you are searching for the best AEPS service provider, biometric AEPS API integration, or a reliable AEPS platform with face authentication, choosing the right partner is very important. A strong AEPS software solution offers real-time processing, high uptime, instant settlement, secure Aeps API integration, and full compliance with digital payment guidelines. These features help you build customer trust and grow AEPS business faster.

By choosing a reliable Aeps platform like AEPS India, you can start AEPS business with low investment and high earning potential. Biometric and face authentication not only improve security but also reduce fraud risks, making your digital banking service more dependable.

With the support of Aeps india, you can build a scalable and secure AEPS business platform that supports biometric authentication and advanced face verification technology. Our goal is to help retailers and fintech startups create a profitable digital banking business with high transaction success rate and transparent Aeps commission structure.

Starting AEPS business with biometric & face authentication in 2026 is not just a trend it is a smart business move. With secure Aeps technology, high Aeps commission margins, and growing demand in rural and urban areas, this opportunity can help you build long-term income and a strong digital payment business.

With this guide, you will learn how to choose a reliable AEPS service provider, implement biometric and face authentication, and grow your AEPS business successfully in 2026 and beyond with NobleWebStudio.

What is AEPS?

Aadhaar Enabled Payment System (AEPS) is a National Payments Corporation of India (NPCI) developed, bank-led model that allows secure, cardless, and PIN-less transactions using Aadhaar authentication. Users can perform basic banking services like cash withdrawals, deposits, balance inquiries, and mini-statements at micro-ATMs or via banking correspondents using their fingerprints or iris scans.

How Biometric Authentication Works in AEPS

Biometric authentication in the Aadhaar Enabled Payment System (AEPS) replaces PINs and cards by using a user’s unique Aeps fingerprint or Aeps iris scan, matched against the Aadhaar database. A customer enters their Aadhaar number, scans their finger on a UIDAI-certified Aeps device, and the system verifies identity in real-time for secure, cardless transactions.

Key Aspects of AEPS Biometric Authentication:

- Process Flow: The user provides their 12-digit Aadhaar number, selects the bank, and scans their finger/iris. This data is encrypted and sent to UIDAI to match against stored biometric records.

- Security & Safety: Because fingerprints are unique, this method significantly reduces fraud risks compared to passwords. It ensures only the rightful owner can access funds.

- Liveness Detection: Modern AEPS system use “liveness detection” to ensure the scan is from a live person, preventing the use of fake or cloned biometric impressions.

- Types of Services: It is used for cash withdrawal, balance inquiry, and funds transfer at micro ATM or business correspondent points.

- Two-Factor Authentication: For enhanced security, some transactions may require a second authentication layer, such as an OTP (One-Time Password), in addition to the Aeps biometric scan.

Core AEPS Services

Core AePS services enable secure, cardless banking through biometric authentication (fingerprint/iris) at local, authorized outlets. Key services include instant cash withdrawal, balance enquiry, mini statements, Aadhaar-to-Aadhaar fund transfers, and cash deposits. These services, regulated by NPCI, are available 24/7, providing financial inclusion in remote areas.

Key Core AEPS Services

- Cash Withdrawal: Allows users to withdraw cash from their linked bank account via Aeps biometrics.

- Balance Enquiry & Mini Statement: Provides real-time account balances and transaction histories.

- Fund Transfers: Facilitates secure, direct transfers between Aadhaar-linked accounts.

- Cash Deposit: Enables deposits into bank accounts at authorized, participating locations.

- Aadhaar Pay: Facilitates merchant payments through biometric authentication.

- Best Finger Detection (BFD): Optimizes authentication success by identifying the best fingerprint.

Read Blog : AEPS Registration Online: Complete Guide for 2026

Key Aspects of AEPS Business with Biometric & Face Authentication

AEPS business, enhanced with Aeps biometric fingerprint/iris and face authentication, provides secure, cardless, and interoperable banking cash withdrawals, deposits, and balance inquiries via Aadhaar-linked accounts. It drives financial inclusion in rural areas, offering 24/7 real-time, high-success-rate transactions.

Key Aspects of AEPS Business with Advanced Authentication:

- Advanced Security (Biometric & Face Auth): Reduces fraud by using unique biometric data (fingerprint, iris, or face) instead of PINs or signatures, complying with NPCI/UIDAI standards. Face authentication offers increased inclusivity for those with worn fingerprints.

- Core Banking Services: Provides essential banking services at local, trusted merchant outlets (Bank Mitras), including Aeps Cash Withdrawal, Balance Enquiry, Mini Statement, and Cash Deposit.

- Interoperability: Enables customers to access accounts from any bank, regardless of the bank where they hold their account, enhancing convenience for rural, unbanked, or underbanked populations.

- Aadhaar Pay (Merchant Payments): Facilitates instant, cashless payments for goods/services using biometric or face authentication, reducing dependence on physical currency.

- Real-Time Settlement & High Reliability: Provides instant transaction authorization and fast Aeps commission settlement (T+0 or same-day) for agents, maintaining high (98-99%) success rates for business operations.

- Easy Technical Integration & Low Cost: Requires minimal infrastructure (smartphone + STQC-certified biometric device), allowing for easy integration into existing web portals or Android Aeps apps.

- Financial Inclusion Impact: Bridges the banking gap in remote areas by enabling access to government benefits (e.g., MGNREGA, pensions) without needing debit cards.

- Best Finger Detection (BFD): A service that identifies the best, most reliable fingerprint for successful, faster authentication.

For successful operations, using certified, secure, and reliable technology is crucial to protecting both business and customer data.

Top Use Cases of AEPS Business with Biometric & Face Authentication

AEPS Aadhaar Enabled Payment System business, enhanced with biometric (fingerprint/iris) and face authentication, revolutionizes rural banking by enabling secure, cardless, and PIN-less transactions through local retail agents. Top use cases include cash withdrawals/deposits, Aadhaar Pay for merchant payments, Direct Benefit Transfers (DBT), balance inquiries, and mini-statements.

Top Use Cases of AEPS Business with Biometric & Face Auth:

- Cash Withdrawal & Deposit (Micro-ATMs): Transforms local shops into mini-banks, allowing users to withdraw or deposit cash using Aadhaar and biometric/face authentication.

- Aadhaar Pay (Merchant Payments): Enables merchants to accept digital payments directly from customers’ bank accounts, eliminating the need for card machines or PINs.

- Direct Benefit Transfer (DBT) Disbursement: Facilitates immediate, secure access to government subsidies, pensions, and welfare payments for rural beneficiaries.

- Balance Inquiry & Mini Statements: Provides instant, secure, and real-time access to account balances and recent transaction history.

- Aadhaar-to-Aadhaar Fund Transfer: Allows secure money transfers between Aadhaar-linked accounts without needing bank details.

- eKYC Services: Supports instant, paperless, and digital verification for opening bank accounts, telecom services, and other financial services.

