AEPS Onboarding: Complete Step-by-Step Guide for New Businesses

Starting an AEPS business in India is one of the fastest ways for retailers, fintech startups, and entrepreneurs to enter the digital payment ecosystem. AEPS (Aadhaar Enabled Payment System) allows businesses to provide essential banking services such as cash withdrawal, balance enquiry, mini statements, and Aadhaar-based fund transfers to customers, even in remote and rural areas. With the growing need for financial inclusion and digital banking, many new businesses are actively searching for a complete AEPS onboarding guide to start their services quickly and securely.

AEPS (Aadhaar Enabled Payment System) Onboarding is the registration process for merchants or agents to become authorized banking correspondents, enabling them to offer services like cash withdrawals and balance inquiries using customer Aadhaar-based biometric authentication. It involves KYC, biometric device setup, and partnership with Aeps india.

AEPS Onboarding refers to the registration process for agents (merchants/retailers) to start providing banking services like cash withdrawal, balance inquiry, and mini-statements using the Aadhaar Enabled Payment System (AePS). It involves Aeps e-KYC via biometric authentication, linking an Aadhaar-enabled bank account, and integrating Aeps biometric scanner to become an authorized Banking Correspondent (BC).

For startups, retail shop owners, CSC operators, and fintech companies, understanding the complete AEPS registration process, required documents, eligibility criteria, and integration steps is essential for building a successful digital payment business. Proper AEPS onboarding not only ensures smooth transaction processing but also helps businesses earn steady commissions while expanding their customer base.

AEPS India onboarding helps new businesses connect with trusted banking networks and digital payment infrastructure without requiring a large investment. By partnering with a reliable AEPS service provider like Aeps india, businesses can quickly set up AEPS software, micro ATM services, and secure payment solutions to serve customers efficiently. The biggest advantage of starting AEPS business is that it supports financial inclusion, allowing people in remote locations to access Aeps banking services without visiting a bank branch.

AEPS India are designed to make banking services easy, fast, and secure using Aadhaar authentication. With the help of advanced AEPS API integrate and best AEPS software, new businesses can quickly start their digital payment services with low investment and high growth potential. Choosing a reliable technology partner like AEPS India helps businesses get secure platforms, smooth onboarding support, and long-term technical assistance.

This guide is designed to help new businesses understand step-by-step AEPS onboarding, including eligibility criteria, required documents, software setup, and technical integration. Whether you are a retail shop owner, CSC operator, or fintech entrepreneur, following this process will allow you to start a profitable and scalable AEPS business while supporting India’s mission for financial inclusion and digital banking growth.

What is AEPS Onboarding

AEPS (Aadhaar Enabled Payment System) Onboarding is the registration process for agents (Business Correspondents) to activate biometric-based banking services such as cash withdrawals and balance inquiries using Aadhaar authentication. It involves e-KYC, PAN card verification, and linking a bank account to authorized Aeps india provide platforms.

AEPS Onboarding Mean

AEPS Onboarding (Aadhaar Enabled Payment System) is the registration process for agents or merchants (like kirana stores) to become authorized banking correspondents, enabling them to offer services such as cash withdrawals, deposits, and balance inquiries to customers using biometric authentication. It involves KYC, connecting to a bank/fintech, and activating Aeps biometric device for secure transactions.

AEPS Onboarding Work

AEPS (Aadhaar Enabled Payment System) onboarding is the mandatory registration process for agents or retailers to become authorized Business Correspondents (BCs) to offer banking services cash withdrawal, deposits, and balance inquiries using Aadhaar-based biometric authentication. It involves Aeps KYC verification, linking a bank account, and setting up a certified Aeps biometric device (fingerprint/iris scanner).

Key Aspects of AEPS Onboarding Work:

- Registration: Agents must register with an NPCI-authorized AEPS service provider, such as Aeps India.

- Documentation (KYC): Mandatory documents include Aadhaar Card, PAN Card, bank account details (cancelled cheque/passbook), and a photograph.

- Hardware Setup: A compatible Aeps biometric device (e.g., Mantra) must be connected to a smartphone or desktop.

- Technical Integration: Aeps india sets up the agent with necessary credentials, including a Merchant ID, and activate Aeps API or Aeps app for transactions.

- Verification: A quick Aeps video KYC or digital Aeps KYC is completed, usually allowing for 24-48 hour approval.

