Aadhaar Enabled Payment System API Explained: Complete Guide

The Aadhaar Enabled Payment System (AEPS) API has become a powerful solution for businesses looking to offer secure and instant banking services in India. With the help of an AEPS API, fintech companies, service providers, and retailers can allow customers to withdraw cash, check balance, view mini statements, and transfer money using only their Aadhaar number and biometric authentication without debit cards or internet banking.

An AePS API (Aadhaar Enabled Payment System Application Programming Interface) is a software bridge developed by the NPCI that enables businesses to integrate secure, biometric-based banking services directly into their top Aeps apps or websites. It allows users to perform transactions like cash withdrawals, deposits, and balance inquiries using their Aadhaar number and fingerprint, turning any shop with a smartphone/micro-ATM into a banking access point.

For businesses, the Aadhaar Enabled Payment System API in India opens new opportunities to earn daily commission while supporting financial inclusion. A reliable AEPS API ensures fast transactions, high success rate, strong security, and full RBI and NPCI compliance.

By integrating the AEPS API in India, businesses can allow customers to complete transactions using only their Aadhaar number and biometric authentication, without the need for debit cards or PINs. This makes AEPS one of the most accessible and trusted payment systems, especially in rural and semi-urban areas.

As digital payments continue to grow, the demand for AEPS API integration in India has increased rapidly. Businesses use the AEPS API provide fast, reliable, and real-time transactions, especially in rural and semi-urban areas where traditional banking access is limited. Supported by NPCI and RBI guidelines, AEPS ensures safe and compliant transactions across all major banks in India.

AEPS India provides a reliable and NPCI-compliant AEPS API solution that helps businesses expand digital financial services, especially in rural and semi-urban areas. This AEPS balance inquiry API connects directly with banks and enables smooth, real-time transactions while maintaining high security standards.

This complete guide on Aadhaar Enabled Payment System API will help you understand how AEPS API works, its benefits for businesses, and why it plays a key role in India’s digital banking ecosystem. If you are planning to offer AEPS services or expand your fintech solutions, knowing how the AEPS API integration works is the first step toward success.

What is Aadhaar Enabled Payment System API?

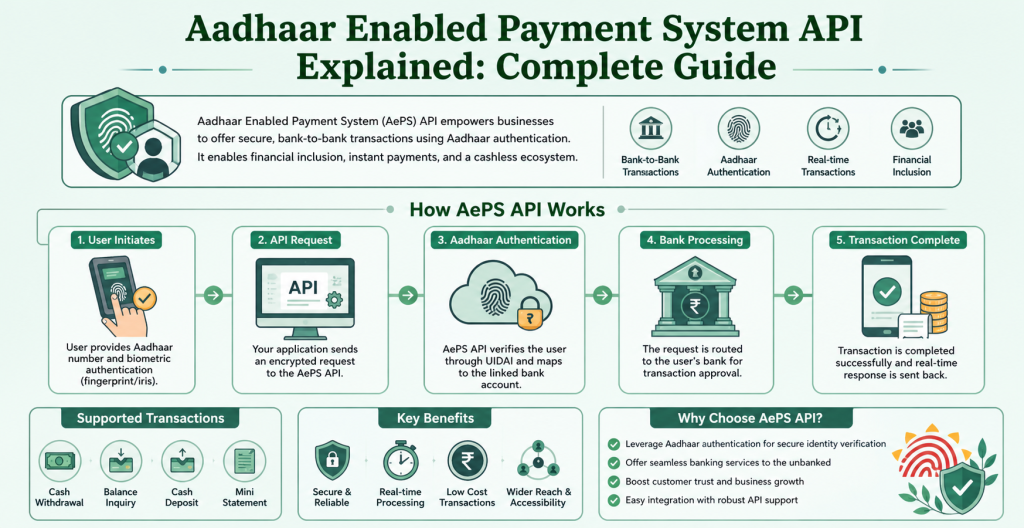

The Aadhaar Enabled Payment System API is a secure, developer-friendly interface that enables, allows, and powers financial transactions such as cash withdrawals, deposits, balance inquiries, and mini-statements using only an Aadhaar number and biometric authentication (fingerprint/iris). It enables, powered by NPCI and UIDAI, facilitates cardless, PIN-less, interbank transactions through Business Correspondents (BCs) at retail points.

Aadhaar Enabled Payment System API Work

Aadhaar Enabled Payment System API enables businesses to integrate banking services cash withdrawal, balance inquiry, mini-statement, and fund transfer directly into apps or websites, turning into micro ATM devices. It uses Aadhaar-based biometric authentication (fingerprint) for secure, real-time transactions linked to a customer’s bank account.

How AEPS API Works (Workflow):

- Initiation: A user provides their Aadhaar number, bank name, and fingerprint on a merchant’s app or website.

- Authentication: The Aeps API sends this data securely to the NPCI (National Payments Corporation of India) network.

- Verification: The Aeps API verifies the data with the Unique Identification Authority of India (UIDAI) and the respective bank.

- Processing: If successful, the transaction is processed in real-time; the customer’s account is debited/credited, and the merchant’s wallet is updated.

- Confirmation: The merchant receives a confirmation receipt, and the customer receives an SMS.

Types of Aadhaar Enabled Payment System API

Aadhaar Enabled Payment System API facilitate essential banking services using Aadhaar authentication and biometrics. Key types include Cash Withdrawal, Balance Inquiry, Mini Statement, Cash Deposit, and Fund Transfer. Additionally, specialized types like Aadhaar Pay (merchant payments) and Direct Benefit Transfer (DBT) are available for enhanced financial transactions.