- Utility Bill Payments & Recharges: Facilitates payment for electricity, water, DTH, and mobile recharges directly through agent networks.

- Face Authentication for Enhanced Accessibility: Provides a superior alternative to fingerprints, particularly useful for elderly users or in areas where, due to physical labor, fingerprints are worn out.

These services drive financial inclusion, particularly in remote areas, by turning local retail shops into crucial, secure, and accessible banking points.

Face Authentication in AEPS – The Future of Digital Banking

Face Authentication in the Aadhaar Enabled Payment System (AEPS) is rapidly emerging as a cornerstone of digital banking in India, transforming how beneficiaries in rural and semi-urban areas access financial services. By replacing or supplementing traditional fingerprint scans with facial recognition, this technology addresses critical issues like failed authentication due to worn-out fingerprints, offering a more secure, hygienic, and inclusive banking experience.

Key Aspects and Advantages of Face Authentication in AEPS

- Enhanced Security: Face authentication uses 1:1 matching against the Aadhaar database, featuring advanced “liveness detection” to ensure a real person is present, preventing fraud through photos or masks.

- Improved Accessibility & Inclusion: It provides a crucial alternative for elderly individuals or laborers whose fingerprints have faded due to manual work, ensuring they are not excluded from banking services.

- Contactless Convenience: As a touchless method, it improves hygiene and eliminates the need for specialized, often high-maintenance, fingerprint scanners.

- High Adoption & Speed: The technology enables near-instantaneous verification, significantly faster than fingerprinting in low-network areas, and is increasingly favored for high-value transactions.

The Future of Digital Banking

- Growth Trajectory: Aadhaar-based face authentication transactions hit a high of 10.6 million in May 2023, with usage projected to continue growing rapidly.

- Multi-Modal Integration: The future lies in combining face authentication with other biometric methods (fingerprints, iris) and OTPs to create a “two-step” verification process that further slashes fraud risks.

- Expanding Use Cases: Beyond cash withdrawals and balance inquiries, it is being used for:

- Direct Benefit Transfers (DBT): Securing subsidies and pensions.

- Digital Life Certificates: Aiding pensioners.

- Digital Account Opening: Allowing remote Aeps onboarding.

- NPCI & RBI Mandates: With the Reserve Bank of India (RBI) mandating two-factor authentication for digital payments by 2026, face authentication is poised to become a standard, secure, and user-friendly feature in India’s digital ecosystem.

Operational Benefits for Agents

Agents and Business Correspondents (BCs) using platforms like Aeps india can utilize standard mobile cameras to offer these services, reducing equipment costs while enhancing trust and enabling higher transaction volumes. As of late 2025, it is becoming a standard feature for secure and compliant banking.

Read Blog : Aadhaar Enabled Payment System API Explained: Complete Guide

Why You Should Start AEPS Business with Biometric Face Authentication

Starting Aadhaar Enabled Payment System business with Biometric Face Authentication (specifically leveraging Aadhaar Face RD service) in 2026 is a strategic move to boost revenue, enhance security, and improve customer experience. As of January 1, 2026, NPCI-mandated security upgrades make this advanced, non-contact method a superior choice over traditional, sometimes unreliable fingerprint scanners.

Here is why you should start an AEPS business with Face Authentication:

1. Superior Customer Accessibility (Inclusivity)

- Overcomes Worn Fingerprints: In rural areas, laborers, farmers, and the elderly often have faded or damaged fingerprints, leading to high failure rates with traditional Aeps biometric scanners. Face authentication solves this, allowing them to transact successfully.

- Higher Customer Adoption: Customers who have been rejected by fingerprint scanners previously will prefer your service, increasing your footfall.

- Solves Physical Challenges: It is easier for the elderly and those whose fingerprints might be difficult to read due to physical conditions.

2. Enhanced Security and Fraud Prevention

- Advanced Liveness Detection: Unlike static photos, the AI-based face recognition technology ensures the customer is physically present, drastically reducing fraud risks like spoofing with silicone molds or photos.

- Two-Factor Authentication (2FA) Readiness: With increasing fraud, facial recognition adds an extra, highly secure layer that builds trust, which is crucial for retaining customers.

- Mandatory Security Layer: As of early 2026, NPCI is integrating face authentication as an additional verification method to strengthen protection.

- Reduced Identity Theft: The best Aeps system captures a live face and matches it directly against Aadhaar records,” ensuring that only the rightful account holder can access their money”.

3. Unmatched Convenience & Hygiene

- Contactless Experience: As a hygienic touchless method, it eliminates the need for physical contact with shared devices, making it preferred by many customers.

- Speed: Face authentication is fast and efficient, allowing for quicker transactions, reducing waiting times in busy retail outlets.

4. Higher Earning Potential for Agents

- Higher Earnings: Retailers can, “earn more” by offering, “secure banking services,” with Aeps india offering up to ₹15 per transaction for, “Super Prime Retailers”.

- Increased Transaction Volume: Because face authentication is more reliable (lower failure rates), you can process more transactions per day, earning higher Aeps commissions (up to ₹15+ per transaction).

- One-Stop Shop: By pairing face authentication with other services like Direct Benefit Transfer (DBT) withdrawals and Aadhaar Pay, you turn your shop into a comprehensive banking hub.

- Reduced Hardware Costs: Face authentication can work on standard mobile Aeps devices equipped with a decent camera, potentially reducing the need for expensive, specialized hardware.

5. Future-Ready and Compliant Business

- Lower Failure Rates: Face authentication is increasingly critical providing a smoother and more reliable banking experience than traditional, methods.

- High-Value Transactions: Face authentication is often used as a primary authentication factor for high-risk transactions allowing for more secure high-value, withdrawals.

- Compliant with 2026 Standards: The industry is moving towards L1-certified Aeps devices and multi-modal biometrics. Adopting face authentication now makes your business compliant with future-ready NPCI and UIDAI guidelines.

Summary Table: Face vs. Fingerprint

| Feature | Face Authentication | Fingerprint Scan |

|---|---|---|

| Accessibility | High (Works for all) | Limited (Worn prints fail) |

| Hygiene | Contactless | Physical Contact |

| Security | High (Liveness check) | Medium (Spoofing risk) |

| Speed | Instant | 2-3 seconds |

For retailers, starting AEPS business with face authentication is not just a technological upgrade it is a, game-changer for increasing, daily, high-frequency, customer-facing, revenue-generating, reliable, secure, and future-proof income.

Key Technical & Safety Requirements for 2026

- STQC-Certified Devices: While face authentication” allows using a camera you should still ensure any accompanying devices are STQC-certified.

- “One Operator, One Bank” Rule: Agents must now adhere to strict regulations where they can link only one acquiring bank for AEPS transactions.

- Mandatory Re-KYC: Agents with 3 months of inactivity must complete a new Aeps KYC.

By embracing this game-changer technology you can build long-term stability and trust in your community while building a profitable Aeps business.