Who Can Apply for AEPS Onboarding

Any Indian citizen aged 18 or older with a valid Aadhaar card, PAN card, and an Aadhaar-linked bank account can apply for AePS (Aadhaar Enabled Payment System) onboarding. It is primarily designed for retail shop owners, Kirana store owners, CSPs (Customer Service Points), and entrepreneurs looking to provide banking services.

Key Requirements for AePS Onboarding:

- Documentation: PAN card, Aadhaar card, and an active bank account.

- Hardware: A STQC/Aadhaar-certified biometric device (fingerprint or iris scanner) is mandatory.

- Setup: A physical shop or office space (owned or rented) is generally required.

- Technology: A smartphone or PC with internet access.

- Registration: Mandatory registration with an authorized Aeps india, which includes Aeps KYC verification.

Who Should Apply:

- Retailers & Shopkeepers: Small business owners (Kirana stores, mobile shops, general stores).

- CSP/Business Correspondents: Individuals operating kiosks or acting as banking correspondents.

- Entrepreneurs: Individuals looking to start a financial services business.

Applicants need basic computer/smartphone knowledge and, for some, at least a 12th-standard education is preferred.

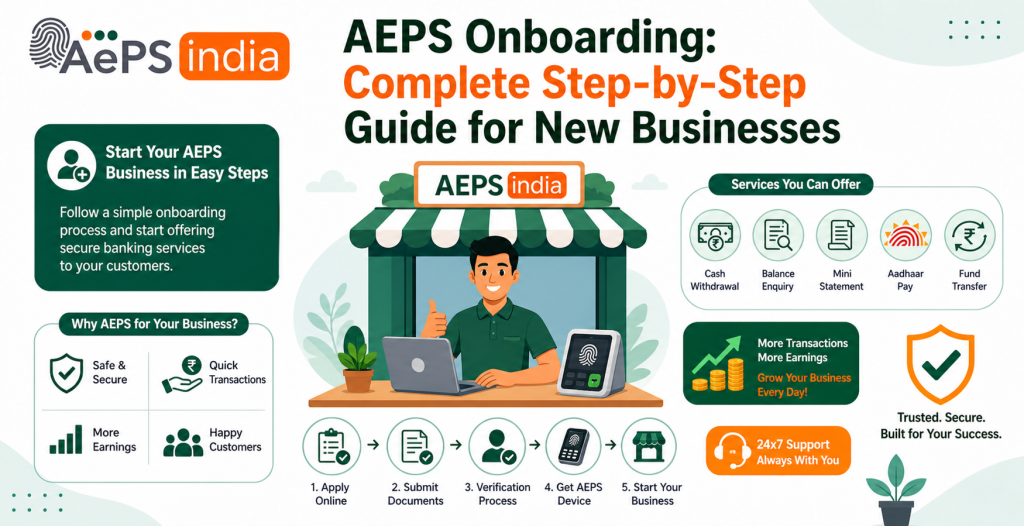

Types of AEPS Services You Can Offer to Customers

As an Aeps india offer a variety of essential banking and financial services directly from your shop or mobile device, eliminating the need for customers to visit a bank branch. These services are powered by the National Payments Corporation of India (NPCI) and use Aeps biometric authentication for security.

Here are the key types of AEPS services you can offer to customers:

1. Core AEPS Banking Services

- Cash Withdrawal: Customers can withdraw money from their Aadhaar-linked bank account using their fingerprint or iris scan. This is particularly useful for rural areas with limited ATM access.

- Balance Enquiry: Customers can instantly check the available balance in their Aadhaar-linked bank account.

- Mini Statement: Aeps india provide a,mini-statement showing the last few transactions of the customer’s account.

- Cash Deposit: Customers can deposit cash into their Aadhaar-linked bank account.

- Aadhaar to Aadhaar Fund Transfer: You can facilitate money transfers from one Aadhaar-linked account to another.

2. Merchant and Retail Services

- BHIM Aadhaar Pay: This allows merchants to accept payments from customers directly from their bank accounts using biometric authentication, without needing a POS machine or card.

- Micro ATM Services: Using a small, Aeps portable device, you can act as a mini-bank, offering cash deposit and withdrawal services.

3. Government and Informational Services

- Direct Benefit Transfer (DBT) Services: You can assist customers in receiving government subsidies, pensions, and NREGA wages directly into their accounts.

- Aadhaar Seeding Status: You can help customers check if their bank account is linked (seeded) with their Aadhaar card.

- eKYC: You can perform electronic Know Your Customer (eKYC) services for customers.

4. Additional Value-Added Services

Aeps india allow you to bundle other services with AEPS, such as:

- Domestic Money Transfer (DMT): Transfer money to any bank account.