Key Types of AEPS API Services

- Cash Withdrawal (CW): Allows customers to withdraw money from their linked bank account at a micro-ATM or agent point using Aeps biometric authentication.

- Balance Inquiry (BI): Enables real-time checking of the account balance via biometric verification.

- Mini Statement (MS): Provides a snapshot of the last few transactions performed in the account.

- Cash Deposit (CD): Enables agents to deposit cash directly into a customer’s Aadhaar-linked account.

- Aadhaar Pay: A merchant-focused AEPS mini statement API that facilitates cashless payments for purchases using Aadhaar authentication.

- Fund Transfer: Enables secure transfer of funds between Aadhaar-linked accounts.

Technical API Classification

- Transaction API: Handles the core financial operations like CW, CD, and BI, with specific service types (e.g.,

service_type=2for Cash Withdrawal). - Verification/KYC API: Used to authenticate the customer’s identity via UIDAI before processing transactions.

- White Label AEPS API: A customizable, branded solution allowing businesses to offer full AEPS services alongside other banking products.

These Aeps API ensure secure, real-time banking services, often integrating Aeps biometric scanners and micro ATM device.

Services Offered Through Aadhaar Enabled Payment System API

AEPS API facilitate essential, secure, and interoperable banking services using Aadhaar-linked biometric authentication. Key services include Cash Withdrawal, Balance Enquiry, Mini Statement, Cash Deposit, and Aadhaar Pay (merchant payments), enabling instant transactions and real-time settlement for users without needing debit cards or PINs.

Core Services Offered Through AEPS API:

- Cash Withdrawal: Allows customers to withdraw money from their Aadhaar-linked bank account via a business correspondent or micro ATM.

- Balance Enquiry: Enables real-time checking of the bank account balance using biometric authentication.

- Mini Statement: Provides a snapshot of the last few transactions, assisting users in tracking their account activity.

- Aadhaar to Aadhaar Fund Transfer: Enables instant transfer of money between two Aadhaar-linked accounts.

- Cash Deposit: Supports depositing cash into a linked bank account.

- BHIM Aadhaar Pay: Facilitates merchant payments, allowing customers to pay for goods/services using their Aadhaar number and Aeps biometrics.

- E-KYC: Facilitates electronic Know Your Customer verification, often used for instant Aeps onboarding.

Who Can Use Aadhaar Enabled Payment System API in India

In India, the AePS API can be used by authorized financial institutions, fintech companies, banks, and Business Correspondents (BCs) to enable secure, biometric-based,, and Aadhaar-linked banking transactions like cash withdrawals, balance inquiries, and mini statements. It is specifically designed to facilitate financial services through Agents, Micro ATMs, and kiosk operators, enhancing, digital banking access in rural and remote areas.

Key users and stakeholders authorized to use or integrate AEPS API include:

- Financial Institutions & Fintechs: Banks and fintech startups that integrated Aeps API to provide banking services.

- Business Correspondents (BCs) & Agents: Authorized agents who, on behalf of banks, provide services in areas without physical bank branches.

- Retailers & Small Business Owners: Shopkeepers, Kirana store owners, and kiosk operators who act as banking agents to turn their shops into micro-ATMs.

- CSC Center Operators: Common Service Centers (CSCs) that provide rural, digital access.

Requirements for Using AEPS API:

- Technical Setup: An active Aeps API integration with a certified AePS service provider like Aeps india.

- Hardware: A registered Aeps Biometric (fingerprint or iris) scanner for authentication.

- Eligibility: Must be an adult citizen of India, typically with KYC documents (Aadhaar, PAN) and a, registered, business entity.

- Compliance: Adherence to RBI and NPCI regulations.

The end-users, or customers, are any Indian residents with an Aadhaar-linked bank account.

Aadhaar Enabled Payment System API Use Cases in India

AEPS API in India enables secure, cardless banking by allowing users to perform transactions using Aadhaar authentication and biometrics (fingerprint/iris) through Business Correspondents (BC) or micro-ATMs. Key use cases include cash withdrawals, balance inquiries, mini-statements, fund transfers, and Direct Benefit Transfers (DBT). It is crucial for financial inclusion in rural areas, turning local shops into mini-banks.

Key AEPS API Use Cases in India:

- Cash Withdrawal & Deposit: The primary use case, enabling users to withdraw or deposit cash at local retail outlets (micro-ATMs) without a debit card or PIN.

- Balance Inquiry & Mini Statement: Instant, secure, and real-time checking of bank account balances and transaction history using biometrics.

- Aadhaar-to-Aadhaar Fund Transfer: Enables secure, intrabank or interbank transfers between two Aadhaar-linked bank accounts.

- Direct Benefit Transfer (DBT) Disbursement: Facilitates government welfare payments, such as subsidies, pensions (NREGA), and scholarships, directly into beneficiaries’ Aadhaar-linked accounts.

- Merchant Payments (BHIM Aadhaar Pay): Allows merchants to accept payments from customers via Aadhaar authentication, particularly useful in areas with low card penetration.

- eKYC (Electronic Know Your Customer): Provides a paperless, real-time method for verifying customer identity for account opening or SIM card activation.

- Rural Banking & Financial Inclusion: Enables Banking Correspondents (BCs) or Village Level Entrepreneurs (VLEs) to provide essential banking services in remote areas, reducing the need for physical bank branches.