High Commission AEPS Platform for Retailers and Agents

The top high commission AEPS platforms for retailers and agents in 2026, such as Aeps India and Noble Web Studio, offer up to ₹15–₹20 per transaction for high-value withdrawals, instant (T+0) settlements, and >98% success rates. These Aeps platforms are designed to turn local kirana shops into “mini-banks,” providing essential, secure, cardless banking services to rural and urban customers.

Key Features & Top Providers (2026)

- High Earnings & Support: Aeps india offer up to ₹13–₹16+ per transaction for high-value Aeps withdrawals, featuring instant 24/7 (T+0) settlements and >98% success rates.

- High Earnings & Instant Settlement: Incentive-based models allow for significant earnings, particularly on withdrawals over ₹3,000, with funds instantly transferred to agent bank accounts.

- Services & Setup: Agents facilitate cash withdrawal service, Aadhaar Pay (up to ₹50,000), mini-statements, and DMT using smartphones with Aeps L1-certified biometric.

- Comprehensive Digital Services: Aeps b2b Platforms include mini-statements, Aadhaar Pay, and bill payments.

- Top Players: Leading Aeps platforms in 2026 for high Aeps commission structures include Aeps India and Noble Web Studio.

- High Success Rates & Flexibility: Reliable, NPCI-compliant services maintain high transaction success rates and offer white label Aeps solutions for branding.

Top High-Commission AEPS Platforms (2026)

- AEPS India: Recognized as a Aeps india offering up to ₹13 + ₹2 bonus (total ₹15) per transaction for retailers.

- Noble Web Studio: Known for industry-leading Aeps commissions of ₹12-₹15 per transaction, specifically for “Super Prime” retailers.

2026 Regulatory & Market Trends:

- Stricter Security & Technology: Mandatory Aeps L1 devices and the “One Operator, One Bank” rule are in effect to combat fraud, with AI-driven surveillance becoming common.

- Increased Transaction Limits: Aadhaar Pay supports transactions up to ₹50,000 per day.

Commission Structure for Retailers/Agents (2026)

Payouts generally peak at ₹13–₹15+ per transaction for amounts between ₹3,000 and ₹10,000, with lower, tiered amounts for smaller withdrawals. Aadhaar Pay enables a 1% commission on high-value transactions up to ₹50,000.

Why AEPS Business is Growing in 2026

The best AEPS business is growing rapidly due to its critical role in driving financial inclusion in rural India, enabling secure, cardless, and PIN-less transactions via biometric authentication. Key drivers include 99.9% uptime, high transaction success rates, real-time settlements, and lucrative commissions for agents.

Key Reasons for the Growth of AEPS Business:

- Financial Inclusion & Rural Reach: AEPS brings banking services to remote areas where bank branches are scarce, allowing residents to withdraw money, check balances, or transfer funds without traveling far.

- Ease of Use & Security: Transactions require only an Aadhaar number and fingerprint/iris scan, making them accessible to those with low digital literacy. The top Aeps system is highly secure, reducing fraud risk.

- High Agent Earnings & Retailer Adoption: Small shopkeepers (kirana stores) act as Business Correspondents (BCs), earning commissions (₹2–₹15+ per transaction) while increasing footfall in their shops.

- Government Support (DBT): The Fast Aeps system is heavily used for withdrawing government subsidies and pensions, boosting trust and usage volume.

- Interoperability & Reliability: Customers from any bank can use any AEPS-enabled agent. The high success rate (98%+) and 99.9% uptime ensure dependable services.

- Comprehensive Services: Beyond cash withdrawals, agents can offer mini-statements, bill payments (BBPS), and remittances, turning local shops into one-stop financial hubs.

- Real-Time Settlement: Agents enjoy fast, same-day settlement of funds (T+0/T+1), which is crucial for managing working capital.

Driven by over 2.8 billion transactions in 2024, the network of 1.4 million Business Correspondents (BCs) continues to expand, acting as a crucial pillar for digital India.

Read Blog : Cost-Effective AEPS API Solutions for High-Volume Transactions

AEPS Services You Can Offer as a Retailer or Agent

As a retailer or agent, you can offer essential AePS services, acting as a mini-bank to facilitate secure, biometric-based transactions. Key services include cash withdrawals, balance inquiries, mini-statements, and cash deposits, enabling customers to manage funds without a debit card or PIN, while earning commission on each transaction.

Key AEPS Services to Offer:

- Cash Withdrawal: Customers can withdraw cash from their Aadhaar-linked bank accounts using their fingerprint or iris scan.

- Balance Inquiry: Instant, real-time checking of the current balance in the customer’s bank account.

- Mini Statement: Provides a snapshot of the last 5–10 transactions for quick account tracking.

- Cash Deposit: Facilitates cash deposits into Aadhaar-linked bank accounts, particularly useful for rural areas.

- Aadhaar to Aadhaar Fund Transfer: Enables secure, direct money transfers between two Aadhaar-linked accounts.

- Aadhaar Pay: Allows merchants to accept digital payments directly from a customer’s bank account, often with higher transaction limits.

Benefits for Retailers/Agents:

- Commission Earnings: Agents typically earn ₹2 to ₹15+ per cash withdrawal, with higher commissions for larger amounts.

- Increased Footfall: Offering banking services attracts more customers to your retail shop.

- Instant Settlement: Fast Aeps platform offer T+0 (same day) or real-time settlement of funds, ensuring continuous working capital.

- Low Setup Cost: Requires only a smartphone/tablet, a STQC-certified Aeps biometric device, and an internet connection.

Requirements:

You must register with an Aeps india india best AEPS service provider and complete Aeps KYC to start providing Aeps services securely.

AEPS Cash Withdrawal Process

AEPS cash withdrawal allows you to withdraw money from your linked bank account via a business correspondent or micro-ATM using only your Aadhaar number and biometric authentication (Aeps fingerprint device/Aeps iris device). The process involves finding an agent, entering bank details, scanning your finger, and receiving cash, usually with a daily limit of ₹10,000.

Steps for AEPS Cash Withdrawal Process:

- Locate an AEPS Center: Visit a local kirana shop, bank Mitra, or banking correspondent equipped with a micro-ATM/POS machine.

- Provide Details: Inform the agent of your intent to withdraw, then provide your 12-digit Aadhaar number and select your bank name.

- Specify Amount: Inform the agent of the exact amount you wish to withdraw.

- Biometric Authentication: Place your finger on the Aeps biometric scanner for fingerprint authentication, which connects to the UIDAI database.

- Transaction Completion: Once the Aeps scanner verifies your identity, the agent will process the transaction.

- Collect Cash and Receipt: The agent will provide the cash and a physical or digital receipt of the transaction.

Key Requirements & Limits:

- Mandatory Linking: Your Aadhaar number must be linked to your bank account.

- No Card/PIN Needed: This service requires no debit card or PIN.

- Transaction Limit: The daily withdrawal limit is typically up to ₹10,000.