- Utility Bill Payments: Payment of electricity, gas, and water bills.

- Recharges: Mobile and DTH recharges.

- PAN Card Application: Assisting with PAN card services.

Key Benefits of Offering These Services

- Commission-Based Income: You earn a commission on each successful transaction (e.g., ₹5–₹15+ for withdrawals).

- Increased Footfall: Providing banking services brings more customers to your store.

- Low Investment: Requires only a smartphone/computer, a,Aeps biometric device (scanner), and internet connectivity.

- 24/7 Availability: Services are accessible round-the-clock.

Requirements to Offer Services: You will need to partner with an Aeps india to get an Aeps Agent ID and Aeps device.

Key Aspects of AEPS Onboarding

Key aspects of onboarding for the Aadhaar Enabled Payment System (AEPS) specifically for agents, retailers, or Business Correspondents (BC) revolve around regulatory compliance, technical Aeps setup, and secure authentication to enable cardless banking services. As of January 1, 2026, the RBI has mandated stricter, full Aeps KYC for all AEPS Touchpoint Operators (ATOs) to prevent fraud.

Here are the key aspects of AEPS onboarding:

1. Mandatory Documentation and KYC

- Essential Documents: Agents must submit a valid Aadhaar card, PAN card, and bank account details (cancelled cheque or passbook).

- Aadhaar-Linked Bank Account: The agent’s bank account used for settlement must be linked to their Aadhaar number.

- Verification Process: Aeps Onboarding requires a rigorous Know Your Customer (KYC) process, which may include video or in-person verification by the Aeps india.

- Re-KYC Rule: If an agent remains inactive for three consecutive months, they must undergo a fresh KYC process before resuming services.

2. Technical and Hardware Requirements

- Certified Biometric Device: A UIDAI/STQC-certified fingerprint or iris scanner is mandatory.

- Registered Device (RD) Service: The biometric device must use RD services to securely encrypt data at the source, preventing the use of spoofed or fake fingerprints.

- Infrastructure: A smartphone (Android) or desktop/laptop with a stable internet connection is required to run the AEPS application.

3. Regulatory Compliance and Security (2026 Rules)

New regulations for AEPS include linking each operator to a single acquiring bank for enhanced accountability. NPCI has established transaction limits to mitigate risk. Agents are required to provide receipts for every transaction and are strictly prohibited from storing customer Aadhaar or biometric data.

4. Selection of Service Provider

Agents must register through an NPCI-approved Aeps india is an AEPS provider. These Aeps india typically offer support and aim to activate Aeps agent ID within 24–48 hours.

5. Operational Setup

Operational requirements generally include having a physical business location and sufficient working capital for cash withdrawals. Agents earn commissions based on transaction value.

6. Post-Onboarding Best Practices

Banks monitor agent activity for suspicious transactions. Aeps Biometric devices are required to have liveness detection to prevent fraudulent activity.

Note: For customers, using AEPS only requires an Aadhaar-linked bank account and does not necessitate separate registration.

Complete Eligibility Criteria for AEPS Onboarding

AEPS onboarding requires Indian residents, aged 18+, to possess a valid PAN card, Aadhaar card, and an Aadhaar-linked bank account. As of 2026, agents must complete “full KYC,” use a UIDAI-certified Aeps biometric device (fingerprint/iris scanner), and operate through a smartphone or PC. A shop or business place is generally required.

Core Eligibility Criteria & Requirements:

- Age & Residency: Minimum 18 years old and an Indian citizen.

Documentation (KYC):

- Aadhaar Card: Must be linked to the bank account for authentication.

- PAN Card: Mandatory for financial transactions.

- Bank Account: An active bank account (Savings or Current) for settlement.

- Photograph: Recent passport-sized photograph.

Technical Requirements:

- Biometric Device: UIDAI-certified Aeps fingerprint or iris scanner (e.g., Mantra).

- Device: Android Smartphone, Laptop, or PC.

- Internet: Stable internet connection.

Operational Requirements:

- Business Setup: A physical shop or kiosk is usually necessary for retail services.

- Registration: Enrollment with a Aeps india is an authorized Aeps API provider.

- Re-KYC: Agents inactive for 3 consecutive months must complete a fresh Aeps KYC.

- One Operator Policy: Under 2026 regulations, agents may be restricted to one acquiring bank.

Important Notes:

- The 2026 guidelines mandate that banks perform thorough background checks before onboarding to ensure compliance with RBI security norms.

- Basic computer knowledge is required to operate the AEPS portal.