Best AEPS API helps Fintechs, banks, and startups expand their service reach, offering a secure, cost-effective, and user-friendly banking experience.

Documents & KYC Requirements for Aadhaar Enabled Payment System API

AEPS API integration requires mandatory KYC for agents/merchants, including Aadhaar card, PAN card, bank account details (passbook/cancelled cheque), and a passport-sized photo. A UIDAI-certified Aeps biometric device (fingerprint/iris scanner) is essential for agent Aeps onboarding and transactions. Business entities may also need GST or incorporation documents.

Essential Documents & Requirements for AEPS Agent Registration

- Aadhaar Card: Mandatory for Aeps e-KYC verification.

- PAN Card: Required for business or individual registration.

- Bank Account Details: A cancelled cheque, bank statement, or the first page of the passbook for settlement of funds.

- Active Mobile Number: Must be linked to Aadhaar for OTP verification.

- Passport-Sized Photograph: For identification purposes.

- Biometric Device: A STQC-certified Aeps biometric scanner (e.g., Mantra) is required.

- Business Address Proof: Optional but often required for physical verification.

Additional Requirements for Corporate/White Label AEPS API

- Company Incorporation Documents: Certificate of Incorporation, MOA, and AOA.

- GST Certificate: Required for business entity registration.

- Board Resolution/Director ID: For company verification.

- Domain & SSL Certificate: For Aeps API website hosting.

Customer Requirements

Customers using the best AEPS service only need their Aadhaar number and their biometric data (fingerprint) for authentication.

Key Considerations

- Onboarding Process: Involves submitting documents via an top Aeps API provider like Aeps india or Aeps portal followed by Aeps KYC verification.

- Minimum Age: 18 years.

- Active Account: The agent’s bank account must be fully functional and KYC-compliant.

Aadhaar Enabled Payment System API Requirements and Eligibility

AEPS API integration allows businesses to offer Aadhaar-based banking services (cash withdrawal, balance inquiry, mini-statement) by connecting with NPCI-certified Aeps india. Key requirements include Indian citizenship, age 18+, Aadhaar-linked bank account, PAN card, and a UIDAI-certified Aeps biometric scanner (fingerprint/iris). Aeps api Setup involves KYC and technical integration Aeps API into existing Aeps platforms.

AEPS API Eligibility Criteria

- Age: Minimum 18 years.

- Citizenship: Indian National.

- Location: A physical shop, office, or kiosk is required.

- Banking: An active bank account, ideally linked to Aadhaar.

- Verification: Successful completion of KYC (Know Your Customer).

Required Documentation

- Aadhaar Card: Must be linked to a bank account.

- PAN Card: Mandatory for identification and tax purposes.

- Proof of Business: Shop & Establishment certificate or GST registration.

- Bank Account Details: Cancelled cheque or bank statement.

- Photograph: Recent passport-sized photo.

Technical and Hardware Requirements

- Biometric Device: A registered (RD) fingerprint scanner or iris scanner (e.g. Mantra).

- Hardware: Smartphone (Android) or PC/Laptop.

- Internet: A stable, high-speed internet connection.

- Software: Integrating AEPS API via a trusted Aeps service provider like Aeps India.

API Integration Details & Cost

- Integration Type: Either via a white label Aeps solution or a direct B2B Aeps API integration.

- Setup Fees: Aeps API integration Cost vary from ₹8,000 to over ₹1,00,000+ for, with white label Aeps solutions often costing ₹15,000–₹30,000.

- Approval Time: Following documentation, approval for activation is typically processed within 24–48 hours.

- Compliance: The Aeps india must be registered with the National Payments Corporation of India (NPCI).

Key Considerations

- No RBI License Needed: Direct RBI licensing is not required for agents; they operate under the license of the partnering bank or aggregator.

- Limits: Maximum withdrawal limit is generally up to ₹50,000 per transaction, with additional options like Aadhaar Pay for higher amounts.

- Commission: Agents earn commission on each successful transaction.

Aadhaar Enabled Payment System API for Retailers and Banking Agents

AEPS (Aadhaar Enabled Payment System) API allows retailers and banking agents to offer secure, biometric-based banking services cash withdrawal, balance inquiry, mini-statements, and fund transfers using a customer’s Aadhaar number. It transforms retail shops into “micro-ATMs,” enabling real-time transactions and high Aeps commission earnings without needing physical bank branches, particularly crucial for rural financial inclusion.

Key Features of AEPS API

- Interoperability: Works across multiple banks, allowing customers to access any bank account.

- Biometric Authentication: Secure transactions via fingerprint or iris scan (UIDAI-verified).

- Real-time Processing: Instant, secure, and reliable, with immediate transaction confirmation.

- Minimal Requirements: Only requires a smartphone/computer, internet connection, and a compliant Aeps biometric device.

Benefits for Retailers and Agents

- New Revenue Stream: High commission per transaction, enhancing business income.

- Increased Footfall: Attracts more customers, improving overall sales.

- Low Setup Cost: Minimal investment to start a “mini-bank”.

- Secure Transactions: Reduces fraud risk compared to card-based systems.

Importance of Aadhaar Enabled Payment System API for Businesses

AEPS (Aadhaar Enabled Payment System) API is crucial for businesses, especially in India, by enabling secure, cardless, and PIN-less transactions (cash withdrawal, balance inquiry, mini-statement) directly via biometric authentication. It drives financial inclusion in rural areas, increases customer footfall for retailers, generates new revenue streams through commissions (₹2–₹15+ per transaction), and offers easy, scalable integration for fintech startups.