AEPS Transaction Limits

The AePS designed for basic banking, featuring specific transaction limits to balance security and convenience, typically allowing for cash withdrawals of up to ₹10,000 per transaction and ₹50,000 per month (based on a rolling 30-day period). These limits can vary based on the issuing bank’s policies, which often set daily cumulative limits around ₹10,000–₹25,000.

Key AEPS Transaction Limit

- Per Transaction Limit: Generally capped at ₹10,000 for cash withdrawals.

- Daily Cumulative Limit: Most banks limit total daily withdrawals via AePS to around ₹10,000 to ₹50,000.

- Monthly Limit: NPCI recommends a maximum cumulative limit of ₹50,000 over a rolling 30-day period.

- Transaction Frequency: Some banks may limit customers to a maximum of 5 transactions per month.

- Balance Inquiry/Mini Statement: These Aeps b2b services usually have no monetary limits, though a maximum of 5–10 requests per day may be permitted.

- Aadhaar Pay Limits: Specifically for merchants, this service often allows higher daily limits, up to ₹50,000, and is distinct from regular cash withdrawals.

Important Notes for Users

- Bank-Specific Variation: While NPCI sets guidelines, individual banks (e.g., SBI, BOB, PNB) can set lower, more restrictive limits based on risk management.

- No PIN Required: Transactions are authenticated only by biometrics (fingerprint/iris).

- Daily Reset: Daily limits generally reset at midnight, or in some cases, follow a 24-hour cycle.

- Failed Transactions: If a transaction fails, money is typically not debited or is automatically reversed.

Read Blog : AEPS Onboarding: Complete Step-by-Step Guide for New Businesses

Biometric & Face Authentication in AEPS

Biometric and Face Authentication in the AEPS are enhancing security and accessibility for digital banking in India, particularly in rural areas. As of 2026, AEPS has evolved to include AI-powered face recognition alongside traditional fingerprint scanning to reduce fraudulent transactions.

Key Components of AEPS Authentication

- Biometric Authentication (Mandatory): Aeps Fingerprint scanning is standard for identifying the account holder, ensuring the person is present, and preventing unauthorized access.

- Face Authentication (Enhanced Security): A newer, contactless method that matches a live facial image against Aadhaar database records, providing an alternative for users with worn-out fingerprints (e.g., laborers, elderly).

- Liveness Detection: Both methods now require AI-based liveness detection to ensure the user is physically present and not using photos, videos, or silicone molds to spoof the system.

Benefits of Biometric & Face Integration

- Improved Success Rates: Face authentication provides a higher success rate for users whose fingerprints have faded.

- Hygiene and Contactless: Face scanning removes the need to touch shared devices.

- Fraud Reduction: NPCI reports that face authentication significantly lowers the risk of identity theft.

- Accessibility: Allows customers to conduct banking without a debit card or PIN, using only their Aadhaar number and unique physical traits.

2026 Regulatory Updates & Process Flow

- Enhanced Security Standards: From January 1, 2026, all Aeps biometric devices must be STQC-certified Level 1 (L1) to boost security.

- Fraud Prevention: New rules restrict agents to a single bank connection and require re-KYC for agents inactive for 3 months.

- Process Steps: Transactions involve entering the Aadhaar number, biometric/Aeps face authentication, and secure validation via NPCI/UIDAI.

These updates enhance best AEPS as a secure, inclusive, and efficient method for doorstep banking, allowing retailers to act as mini-ATMs.

Benefits Biometric & Face Authentication in AEPS

Biometric and face authentication in AEPS enhance security and financial inclusion by allowing instant, cardless, and PIN-less transactions using Aadhaar, ensuring only the account holder accesses funds. These technologies reduce fraud, facilitate secure 24/7 banking for rural/elderly populations, and enable seamless, contactless, and hygienic authentication.

Key benefits of Biometric & Face Authentication in AEPS include:

- Enhanced Security & Fraud Prevention: Transactions are authorized using unique fingerprints or iris scans, significantly reducing unauthorized access and fraud compared to traditional PINs or passwords. Advanced liveness detection ensures the account holder is physically present.

- Superior Accessibility (Cardless & PIN-less): Users do not need to remember PINs or carry debit cards, making banking accessible to technologically challenged users or those in rural areas.

- Financial Inclusion: Extends banking services to unbanked, remote, and rural populations, bridging the gap between banks and customers.

- Convenience & Speed: Facilitates real-time, 24/7 transaction processing, including cash withdrawals, deposits, and balance inquiries.

- Improved Hygiene with Face Authentication: Aeps india offers a contactless, hygienic alternative to fingerprint scanning, removing dependencies on fingerprint quality.

- Direct Benefit Transfer (DBT): Enables secure, direct receipt of government subsidies and pensions into bank accounts.

- Interoperability: Allows users to access accounts across different banks via AEPS.

- Business Growth for Agents: Retailers can act as mini-ATMs, increasing customer footfall and earning Aeps commission on transactions.

Key Benefits:

- Earn up to ₹15 commission per transaction for Super Prime Retailers

- Safe and secure Aeps biometric + Aeps face authentication system

- Quick and smooth transaction processing

- Attractive and competitive payout structure

- Dedicated support team for retailers

By working with Aeps india, retailers can grow their daily income, bring more customers to their shop, and build strong trust in their local community.

Features Biometric & Face Authentication in AEPS

AEPS utilizes biometric (fingerprint/iris) and face authentication to provide secure, cardless, and PIN-less banking services like cash withdrawals, deposits, and balance inquiries. These methods offer high security, real-time verification, and improved accessibility, particularly for individuals with worn-out fingerprints or in remote areas.

Key Features of Biometric Authentication (Fingerprint/Iris)

- High Security & Accuracy: Uses unique, non-replicable biological traits for authentication, reducing fraud risk.

- Interoperability: Enables transactions across any bank, regardless of the user’s home bank, via Business Correspondents.

- STQC Certification: Aeps Fingerprint scanners and Aeps iris scanners must be STQC-certified, ensuring they meet government standards.

- Improved Accessibility: Iris scanning helps users with worn-out fingerprints or difficulty placing fingers, increasing transaction success rates.

- Instant Verification: Transactions are processed in real-time, offering instant, secure, and hassle-free banking.

Key Features of Face Authentication

- Touchless Experience: Aeps india offers a contactless, hygienic, and convenient alternative to fingerprint scanners.

- Enhanced Convenience: Does not require specialized external, physical hardware beyond a smartphone or camera-enabled device.

- High Reliability: Effective for users who cannot use fingerprint scanners due to environmental or physical factors.

- Fast & Secure: Utilizes advanced algorithms to detect liveness and ensure secure authentication.

Key Benefits of Combined Features

- Financial Inclusion: Allows users to access banking services at their doorstep without needing a PIN or debit card.

- Fraud Prevention: Reduces identity theft by linking transactions to unique biometric data (fingerprint or face).