Documents Required for AEPS Onboarding Process

AEPS (Aadhaar Enabled Payment System) onboarding requires key Aeps KYC documents for agent registration, primarily a valid Aadhaar card (linked to a bank account), PAN card, and bank account details (passbook/cancelled cheque). Additional requirements include a passport-sized photograph, active mobile number linked to Aadhaar, email ID, and a UIDAI-certified Aeps biometric scanner (fingerprint/iris).

Mandatory Documents for AEPS Onboarding

- Aadhaar Card: Must be active and linked to the bank account for authentication.

- PAN Card: Required for identity verification and business compliance.

- Bank Account Details: A cancelled cheque, passbook, or bank statement for settlement.

- Passport-sized Photograph: Recent photo.

- Proof of Address/Business: Utility bill, shop rental agreement, or trade license (often required for physical verification).

- Active Mobile Number: Preferably linked with the Aadhaar card for OTPs.

- Email Address: For registration and communication.

Hardware & Additional Requirements

- Biometric Device: A UIDAI-certified (STQC) fingerprint or iris scanner (e.g., Mantra).

- Smartphone/Computer: Android phone or computer to access the agent Aeps portal or best Aeps app.

- Shop/Business Address Proof: Utility bill, rent agreement, or trade license may be required.

- Minimum Age: Applicant must be 18 years or older.

Additional Requirements:

- Business Entity Documents: For firms, GST registration or incorporation documents may be needed.

- Age Requirement: Applicant must be over 18 years old.

- Technical Setup: A smartphone, laptop, or desktop computer with internet access.

It is important to ensure that the Aadhaar card is properly linked to the bank account and that the Aeps biometrics are active to avoid onboarding failures.

Who Can Start AEPS Business in India?

Any Indian citizen aged 18 or older with a valid Aadhaar card, PAN card, and a bank account can start an AEPS (Aadhaar Enabled Payment System) business. Ideal for shopkeepers, CSC centers, or individuals, this low-investment venture requires a smartphone/PC, a biometric device (fingerprint/iris scanner), and registration with an authorized Aeps india.

Key Requirements to Start AEPS Business:

- Documentation: Aadhaar card, PAN card, and a bank account linked to your Aadhaar.

- Equipment: A smartphone, tablet, or PC with internet connectivity and a certified Aeps biometric device (RD Service).

- Location: A physical shop (Kirana store, medical store, recharge shop) is preferred, though it can be operated from home.

- Registration: Aeps india to get access to the NPCI system.

Who is Best Suited?

- Small shop owners (Kirana stores) looking to earn extra income.

- CSC (Common Service Center) operators.

- Unemployed individuals looking for self-employment opportunities.

- Banking agents/Business Correspondents (BCs).

Why AEPS Onboarding is Important for New Businesses and Retailers

AEPS onboarding is essential for new businesses and retailers because it transforms ordinary shops into local banking hubs (mini-banks), allowing them to provide essential services like cash withdrawals, balance inquiries, and money transfers. This, in turn, boosts revenue, increases customer footfall, and enhances security by reducing the reliance on physical cash.

Here is why AEPS onboarding is crucial for new businesses and retailers:

1. Increased Revenue through Commissions

- Steady Income Stream: Retailers earn commission on every AEPS transaction (e.g., cash withdrawals, balance checks).

- High-Volume Earnings: According to 2026 projections, active agents can generate significant monthly income (ranging from ₹15,000 to ₹25,000 or more in high-volume areas).

- Tiered Commission Structure: Larger cash withdrawal amounts often lead to higher commissions, providing better returns for the retailer.

2. Higher Customer Footfall

- Turning Retailers into “Mini-Banks”: By offering services like cash withdrawals (especially valuable in areas with few ATMs), retailers attract more customers, particularly in rural or underserved areas.

- Cross-Selling Opportunities: Increased foot traffic means more customers are likely to purchase other products or services in the shop.

3. Low Investment, High ROI

- Simple Setup: New businesses can start offering AEPS service with minimal investment, usually requiring only a smartphone/PC, an internet connection, and a UIDAI-certified biometric device.

- Immediate Activation: Aeps india offer fast digital Aeps onboarding (e-KYC), allowing retailers to start providing services in 24–48 hours.

4. Enhanced Security and Reduced Cash Risk

- Biometric Authentication: Transactions are authorized using fingerprint or iris scans, which are much harder to fake than traditional PIN-based methods, reducing fraud risks.