Key Benefits and Importance for Businesses:

- Increased Customer Footfall & Revenue: Retailers, such as kirana shops, can act as mini-banks, attracting more customers and earning commissions on transactions.

- Financial Inclusion & Reach: Enables businesses to tap into unbanked and rural populations, providing essential banking services without needing physical bank branches.

- Secure & User-Friendly: Utilizes Aadhaar-based Aeps biometric authentication (fingerprint/iris), which is safer than traditional PIN-based transactions, reducing fraud risk.

- Low Infrastructure Costs: Requires minimal investment typically just a smartphone and a biometric device—making it accessible for small businesses.

- Interoperability: Allows customers from any bank to transact, increasing the potential customer base.

- Real-Time Transactions: Aeps India offers high-speed, instant processing, ensuring smooth customer experiences.

- Easy Integration: Aeps India is the Aeps API designed for easy, secure (OAuth 2.0) integration with existing Aeps systems.

Features AEPS API

AEPS (Aadhaar Enabled Payment System) API enables secure, real-time, cardless banking cash withdrawals, deposits, balance inquiries, and mini-statements using Aadhaar-linked biometric authentication (fingerprint/iris). It transforms retail outlets into micro-ATMs, promoting rural financial inclusion by connecting users directly to their bank accounts.

Key Features of AEPS API

- Secure Authentication: Utilizes biometric data (fingerprint or iris scan) matched against Aadhaar records for high security.

- Core Banking Functions: Supports cash withdrawal, cash deposit, mini-statement generation, and balance inquiry.

- Interoperability: Allows customers to access accounts from multiple banks through a single, unified platform.

- Real-Time Processing: Transactions are processed immediately, ensuring instant,, secure, and reliable,, settlements.

- Cardless & PIN-less: Eliminates the need for physical debit/credit cards or PINs, requiring only an Aadhaar number and Aeps biometric verification.

- Easy Integration: Provides developer-friendly documentation for seamless integration into web and mobile applications.

- Fund Transfer: Enables Aadhaar-to-Aadhaar fund transfers, facilitating, efficient, transactions.

- Report Management: Includes tools for tracking transaction history, settlements, and agent performance.

Top AEPS API is highly beneficial for, creating, a, digital,, banking, ecosystem, in, rural, and, semi-urban, areas, through, local, agents.

Benefits AEPS API

Aadhaar Enabled Payment System (AEPS) API enables secure, real-time banking transactions cash withdrawals, balance inquiries, and mini-statements using only biometric authentication and an Aadhaar number. It promotes financial inclusion, especially in rural areas, by eliminating the need for physical debit cards, PINs, or bank visits, while allowing businesses to earn commissions and increase customer traffic.

Key Benefits of AEPS API:

- High Security & Reduced Fraud: Utilizes unique biometric (fingerprint/iris) authentication, which is more secure than traditional PIN-based transactions.

- Enhanced Convenience & Accessibility: Allows users to access banking services at local, trusted retail shops (micro-ATMs), reducing the need to travel long distances.

- Financial Inclusion: Extends banking services to unbanked and underbanked populations, particularly in remote, rural, and semi-urban areas.

- No Physical Card/PIN Required: Users only need their Aadhaar number and biometrics to complete transactions.

- Real-Time Transactions & Settlement: Offers instant, 24/7 transaction processing, which is highly beneficial for urgent cash needs.

- Interoperability: Customers can use any bank account (linked with Aadhaar) at any AEPS-enabled terminal.

- Business Growth & Revenue: Helps fintechs, banks, and CSPs create new revenue streams through commissions and increased footfall.

- Government Benefits Access: Facilitates easy withdrawal of Direct Benefit Transfers (DBT), such as pensions and MNREGA funds.

AEPS API Integration Process

AEPS API Integrating involves partnering with a certified Aeps india and following a structured technical process. You cannot connect directly to the National Payments Corporation of India (NPCI) network.

Here are the steps for the AEPS API integration process:

1. Partner Onboarding and Registration

- Choose a Certified Provider: Aeps india that is licensed by the NPCI and follows Reserve Bank of India (RBI) guidelines.

- Business Registration: Register your business with the Aeps india. This typically involves an online form and signing an agreement.

- Complete KYC: Submit mandatory Know Your Customer (KYC) documents, which usually include:

- Aadhaar Card

- PAN Card

- Bank account details (cancelled cheque/passbook)

- Passport-sized photograph

- Business registration proof (if applicable)

- Receive Credentials: Upon successful verification and approval (which can take 24-48 hours), you will receive unique Aeps API credentials like a Merchant ID, Aeps API key, and client Aeps ID/secret.

2. Acquire and Set Up Hardware

- Purchase Biometric Devices: Acquire UIDAI-certified Aeps biometric devices (fingerprint or iris scanners) from an approved manufacturer.

- Install RD Service: Install the manufacturer’s Registered Device (RD) Aeps service software on your smartphone or computer.

- Register Devices: Register the serial number of your Aeps biometric device with Aeps india.

3. Technical Integration and Development

- Obtain Documentation & SDKs: Get detailed Aeps API documentation, SDKs, and code snippets from Aeps india. This documentation outlines Aeps service API endpoints, request/response formats, and authentication mechanisms.

- Develop the Interface: Develop Aeps api with user interface (UI) and front-end components within your existing Aeps application, web portal, or POS system for user interaction.