- Easy Setup: Retailers can configure and enable face/biometric authentication through AEPS portal settings.

Read Blog : AEPS Software Provider Company Solutions for High-Volume Transactions

Steps to Aeps API Inrtegration

AePS API integration involves partnering with an NPCI-certified provider, completing KYC, and integrating Aeps biometric device RD services to enable Aadhaar-based transactions. Key steps include acquiring Aeps API credentials (MID/keys), developing backend endpoints for cash withdrawals/balance inquiries, and testing in a sandbox environment.

Steps to AEPS API Integration:

- Partner with an NPCI-Certified Provider: Select a Aeps india offers robust security, high success rates, and competitive commission structures.

- KYC and Registration: Submit business documents, including PAN card, Aadhaar, and bank details, to complete the Aeps onboard process.

- Obtain API Credentials: Receive your Aeps API keys, Merchant Aeps ID (MID), and technical documentation, typically provided within 24-48 hours.

- Acquire and Register Biometric Devices: Purchase Aeps L fingerprint or iris scanners and register them with the manufacture Aeps Device (RD) service.

- Technical Integration:

- Backend: Implement Aeps API endpoints (e.g., cash withdrawal, balance inquiry, mini-statement) using JSON/XML as per documentation.

- Frontend: Configure the UI to capture Aadhaar numbers and biometric data via the RD service.

- Callback URL: Set up a secure HTTPS callback URL to handle transaction status notifications.

- Sandbox Testing: Thoroughly test all transaction types in the Aeps india sandbox environment to ensure proper callback handling and error management.

- Go Live: Move to the production environment to start Aeps API live transactions.

- Monitoring and Compliance: Monitor transactions for reconciliation and adhere to regulations like the “One Operator, One Bank” rule.

The integration process usually involves one-time fees ranging from ₹12,000 to ₹35,000, with providers charging 0.5% to 1% per transaction.

AEPS as a High-Income Business Opportunity

AEPS has emerged as a highly profitable, low-investment business opportunity in India, particularly for local retailers in rural and semi-urban areas. It enables shop owners to turn their premises into “mini-banks” or “banking points” by offering essential Aeps banking services like cash withdrawals, balance inquiries, and mini-statements using only a customer’s Aadhaar number and biometric authentication.

Key Earning Potential and Profitability

AEPS is considered a high-income opportunity because it allows retailers to generate daily income through commissions on every transaction.

- Commission Structure: Retailers can earn up to ₹15 per transaction for high-value cash withdrawals (typically ₹3,000–₹10,000).

- Monthly Earnings: Active agents can earn between ₹10,000 and ₹30,000+ per month, depending on transaction volume and location.

- Additional Revenue: Beyond cash withdrawals, income can be generated from balance inquiries (₹1–₹5), mini-statements (₹2–₹7), and best Aadhaar Pay.

- High-Volume Incentives: Aeps india offer extra monthly bonuses (e.g., ₹2,000+) for high volume Aeps agents processing 150-200+ transactions.

Advantages for Retailers

- Increased Footfall: Providing Aeps banking service attracts more customers, which can boost sales of regular products.

- Low Initial Investment: The Aeps setup requires minimal capital a smartphone or computer, a stable internet connection, and an STQC-certified Aeps biometric scanner (approx. ₹2,000–₹3,000).

- No Need for Large Cash Reserves: Retailers can use their daily sales cash to facilitate withdrawals, as the money is instantly settled into their bank account.

- High Demand: Especially in rural areas, it serves as an essential alternative to distant bank branches and ATMs.

- Secure Transactions: Biometric authentication (fingerprint/face) ensures that only the account holder can authorize the transaction.

Key Considerations for 2026

- Mandatory L1 Devices: As of 2026, the use of Level 1 Buy L1certified biometric devices is mandated for enhanced security.

- “One Operator, One Bank” Rule: New regulations require agents to link with only one acquiring bank, with mandatory re-KYC for agents inactive for three months.

- Face Authentication: High commission Aeps platform are now integrating face authentication alongside fingerprints for faster, more secure verification.

- Transaction Limits: Typically capped at ₹10,000 per transaction and ₹50,000 daily.

How to Earn More Commission with AEPS India Platform

To earn commissions AEPS platform, register as a retailer with a certified Aeps india, obtain a biometric scanner, and perform banking transactions like cash withdrawals or balance inquiries. Retailers typically earn ₹1 to ₹15+ per transaction, with higher earnings on ₹3,000+ transactions.

Steps to Start Earning AEPS Commission

- Select a Trusted AEPS Provider: Register with Aeps India and Noble web studio to ensure secure transactions and competitive rates.

- Required Documents & Setup: You will need your Aadhaar card, PAN card, a bank account for settlements, and a UIDAI-certified Aeps biometric device (e.g.,Mantra scanner).

- Complete KYC & Training: Complete the mandatory, often digital, Aeps KYC process and train on the High volume Aeps platform to handle biometric authentication securely.

- Perform Transactions: Aeps india offer services like cash withdrawals, balance inquiries, and mini-statements to customers.

Commission Structure and Maximizing Earnings

- Transaction Slab: Commission is generally tiered based on the withdrawal amount. Highest earnings (up to ₹15+) are for transactions above ₹3,000.

- Cash Withdrawal Rate (Approx. 2026):

- ₹100 – ₹999: ₹2.00

- ₹1,000 – ₹1,499: ~₹3.00

- ₹1,500 – ₹1,999: ~₹4.50

- ₹2,000 – ₹2,499: ~₹5.50

- ₹3,000 – ₹10,000: ₹13 – ₹15+

- Non-Cash Services: Balance inquiries and mini-statements offer lower commissions, typically ₹1–₹5.

- Volume Bonuses: Highest volume Aeps agents (100+ transactions/month) often receive extra monthly incentives, sometimes up to ₹2,000.

Tips for Success

- Instant Settlement: Highest earning Aeps platform offering real-time or daily wallet settlement to maintain liquidity.

- High-Footfall Location: Operating in rural or semi-urban areas with limited ATM access increases transaction volume.

- Build Trust: Ensure secure transactions with two-factor authentication to increase customer loyalty.

Read Blog : Top 10 AEPS API Providers in India (2026)

Earn Up to ₹15 Commission Per AEPS Transaction

Based on 2026 industry data, Aeps india offer high commissions for AEPS transactions, with top rates reaching up to ₹15–₹20 per transaction for agents, particularly for high-value cash withdrawals.

Aeps india offers a highest commission structures in the market for AEPS retailers.

- For Super Prime Retailers, the Aeps platform provides up to ₹15 commission on every AEPS transaction.

Up to ₹15 commission per AEPS transaction

- This helps retailers earn better income on daily transactions. Because of its attractive payouts and transparent system, Aeps india is considered one of the rewarding Aeps platform.

- The rewarding AePS platforms in India, as of early 2026, are characterized by high commission structures, real-time settlements, and, in some cases, free Aeps onboarding for retailers. Highest commission earning Aeps platform allow shopkeepers to turn their businesses into banking points, earning up to ₹15–₹16 per transaction.