- Less Physical Cash Handling: Retailers can easily deposit cash into their own accounts, reducing the risk of holding large amounts of physical cash on site.

5. Competitive Advantage and Customer Loyalty

- Increased Trust: Providing a secure, government-backed (NPCI) service makes the business more trusted in the local community.

- One-Stop Solution: Retailers can offer a comprehensive range of services including AEPS, utility bill payments, and recharges which strengthens customer loyalty and makes them a one-stop-shop.

6. Regulatory Compliance

- Mandatory Standards: As of Jan 1, 2026, the RBI mandates strict KYC for all AEPS Touchpoint Operators (ATOs). Proper onboarding ensures compliance, avoiding penalties or deactivation.

By embracing AEPS, new businesses can bridge the financial inclusion gap in their locality while building a profitable and sustainable business model.

Benefits AEPS Onboarding

AEPS onboarding provides secure, paperless, and cardless banking services, allowing users to perform transactions like cash withdrawals, deposits, and balance inquiries using only Aadhaar authentication. It promotes financial inclusion in rural areas, offers 24/7 accessibility, and allows merchants to generate extra income via commissions.

Key Benefits of AEPS Onboarding:

For Users (Customers):

- Financial Inclusion: Access to banking in remote areas, bringing services to the doorstep.

- Convenience & Simplicity: No debit cards, PINs, or smartphones needed; only Aadhaar number and biometrics (fingerprint/iris) are required.

- Security: High-security, biometric-based, reducing fraud and phishing risks.

- Direct Benefit Transfer (DBT): Easy receipt of government subsidies and pensions.

- Interoperability: Customers can use any bank’s service at any AEPS-enabled merchant point.

For Merchants/Agents (Onboarding Partners):

- New Revenue Stream: Earn commissions on every transaction (withdrawals, balance inquiries).

- Increased Footfall: Attracts more customers to retail shops.

- Low Investment: Requires only a smartphone/computer and a certified biometric device.

- Instant Settlement: Fast, secure, and often 24/7 settlement of funds.

- Service Diversification: Enables bundling of other services like bill payments (BBPS) and money transfers.

For Banks & Financial Institutions:

- Reduced Costs: Lowers costs associated with operating physical branches and ATM maintenance.

- Reach & Penetration: Extends services to rural, unbanked populations.

- Faster Digital KYC: Streamlines user verification.

General Advantages:

- Digital & Paperless: Speeds up the Aeps onboarding process and supports environmentally friendly, cashless operations.

- Government Benefit Disbursement: Facilitates direct transfers of subsidies, pensions, and MGNREGA funds.

- Future-Ready: Incorporates advanced technology like face authentication and AI for improved security.

Features AEPS Onboarding

(AEPS) Aadhaar Enabled Payment System onboarding enables retail shop owners, business correspondents (BCs), and agents to quickly and securely begin offering banking services to customers. The process leverages Aadhaar-based authentication to turn local, small businesses into “mini-banks”.

Key features of AEPS onboarding for agents and businesses include:

- Fast, Paperless Digital Registration: Onboarding is a predominantly digital, paperless process that can be completed within 24 to 48 hours.

- Minimal Documentation: Required documents are limited to basic, officially valid documents: PAN Card, Aadhaar Card, bank account details (for commission settlement), and a passport-sized photograph.

- Instant Activation & eKYC: Aeps india offer instant activation, allowing agents to begin transactions almost immediately after digital or Aeps video KYC verification.

- Biometric Device Integration: Aeps Onboarding involves registering a UIDAI-certified, STQC-compliant biometric device (fingerprint or iris scanner) to ensure secure, encrypted authentication.

- “One Operator, One Bank” Rule: To enhance security and comply with 2026 regulations, agents are now linked to only one acquiring bank to prevent misuse.

- Mandatory Re-KYC for Inactive Agents: If an agent is inactive for three consecutive months, they must undergo a fresh KYC process to resume service.

- Training & Support: Aeps india often offer training on operating the top AEPS app or best Aeps portal, handling transactions (cash withdrawal, balance inquiry), and ensuring compliance.

- Low Setup Investment: It requires minimal infrastructure usually just a smartphone or computer, a stable internet connection, and a compatible Aeps biometric scanner.

Agent Benefits Post-Onboarding:

- Commission Earnings: Agents earn commissions on every transaction, often ranging from ₹2 to ₹15+ per withdrawal.

- Increased Footfall: Offering banking services increases customer traffic to the retail shop.

- High-Value Transactions: Access to “Aadhaar Pay” for transactions exceeding the standard ₹10,000 limit.