- Implement Back-end Logic: Code the back-end logic to handle secure Aeps API calls, send transaction requests (e.g., balance inquiry, cash withdrawal), and process responses.

- Integrate Biometric Capture: Integrate Aeps biometric device SDK to securely capture and encrypt customer biometric data (fingerprints or iris scans). Ensure raw biometric data is never stored locally to comply with security standards.

4. Testing and Deployment

- Sandbox Testing: Utilize the Aeps india sandbox or testing environment to rigorously test all transaction types, error handling, and security measures before going live.

- Go Live (Production): After successful testing and validation, switch to the live/production environment using your live Aeps API keys and endpoints.

- Train Users: Train your agents/merchants on using the system effectively and securely.

5. Monitoring and Support

- Monitor Transactions: Continuously monitor the transactions for failures and ensure accurate reconciliation of settlements.

- Provide Customer Support: Establish a system for handling customer complaints and failed transactions.

By following these steps, businesses can integrate AEPS capabilities to offer secure, AEPS Banking Software services like cash withdrawals, balance inquiries, and mini-statements to customers.

AEPS API Charges and Commission Structure

AEPS API setup in India typically costs between ₹12,000 and ₹35,000 for standard Aeps api integrations, while white label Aeps software solutions range from ₹15,000 to over ₹1 Lakh. Retailers earn commissions of ₹2–₹15+ per transaction, with higher amounts offering better returns. Transaction fees for Aeps india are generally ₹0.25–₹10 or 0.5%–1%.

AEPS API Setup & Costs

- One-time Setup/Integration: Generally ₹12,000 – ₹35,000 for standard Aeps API; higher for direct, custom integrations.

- White-Label Solutions: Ranging from ₹15,000 up to ₹1.2 Lakhs+ for full, branded Aeps platforms.

- Biometric Devices: ₹1,500 – ₹3,000 per unit (e.g., Mantra MFS100).

- Maintenance: Potential monthly/yearly, or per-transaction fees of ₹0.25–₹10, to as high as 1%.

Typical Commission Structure (Retailer/Agent)

Commissions are largely dependent on the transaction amount and the Aeps india.

- ₹100 – ₹999: ~₹2 per transaction.

- ₹1,000 – ₹1,499: ~₹3 per transaction.

- ₹1,500 – ₹1,999: ~₹4.5 per transaction.

- ₹2,000 – ₹2,499: ~₹5.5 per transaction.

- ₹2,500 and above: High commission, potentially up to ₹13 or 0.40%–1% of the value.

- Mini Statement/Balance Inquiry: Usually a fixed fee of ~₹3.

Key Considerations

- Daily Limits: NPCI defines daily limits, generally up to ₹10,000 per transaction and ₹50,000 daily.

- Commission Sharing: Often 80:20 or similar structures exist between the corporate BC and the agent.

- Charges on High Volume: Some banks charge up to ₹20 + GST if free limits are exceeded.

AEPS API Cost Structure

AEPS API cost typically include a one-time setup fee of ₹12,000–₹35,000,, and sometimes up to ₹1 lakh+ for comprehensive Aeps solutions, with ongoing transaction fees of 0.5%–1% (or ₹3–₹10 per transaction). White-label Aeps software solutions often range from ₹15,000 to ₹1.2 Lakhs. Recurring costs for Aeps software or maintenance can be extra.

Key Cost Components

- One-time Setup/Integration Fees: Generally range from ₹12,000 to ₹35,000, with specialized or white-label Aeps software solution potentially costing up to ₹1 lakh+.

- Transaction Charges: Fees are typically ₹0.25–₹10 per transaction, or 0.5%–1% of the transaction value.

- Software/Maintenance Fees: Aeps india charge recurring monthly or annual fees for support, smooth Aeps API, and Aeps platform access, often around ₹40,000 annually.

- Failed Transactions: Charges for failed, but attempted, authentication transactions can be around ₹0.50.

- Hardware Costs: Best Aeps Biometric devices, such as scanners, usually cost between ₹1,500 and ₹3,000.

Common Fee Structures

- White-label API: Often priced between ₹15,000 and ₹1.2 Lakhs for Aadhaar Enabled Payment System api setup, sometimes including the Aeps portal, but usually with higher transaction fees.

- Standard API: Higher initial Aeps setup fees (up to ₹4.5 lakh for certain Aeps API types) but typically lower transaction charges.

- Agent Commissions: Retailers and agents often earn between ₹1 and ₹10 per transaction, with higher amounts for larger transactions.

Factors Affecting Cost

- Integration Type: White label Aeps api vs. custom Aeps api integration.

- Aeps india Partnerships: Costs may vary based on the underlying Aeps india.

- Service Level: Standard vs. premium support, which may increase fees.

Aeps Api Documentation provide

AEPS API documentation is specific to the Aeps india and generally includes details on endpoints, parameters, security measures (like biometric data encryption), and Aeps api activation processes.

For specific documentation, you must choose a Aeps india and register with them.

Key Features Covered in Documentation

AEPS API allow integration of the following core banking services using Aadhaar number and biometric authentication:

- Cash Withdrawal: Enables a customer to withdraw cash from their Aadhaar-linked account.

- Balance Inquiry: Allows checking the bank account balance in real time.

- Mini Statement: Provides a list of the last few transactions.

- Cash Deposit: Enables cash deposit functionality.

- Fund Transfer: Facilitates Aadhaar-to-Aadhaar fund transfers.