Here are the key details regarding the “Earn Up to ₹15 Commission Per AEPS Transaction” offer:

Top High-Commission AEPS Platforms (2026)

- Aeps india: Aeps india offers a high commission structure of up ₹13 + ₹2 bonus (total ₹15) commission for “Super Prime Retailers” on cash withdrawals.

- Noble Web Studio: Known for providing high commission structures, ranging from ₹12 to ₹15+ per transaction for Super Prime Retailers.

Typical High-Commission AEPS Structure (2026)

Commission is usually tiered based on the withdrawal amount. The highest payouts are for transactions between ₹3,000 and ₹10,000:

- ₹3,000 – ₹10,000: ₹10 – ₹15+ per transaction.

- ₹2,500 – ₹2,999: ₹5 – ₹7 per transaction.

- ₹2,000 – ₹2,499: ~₹5.50 per transaction.

- ₹1,500 – ₹1,999: ~₹4.50 per transaction.

- Below ₹1,000: ~₹2.00 per transaction.

- Balance Inquiry/Mini Statement: ₹1 – ₹5 per transaction.

Key Features and Tips for High-Commission AEPS

- Key Features: High commission Aeps services often feature instant (T+0) settlement for liquidity, Aadhaar Pay for high-value transactions, biometric authentication, and low cost Aeps onboarding.

- Maximizing Earnings: To earn up to ₹15+ per transaction, focus on high-value (₹3,000+) withdrawals, increase transaction volume for monthly bonuses, and utilize best Aeps platforms that combine AEPS with other services like DMT and BBPS.

Why Aeps india Offers Higher Commission

High AEPS commissions are offered to incentivize agents and retailers to act as “mini-bank branches,” providing crucial cash withdrawal and banking services to rural and underbanked populations. As of 2026, Top Aeps platforms offer commissions up to ₹15–₹20 per transaction to attract high-volume agents and encourage the adoption of digital, cardless transactions.

Typical 2026 High-Commission Structure:

- ₹100 – ₹999: ~₹2.00

- ₹2,000 – ₹2,999: ~₹5.50 – ₹8.00

- ₹3,000 – ₹10,000: Up to ₹15–₹20 (or 0.40%–1% of transaction value)

- Balance Inquiry/Mini Statement: ~₹1 to ₹5 per transaction

Here are the primary reasons why some providers offer higher AEPS commissions:

- Tiered Commission Structures: Commissions are not flat; they rise with the value of the transaction. High-value withdrawals (e.g., ₹3,000–₹10,000) offer the highest Aeps commission payouts, often up to ₹13–₹15+, encouraging agents to handle larger transactions.

- Incentivizing High Volume & “Super Prime” Agents: To secure loyal agents, top Aeps platform like Aeps India offer premium, higher-commission structures (e.g., ₹15 per transaction) for “Super Prime” agents who achieve high daily transaction volumes.

- Increased Customer Footfall: Aeps india offering higher Aeps commissions benefit from increased foot traffic, which leads to higher, faster turnover for their primary, non-banking products (cross-selling).

- Distributor/Agent Network Growth: Aeps India or Noble Web Studio use high commissions to build a strong network of retailers, ensuring they remain competitive against other fintech companies.

- Financial Inclusion Mandate: The government and NPCI aim to bring banking services to remote areas. Higher payouts encourage agents to operate in underserved regions where setting up a physical bank branch is not viable.

- Bundled Service Income: High paying Aeps platform encourage using additional services (Mini-statements, Aadhaar Pay, Utility Bill Payments) alongside AEPS, multiplying the total earnings for the agent.

Aeps India and Noble Web Studio are noted for offering higher, competitive commissions to maximize retailer income.

Higher Aeps commission means better profitability and faster business growth for retailers.

Step-by-Step Guide to Start AEPS Business with Aeps India

Starting an Aadhaar Enabled Payment System business involves registering with an authorized BC (Business Correspondent) agent or NPCI-approved Aeps india, completing KYC with your Aadhaar/PAN/bank details, Buy Aeps biometric device (Mantra), and using a smartphone or PC to provide banking services like cash withdrawals and balance inquiries.

Step-by-Step Guide to Start an AEPS Business:

- Meet Eligibility Criteria: You must be 18+ years old, possess a shop (physical location preferred), a smartphone or PC with internet, and a bank account for settlements.

- Select an Authorized AEPS Provider/BC: Choose a reputable AEPS provider such as Aeps india and Noble web studio.

- Complete Registration and KYC: Register on the best Aeps portal/best Aeps app and submit required documents: PAN Card, Aadhaar Card, Bank account proof (cancelled cheque), and shop address proof.

- Purchase Biometric Device: Acquire an Purchasing Aeps fingerprint or Purchase Aeps iris scanner (e.g., Mantra) and ensure it has registered device (RD) service functionality.

- App Installation and Training: Install the Aeps Android app or web portal. Complete the required training regarding transaction safety, compliant banking practices, and agent mapping.

- Activate Services: Once KYC is verified (usually within 24-48 hours), log in, connect your biometric device, and begin providing Aeps services like Cash Withdrawal, Balance Enquiry, and Mini Statement.

- Manage Settlement: Earn commissions instantly on Aeps transactions, which are accumulated in Aeps india wallet and can be transferred to your bank account.

Key Requirements:

- Documents: Aadhaar Card, PAN Card, Bank Account, Mobile Number.

- Hardware: Android Phone/PC, Internet Connection, Biometric Fingerprint Scanner.

- Aadhaar Linkage: Ensure your bank account is linked to your Aadhaar for secure settlement.

Read Blog : The Ultimate Guide to AEPS API: Everything You Need to Know in 2025

How to Become an Aeps india AEPS Retailer

To become an AEPS retailer, you must register with an authorized Aeps india and Noble web studio Key requirements include a physical shop, PAN card, Aadhaar card, a smartphone/PC, and a biometric Aeps fingerprint scanner. The process involves online Aeps registration, Aeps KYC verification, and training to enable services like cash withdrawals and balance inquiries.

Steps to Become an AEPS Retailer

- Meet Eligibility Criteria: You must be an Indian citizen, at least 18 years old, and own a physical shop (e.g., Kirana store, mobile shop).

- Select a Service Provider: Choose a registered Aeps india and Noble web studio.

- Register Online: Visit the Aeps indi website to fill out the AEPS retailer registration form with your business and personal details.

- Complete KYC Verification: Submit required documents, which typically include your PAN card, Aadhaar card, and proof of address.

- Set Up Hardware: Purchase Aeps biometric device (fingerprint scanner).

- Training and Activation: Complete the required training on using the top Aeps portal. Once verified, your Aeps agent ID will be activated.

Required Documents & Setup

- Documents: Aadhaar Card, PAN Card, Bank Account Details (for commission payout), Passport Size Photo.

- Hardware: Smartphone (Android) or Laptop/Desktop, Internet Connection, Buying Aeps Biometric Device (Mantra).

Key Benefits

- Earnings: Earn commissions on every Aeps transaction.

- Services: Offer cash withdrawal, balance inquiry, and mini-statement services.

- Setup: Generally quick Aeps onboarding, often with low or zero Aeps setup costs.

Handling Aeps Transaction Issues

For AePS transaction issues like failed debits, immediately contact your bank to report the transaction ID, date, and amount. Failed, deducted amounts usually auto-reverse within 24-48 hours, up to 7 working days. If unresolved, file a complaint with your bank or the RBI Ombudsman.

Key Steps for Handling AePS Failures:

- Verify Deduction: Check your bank account via mobile Aeps app or mini-statement to confirm the money was actually deducted.

- Get Evidence: Obtain a receipt with a transaction ID or reference number from the agent.

- Contact Bank Immediately: Reach out to your bank’s customer service to report the failure.

- Report Fraud: If you suspect unauthorized transactions, contact Aeps india immediately.

- Check Tech & Network: Ensure the agent’s internet connection is stable and the biometric device is functioning.

- Use Security Measures: Lock your Aadhaar biometrics via the Aeps india website to prevent unauthorized usage.

Common Reasons for Failure:

- Weak internet signal.

- Incorrect Aadhaar number entry.

- Fingerprint scanning issues.

- Technical glitches at the bank or server.

Why AEPS is the Future of Assisted Digital Banking

The Aadhaar Enabled Payment System (AePS) is widely regarded as the future of assisted digital banking, particularly in India, because it removes traditional barriers such as the need for physical debit cards, PINs, or smartphones by utilizing a person’s Aadhaar number and biometric authentication (fingerprint or iris scan) to perform banking transactions. It bridges the gap between rural, unbanked populations and the formal financial system by transforming local, trusted, and accessible shops into “micro-ATMs”.

Here is why AEPS is the future of assisted digital banking:

1. Unmatched Accessibility and Inclusivity

- Doorstep Banking: AePS brings banking to remote areas where traditional bank branches and ATMs are scarce or non-existent.

- No Technical Expertise Required: Users do not need to know how to use complex smartphone Aeps software or apps or remember PINs; they only need their unique biometrics.

- Financial Inclusion: It empowers millions of unbanked, elderly, and rural citizens to access essential financial services right in their neighborhood.

2. High-Level Security with Biometrics

- Biometric Authentication: By using fingerprint or iris scans, AEPS reduces the risk of fraud associated with stolen cards or forgotten PINs.

- Real-time Verification: Transactions are authenticated in real-time against the UIDAI (Unique Identification Authority of India) database, ensuring only the genuine account holder can authorize a transaction.

- Enhanced Security Measures: The National Payments Corporation of India (NPCI) has introduced, and continues to update, security features like liveness detection and, as of 2026, mandatory two-factor authentication (biometric + OTP) for high-value transactions.

3. Key Benefits for Users and Agents

- For Users: Provides instant cash withdrawals, balance enquiries, and mini-statement services without traveling long distances.

- For Agents/Retailers: It acts as a high-income business opportunity. Local shopkeepers (Business Correspondents) can earn significant commissions (up to ₹15+ per transaction) while increasing customer footfall to their shops.

4. Direct Benefit Transfers (DBT)

- Efficient Delivery: AePS serves as a vital channel for the government to directly transfer subsidies, pensions, and MGNREGA wages into the beneficiaries’ accounts, reducing leakages.

5. Future Growth and Evolving Technology

- Integration with Future Tech: Future Aeps software development include the integration of AI for real-time fraud detection and blockchain for enhanced security.

- Broader Financial Services: Beyond cash, AePS is expanding to offer micro-loans, insurance, and other financial services, turning local shops into comprehensive “mini-banks”.

Challenges Being Addressed: While AePS faces challenges like internet connectivity issues and occasional biometric failures, ongoing improvements in technology and infrastructure, combined with its role in the “Digital India” initiative, solidify its position as the future of inclusive, assisted banking.

Read Blog : Best AEPS API Service in India for AEPS Cash Withdrawal

Why AEPS Business is the Best Digital Banking Opportunity in India

The Aadhaar-Enabled Payment System (AePS) is arguably India’s top digital banking opportunity due to its low-investment, high-commission, and high-demand nature, allowing local shopkeepers to become “mini-bankers”. By enabling secure, biometric-based cash withdrawals, deposits, and fund transfers for rural and underbanked populations, it provides an essential service with instant settlements.

Key Reasons Why AEPS is the Best Opportunity:

- High Revenue & Low Investment: Requires minimal infrastructure (smartphone + biometric scanner), allowing retailers to earn commissions up to ₹12-₹15 per transaction, creating a sustainable, high-ROI business.

- Financial Inclusion & Demand: It bridges the gap between urban and rural banking, serving millions who lack access to physical bank branches or ATMs.

- Secure & User-Friendly: Transactions are authenticated via biometrics (fingerprint/iris), which eliminates the need for cards or PINs, offering high security against fraud.

- Government Support (DBT): It is crucial for delivering government Direct Benefit Transfers (DBT), such as pensions and subsidies, ensuring constant demand.

- Increased Footfall: For shop owners, offering AEPS brings more customers to their store, increasing trust and boosting sales of core products.

- Instant Settlements: Aeps india offer 99.9% uptime and instantaneous, real-time settlements (T+0), keeping cash flow efficient.

This system is rapidly transforming India into a cashless economy by providing easy access to financial services at the doorstep, making it a lucrative and socially impactful business model.

Why Choose Aeps india for AEPS Business with Biometric & Face Authentication

Choosing a Aeps india for AEPS business with biometric and face authentication offers high security, 99.9% uptime, and up to ₹15 commission per transaction. These services enable swift, contactless, and secure, Aadhaar-based transactions, increasing customer trust and footfall, while allowing instant T+0 settlements for better working capital management.

- Advanced Security & Compliance: Aeps india ensure NPCI, RBI, and UIDAI compliance, reducing fraud risk with encrypted biometric and, increasingly, face authentication.

- Enhanced Reliability & Speed: High performance Aeps platform offer 99.9% uptime, resulting in high transaction success rates (98%+).

- Increased Income & Competitive Payouts: Agents can earn ₹12–₹15 per transaction, with additional earnings from integrated Aeps services like Micro ATMs and bill payments (BBPS).

- Instant Settlement (T+0): Immediate settlement of funds (T+0 or same-day) ensures that working capital is always available for transactions, preventing cash flow issues.

- Convenience & Accessibility: Face authentication provides a contactless, hygienic, and efficient alternative, especially when fingerprint quality is poor or for elderly customers.

- Robust Support: 24/7 technical support is provided to resolve issues, ensuring minimal service downtime.

Key Considerations for Selection:

- Ensure the Aeps india supports L1-certified (Level 1) biometric devices for 2026 security standards.