Integration Requirements

The documentation typically outlines the following general steps and requirements:

- API Key/Credentials: Obtaining necessary authentication keys from the Aeps india.

- Onboarding Process: Aeps API onboarding retailers/merchants and performing their Aeps e-KYC (Know Your Customer) using OTP or biometric verification.

- Biometric Device Integration: Instructions for integrating Aeps biometric devices (fingerprint scanners, iris scanners) as per UIDAI standards.

- Request/Response Format: Details on the required request parameters (e.g., Aadhaar number – sent encrypted, bank IIN/code, amount) and the structure Aeps API response, often in JSON or XML format.

- Security Measures: Information on data encryption (e.g., Aadhaar number encryption) and compliance with regulatory guidelines (RBI/NPCI).

- Sandbox Environment: Access to a testing environment for aeps software development and ensuring seamless integration before going live.

Aeps Api Security, Compliance & RBI/NPCI Guidelines

As of January 1, 2026, the Reserve Bank of India (RBI) and the National Payments Corporation of India (NPCI) have introduced stringent regulations to enhance security in the Aadhaar Enabled Payment System (AePS), following increased fraud risks. These guidelines focus on rigorous KYC for AePS Touchpoint Operators (ATOs), mandatory device standards, and continuous transaction monitoring.

Key RBI/NPCI Guidelines (Effective Jan 1, 2026)

- Mandatory Full KYC: All AePS agents must undergo a complete “full” Know Your Customer (KYC) verification process before onboarding.

- Re-KYC for Inactivity: Agents with no transaction history for three consecutive months are deemed inactive and must complete a fresh Aeps KYC process to resume services.

- “One Operator, One Bank” Rule: To improve accountability and prevent misuse, each AePS operator/agent can only be linked to a single acquiring bank.

- Strict API Control: Authorized AEPS Cash Withdrawal API must be used exclusively for legitimate, authorized AePS operations to prevent misuse.

- Location Constraints: Transaction activity must be consistent with the registered geographical location of the operator.

- Transaction Limits: NPCI maintains a maximum limit of ₹10,000 per transaction, with daily limits often restricted to ₹50,000 to manage risk.

- No Extra Charges: Agents are strictly prohibited from charging additional fees to customers for AePS services.

AePS Security Measures (2026 Guidelines)

To enhance user security, the RBI has mandated several measures for banks and service providers:

- Two-Factor Authentication & Liveness Detection: Enhanced verification, such as liveness detection (to ensure a live person, not a copy), is required to prevent fraud.

- One Operator, One Bank Limit: Each AePS Touchpoint Operator (ATO) is restricted to being onboarded by only one acquiring bank to enhance accountability.

- Mandatory Re-KYC: Agents inactive for 3 consecutive months must undergo a fresh, mandatory Aeps KYC process before resuming services.

- Real-time Monitoring & API Security: Acquiring banks must monitor transactions in real-time for fraud and ensure that APIs are used strictly for AePS functions.

- Biometric Data Protection: In accordance with UIDAI guidelines, sensitive biometric data is never stored on agent devices or Aeps india servers.

- Device Safety: Only UIDAI-certified, STQC-compliant Registered Devices (RD) are allowed to prevent data tampering.

The new rules aim to build greater trust in the digital payment ecosystem, particularly in rural and underbanked areas.

Support and Maintenance by Aeps india

Aeps india offer comprehensive technical support and maintenance, ensuring 24/7 assistance for top Aeps API integration, transaction monitoring, and troubleshooting. Services include ensuring high uptime for cash withdrawals/deposits, managing security compliance, real-time reporting, and agent training. They typically offer support via dedicated support teams to resolve issues promptly.

Key Aspects of Support and Maintenance:

- Technical Assistance: 24/7 support for integrating, testing, and launch AEPS API, ensuring smooth operation.

- Maintenance & Security: Regular updates to the AEPS biometric API to maintain compliance with RBI and NPCI guidelines, including secure data handling.

- Transaction Monitoring: Real-time tracking of transactions (withdrawals, balance inquiries) to immediately resolve failed or pending requests.

- Agent Support: Assistance for retailers, agents, and distributors regarding onboarding, KYC, and, if needed, white label Aeps api solutions.

- Troubleshooting: Quick resolution of technical glitches to minimize downtime and prevent service disruptions.

Aeps India one of the top aeps providers in India often mentioned for strong support.

Aps india – Fast Aeps Api Provider

Aeps india is one of the top fast AEPS API providers in India for 2026, offering high speed Aeps api, secure, and compliant cash withdrawals, balance inquiries, and mini-statements. These Aeps india offer 99% uptime, top Aeps API integrate for instant Aeps api setup, and competitive Aeps commission structures.

Key Features to Look For

- Speed: Real-time transaction processing.

- Reliability: High uptime and low failure rates.

- Security: Biometric authentication and UIDAI compliance.

- Support: 24/7 technical assistance for integration.

Common Use Cases

- Cash Withdrawal: Customers can withdraw money from Aadhaar-linked accounts.

- Balance Inquiry: Real-time bank balance checks.

- Mini Statement: Accessing recent transaction history.

For developers, these b2b Aeps services usually offer well-documented Aeps API, allowing for quick integration into existing Aeps b2b platforms or retail Aeps applications.