- Look for Aeps india offering a comprehensive suite, including Aeps API integrate, to scale operations.

Read Blog : Best AEPS Portal in India 2026: Complete Guide

Future Trends AEPS Business with Biometric & Face Authentication

Future AEPS business trends focus on enhancing security and user experience by integrating AI-driven face authentication alongside traditional fingerprint biometrics, ensuring higher success rates and reduced fraud. Key trends include mandatory L1 biometric Aeps devices, “one operator-one bank” rules, 24/7 instant settlement, and multi-modal authentication, driving secure financial inclusion in rural areas.

Key Future Trends in AEPS Business (2026-2028):

- Face Authentication & Liveness Detection: Integration of AI-powered facial recognition with liveness detection (distinguishing live vs. fake) is becoming standard to reduce spoofing and help seniors with poor fingerprints.

- Mandatory L1 Devices: The use of STQC-certified, Level 1 (L1) compliant biometric devices is becoming mandatory for all AEPS transactions, providing stronger encrypted security.

- Multi-Modal Biometrics: Combining fingerprint, iris, and facial recognition for higher authentication accuracy and security.

- AI for Fraud Prevention: Machine learning is used for real-time risk assessment and detecting fraudulent activities.

- “One Operator, One Bank” Rule: Increased security by restricting each agent (Business Correspondent) to link with only one acquiring bank.

- Blockchain Technology: Future implementation of blockchain for immutable and transparent transaction records.

- Expanded Service Portfolio: Agents are evolving into fintech hubs offering, besides cash withdrawal/balance inquiry, services like micro-loans, insurance, and UPI integration.

Impact on Business Growth:

- Higher Earnings: Retailers can earn up to ₹15 commission per transaction.

- Customer Trust: Enhanced security builds trust, leading to higher transaction volumes.

- Increased Footfall: Acting as a mini-bank increases customers in rural, underbanked areas.

Conclusion

Starting an AEPS business with biometric and face authentication is one of the smartest ways to grow in the digital banking sector in India. As more customers look for secure and easy banking services, the demand for Aadhaar Enabled Payment System (AEPS) with advanced authentication technology is increasing rapidly. Retailers and agents who adopt biometric AEPS service and face authentication best AEPS API can build stronger customer trust and earn higher commission income.

With secure fingerprint authentication and face verification system, transactions become safer and faster. This reduces fraud risk, improves transaction success rate, and ensures smooth cash withdrawal, balance enquiry, mini statement, and Aadhaar to Aadhaar fund transfer services. Aeps india one of the trusted AEPS service provider in India that offers real-time processing, high server uptime, fast settlement cycle, and strong technical support helps agents run their business without interruption.

For retailers, AEPS is not just a service it is a strong and growing income opportunity. It allows shop owners to earn money on every transaction while helping customers with basic banking services.With Aeps india, Super Prime Retailers can earn up to ₹15 commission on each successful transaction. This means more daily income and better profit compared to Aeps service platforms in the market. Because transactions happen regularly, retailers get a steady earning source. The more transactions you complete, the more you earn. This makes AEPS a simple, scalable, and reliable business opportunity for small shop owners and rural retailers.

The combination of AEPS API integrating, biometric device support, face authentication technology, and multi-bank connectivity makes your platform more powerful and future-ready. As digital payments and financial inclusion continue to expand across rural and urban India, agents who upgrade to advanced AEPS solutions can increase daily transactions and maximize their commission earnings.

Partnering with a reliable platform like AEPS India ensures secure onboarding, transparent commission structure, and scalable Aeps business growth. If you want long-term success in the fintech industry, investing in a secure AEPS business with biometric and face authentication is the right decision.

Start today, serve more customers, and build a profitable AEPS business with higher income potential and trusted digital banking services in India.

FAQ – AEPS Business with Biometric & Face Authentication (2026 Guide)

AEPS Business with biometric & face authentication allows retailers and agents to offer Aadhaar-based banking services like cash withdrawal, balance enquiry, and mini statement using both fingerprint and face verification. This ensures higher transaction success and secure payments.

In biometric AEPS, the customer uses their Aadhaar number and fingerprint to authenticate transactions. The system verifies the fingerprint through a secure AEPS API provider like Aeps india in real-time, completing the transaction instantly.

Face authentication helps when fingerprint verification fails. It provides a backup verification method, reduces transaction failures, and increases customer trust. Retailers can complete transactions quickly, earning more commission per transaction.

Anyone can start this high commission AEPS business, including:

Retail shop owners

CSC operators

Payment service providers

Fintech startups

Agents in rural and urban areas

It is a low-investment, high-profit digital business in India.

A Aeps india allows you to offer:

AEPS cash withdrawal service

Balance enquiry

Mini statement

Aadhaar-based banking transactions

All services can be accessed through secure biometric and face authentication devices.

Commission depends on the Aeps india and transaction type. High commission AEPS providers like Aeps india offer attractive margins on every cash withdrawal. Adding face authentication increases transaction success, resulting in higher total commission.

To start with a Aeps india, you need:

Aadhaar card

PAN card

Bank account details

Passport-size photo

Biometric device & face authentication setup

KYC verification is mandatory before activation.

Top AEPS service providers like Aeps india offer instant or same-day settlement. Fast settlement ensures smooth cash flow and timely commission for agents and retailers.

You need a certified biometric fingerprint scanner, a device or camera for face authentication, stable internet, and registration with a trusted AEPS API provider like Aeps india.

Yes. Using both biometric and face authentication, transactions are encrypted and fraud-resistant. It ensures customer data is secure while offering reliable and fast digital banking services.

Absolutely. AEPS business is highly popular in rural and semi-urban areas, where access to banks and ATMs is limited. Retailers become local banking points, increasing both customer visits and transaction volume.

Look for:

Secure biometric & face authentication devices

High transaction success rate

Fast settlement system

Transparent commission structure

24/7 technical and customer support

A reliable provider ensures smooth operations and maximum earnings.

Yes. By reducing failed transactions and offering secure Aeps banking api services, AEPS business with biometric & face authentication increases daily transaction volume, resulting in higher commission and profit.

Digital payments and Aadhaar-based banking are growing rapidly in India. Adding face authentication ensures more successful transactions, builds trust, and provides a scalable income opportunity for retailers and agents across urban and rural areas.

With growing digital payments and government initiatives, AEPS business is expanding rapidly. Retailers and fintech startups can earn steady income, expand services, and scale business with advanced authentication features in 2026.

Aeps india provides a secure, scalable, and high-commission AEPS platform in India with biometric and face authentication. Our Aeps solution ensures fast settlement, multi-bank support, high transaction success rate, and technical assistance helping retailers and agents maximize earnings and grow their AEPS business in 2026.

Best AEPS Platform in India 2026: Features, Benefits & Business Opportunities

AEPS Registration in India: Complete Step-by-Step Guide 2026