How to Choose the Best AEPS API Provider in India

Aeps india is the best AEPS API provider in India requires prioritizing high transaction success rates (98%+98%+), robust security (NPCI compliance), and instant settlement capabilities. Key factors include competitive commissions, 24/7 technical support, a user friendly Aeps app/Aeps admin portal, and AEPS payment API stability to ensure smooth, uninterrupted service for banking transactions.

Here is a comprehensive guide to the Aeps india:

1. Security and Compliance (Most Critical)

- NPCI/RBI Authorized: Ensure the Aeps india is a direct Business Correspondent (BC) or authorized by the National Payments Corporation of India (NPCI).

- Data Security: Aeps india using end-to-end encryption for biometric data (fingerprint/iris) to prevent fraud.

2. Technical Performance and Stability

- High Success Rate: Aeps india offering a 98%+98%+ transaction success rate to avoid failures.

- Low Downtime: The Aadhaar payment API must have high uptime, ensuring service availability during peak hours.

- Speed: Fast transaction processing is essential for a good user experience.

3. Commission and Fee Structure

- Competitive Rates: Best commission structures; Aeps india offer up to ₹10–₹15 per transaction.

- Transparency: Ensure there are no hidden fees or exorbitant, unclear charges.

- Joining Fees: Aeps india offer free Aeps registration or low cost Aeps onboarding for new agents.

4. Settlement and Wallet Management

- Instant/Same-Day Settlement: Aeps india offers instant wallet-to-bank transfers to keep your working capital moving.

- Multiple Payout Options: The ability to transfer funds directly to bank accounts via IMPS/NEFT is crucial.

5. Support and Usability

- 24/7 Technical Support: Access to instant support (phone, WhatsApp, email) is vital to handle failed transactions or API downtime.

- User-Friendly Dashboard: A clean, intuitive Aeps dashboard with detailed reporting helps in tracking daily transactions and earnings.

6. Additional Services (Value Additions)

- Aeps india that offer a comprehensive suite of services beyond AEPS, such as Micro ATM, BBPS (Bill Payments), Recharge, and Money Transfer (DMT).

Why Choose Aeps India as Your AEPS API Solution

Aeps india one of the AEPS API solution (Aadhaar Enabled Payment System) is crucial to ensure secure, fast, and compliant financial transactions, featuring high success rates (99.9% uptime), real-time settlements, and robust Aeps biometric authentication. Aeps india enable businesses to offer essential banking services like cash withdrawals, balance inquiries, and mini-statements, improving financial inclusion and generating revenue through commissions.

Key Reasons to Choose a Professional AEPS API Provider:

- Robust Security & Compliance: Ensures compliance with RBI and NPCI standards, utilizing secure, encrypted, and Aeps biometric-based authentication (fingerprint/iris) to prevent fraud.

- High Transaction Success Rates: Provides reliable, high-performance infrastructure with minimal downtime, ensuring smooth, real-time, and uninterrupted financial services.

- Easy Integration & Support: Offers well-documented, easy-to-secure Aeps API integration for quick deployment into existing Aeps apps, along with 24/7 technical support to resolve issues.

- Increased Revenue & Growth: Enables businesses to earn commissions on transactions, creating new revenue streams, and helps in expanding the customer base to unbanked or rural areas.

- Cost-Effectiveness & Scalability: Aeps india affordable Aeps api, best Aeps api solutions (White Label Aeps Api solution options) suitable for both startups and established businesses, minimizing infrastructure costs.

- Scalability: White label Aeps Api solution are available, allowing businesses to scale from small startups to large enterprises.

- Diverse Service Offerings: Supports multiple banking services through a single Aeps API, including cash withdrawal, mini-statements, and, in some cases, Aadhaar Pay.

Top providers like Aeps India are often chosen for these comprehensive benefits.

Future Trends AEPS API in India

Future trends for Aadhaar Enabled Payment System API (2026+) focus on enhanced security through AI-driven fraud detection, liveness-detection biometrics (face/iris), and blockchain, alongside stricter RBI compliance (re-KYC, operator monitoring). The technology is moving toward cloud-based, mobile-first Aeps api design, deeper UPI integration, and expanded financial services like micro-loans and insurance to drive rural financial inclusion.

Key Future Trends in AePS API Technology

- Advanced Biometrics & Liveness Detection: Moving beyond fingerprints to iris and face scanning, with mandatory “liveness” detection to prevent spoofing.

- AI/ML for Security: Implementation of artificial intelligence for real-time risk assessment, anomaly detection, and personalized financial advice.

- Blockchain Integration: Exploration of distributed ledger technology to ensure immutable and transparent transaction records.

- API-First & Cloud-Based Infrastructure: Increased adoption of cloud-native AEPS transaction settlement API for better scalability, easier integration, and faster transaction processing.

- Mobile-First Design: Enhanced user interfaces designed for mobile devices to improve accessibility for agents and users.

Regulatory and Operational Shifts (2026 Guidelines)

- Tightened Compliance: Stricter KYC requirements for Aadhaar Touchpoint Operators (ATOs) and mandatory re-verification for inactive agents.

- Risk-Based Monitoring: Real-time, transaction-level monitoring of agents by banks to prevent fraudulent activity.

- Enhanced Fraud Management: Integration with advanced Security Information and Event Management (SIEM) and EFRMS for better security.

Expanded Service Offerings

- Embedded Finance: Integration AEPS with micro-loans, insurance, and other fintech products.

- Interoperability with UPI: Deeper integration with UPI and digital wallets to create a unified payment experience.

- Expanding Use Cases: Moving beyond cash withdrawals to include cash deposits, mini-statements, and Aadhaar Pay for merchants.

These trends are driven by the goal to reach 3.5 billion annual transactions by 2026, making rural banking safer and more seamless.

Conclusion

The Aadhaar Enabled Payment System API has become a powerful solution for businesses that want to offer fast, secure, and card-less banking services in India. With AEPS API integration, retailers, CSPs, and fintech companies can provide cash withdrawal, balance enquiry, mini statement, and Aadhaar-to-Aadhaar fund transfer services using simple biometric authentication. This makes AEPS API an important part of India’s growing digital payment ecosystem.

An AePS API (Aadhaar Enabled Payment System Application Programming Interface) is a software bridge developed by the NPCI that enables businesses to integrate secure, biometric-based banking services directly into their Aeps app or websites. It allows customers to perform transactions like cash withdrawals, deposits, balance inquiries, and mini-statements using just their Aadhaar number and fingerprint, turning any retailer into a micro-ATM.

For fintech companies, retailers, and service providers, the AEPS API in India simplifies digital payments while ensuring high security and regulatory compliance. It reduces dependency on cards and ATMs, improves financial inclusion, and allows businesses to reach customers even in remote areas.

For businesses, Aeps india is the right AEPS API provider in India is essential to ensure high transaction success rate, RBI and NPCI compliance, strong security, and real-time settlements. A reliable b2b Aeps API helps reduce failures, improve customer trust, and increase daily transaction volume and commission income.

If you are looking for a scalable and reliable AEPS API solutions, choosing the Aeps india is key to success. A well-integrated AEPS API helps businesses deliver smooth transactions, better user experience, and trusted digital banking services, making it an essential part of India’s growing digital payment ecosystem.

Aeps India offers a secure, easy-to-integrate Aeps api, and scalable Aadhaar Enabled Payment System API designed for long-term business growth. With strong technical support, smooth Aeps onboarding, and future-ready technology, Aeps India helps businesses stay ahead of competitors while delivering trusted Aadhaar-based banking services across India.

Aeps india is the top AEPS API provider in India is key to growth. A reliable Aeps platform like AEPS India supports scalability, compliance, and consistent earnings, making it the ideal choice for businesses looking to expand their digital payment offerings and stay ahead in India’s growing fintech market.

If you want to integrate AEPS API for your business in India, contact Aeps india today to get fast, secure, and fully compliant AEPS solution that enhance customer experience and simplify digital banking.

FAQ: Aadhaar Enabled Payment System (AEPS) API Explained

The AEPS API is a digital payment interface that allows businesses to provide Aadhaar-based banking services. Using this API, users can perform cash withdrawal, cash deposit, balance enquiry, and fund transfer through biometric authentication without using a debit card or ATM.

The AEPS API in India works by verifying a customer’s Aadhaar number, bank name, and fingerprint. Once authenticated, the transaction is processed securely through the banking network, making payments fast and reliable.

The AEPS API can be used by fintech companies, retailers, distributors, CSPs, NBFCs, and digital payment platforms. It helps businesses offer cardless and secure banking services to customers across urban and rural India.

The Aadhaar Enabled Payment System API supports:

Cash withdrawal

Cash deposit

Balance enquiry

Aadhaar-based fund transfer

These services help businesses provide complete digital banking solutions.

Using an AEPS API provides secure, fast, and reliable banking services. It enables digital financial inclusion, reduces the need for physical bank visits, allows real-time Aadhaar-based transactions, and helps businesses expand their payment services efficiently.

To integrating AEPS API, you need to register with a Aeps india, get Aeps API credentials, and follow their integration guide. Once set up Aeps platform can start processing Aadhaar-based transactions instantly, with full compliance to NPCI and RBI guidelines.

Yes, the AEPS API is highly secure. It uses biometric authentication and follows strict banking and regulatory guidelines, ensuring safe transactions and protection against fraud.

Integrating AEPS API allows businesses to expand their services, increase customer trust, and support financial inclusion. It also helps reach customers in areas where ATM or card usage is limited.

Aeps india the best AEPS API provider company in india look for high uptime, fast transaction processing, easy integration, strong technical support, and full compliance with Indian regulations.

Businesses earn commission per transaction. Higher transaction volume means higher daily income, making AEPS API a profitable digital banking solution.

Basic business KYC documents, Aadhaar, PAN, and bank account details are required to activate AEPS API services.

Aeps India is an Aeps api provider offers a reliable, secure, and easy-to-integrate AEPS API solution with high success rate, real-time settlements, and full technical support.

Yes, transaction limits depend on bank and NPCI rules, but Aeps India supports high-volume transactions suitable for growing businesses.

Earnings depend on transaction volume and commission structure. AEPS API offers daily income opportunities for retailers and service providers.

Yes, AEPS API is ideal for rural and semi-urban areas, where customers can access basic banking services without visiting a bank branch.

Customers enter their Aadhaar number, select their bank, and verify with fingerprint. The amount is processed instantly through the best AEPS cash withdrawal API.

Yes, AEPS API integration is simple and works smoothly with websites, Aeps android apps, and business Aeps b2b software.

Yes, the best Aadhaar Enabled Payment System API follows all required guidelines and security standards in India.

Yes. AEPS API is highly secure, fully regulated by NPCI and RBI, and ensures biometric authentication for every transaction. Businesses can trust it to provide safe, fraud-free financial services to their customers.

AEPS API: Complete Guide to Integration, Features & Benefits (2026)

Best Aadhaar Pay API in india : Complete Guide