Steps to AEPS Onboarding Process

AEPS onboarding involves registering with an NPCI-certified Aeps india, completing digital or physical KYC, and setting up a biometric device. Key steps include submitting Aadhaar, PAN, and bank details, followed by verification, Aeps agent ID generation, and app installation to start secure, biometric-based transactions.

Steps to AEPS Onboarding Process:

- Select an AEPS Service Provider: Choose a reputable, government-approved Aeps India that provides technical support and Aeps API integration.

- Submit Registration Details: Fill out the agent registration form on the Aeps india provide Aeps portal or app, providing personal details like name, email, address, and mobile number.

- Complete KYC Verification: Upload mandatory KYC documents, including your Aadhaar card, PAN card, and bank account details (account number and IFSC code).

- Verify Identity via Biometrics: Complete the Aeps KYC process, which may include a video KYC or a physical verification check at a partner store.

- Purchase & Register Biometric Device: Acquire a UIDAI-certified Aeps fingerprint scanner or iris device, then register it with the Aeps india to ensure secure, encrypted authentication.

- Approval & Activation: Once documents are verified by the NPCI or partner bank, your AEPS agent account is activated.

- Training & Start Operations: Complete the required training on the best Aeps application, receive your unique Aeps Agent ID, and begin offering services like cash withdrawal and balance inquiries.

Key Requirements:

- Aadhaar-Bank Linkage: Ensure the customer’s Aadhaar is linked to their bank account.

- Active Biometrics: The agent must have a working biometric device.

- Compliance: Adhere to all NPCI, RBI, and KYC guidelines to avoid penalties.

AEPS Onboarding Charges, Cost, and Investment Details

AEPS (Aadhaar Enabled Payment System) onboarding involves minimal, often free registration for agents, with total setup investments (device + initial working capital) ranging from ₹1,500 to over ₹30,000 depending on whether a basic retailer or a, white label Aeps service is chosen. Agents can earn between ₹2 and ₹15+ per transaction.

Here is the detailed breakdown of AEPS onboarding charges, costs, and investment details as of February 2026:

1. AEPS Onboarding Charges & Registration Costs

- Retailer/Agent ID (Basic): Often free to ₹499.

- Premium/White Label Registration: Ranging from ₹499 to over ₹1,250 for advanced Aeps portals.

- Documentation Required: PAN Card, Aadhaar Card, bank details (for settlements), and address proof.

- Onboarding Process: 100% online with eKYC via OTP or biometric authentication.

2. Investment Details (Hardware & Infrastructure)

- Biometric Device: Mandatory, certified fingerprint scanner (e.g., Mantra MFS100, Morpho) costs ₹1,500 – ₹3,000.

- Optional Micro ATM: For card-based transactions, costs ₹10,000 – ₹15,000+.

- Initial Working Capital: ₹10,000 – ₹20,000+ is recommended for cash liquidity to handle customer withdrawals.

- Device Requirement: Smartphone or desktop with internet connectivity.

3. Business Models & Setup Costs

- Retailer/Agent: Low investment (Device cost + Working Capital).

- Distributor/Master Distributor: Higher investment (₹15,000 – ₹1.2 Lakhs+ for white label Aeps api/Aeps API) to manage a network of agents.

- API Integration: For fintechs, Aeps API setup costs typically range from ₹12,000 to ₹35,000.

4. Revenue Model (Commission Structure)

Agents earn commission per successful transaction, with higher amounts yielding better returns:

- ₹100 – ₹999: ~₹2 per transaction

- ₹1,000 – ₹1,499: ~₹3 per transaction

- ₹1,500 – ₹1,999: ~₹4.5 per transaction

- ₹2,000 – ₹2,499: ~₹5.5 per transaction

- ₹3,000 & Above: Up to ₹13 or more per transaction

- Balance Enquiry/Mini Statement: ₹1 – ₹5 per transaction

5. Other Important Considerations

- Transaction Limits: Maximum of ₹10,000 per transaction, and generally up to ₹50,000 daily per user.

- Settlement: Many Aeps india offer instant wallet-to-bank transfers, while some may take T+1 day.

- Maintenance Fees: Possible annual/monthly maintenance fees (AMC) for white-label Aeps software, often around ₹40,000 annually.

AEPS Onboarding Commission Structure

AEPS (Aadhaar Enabled Payment System) onboarding involves registering as a Business Correspondent (BC) or agent to facilitate Aeps banking software services, with Aeps commission structures designed to incentivize high volume Aeps transactions. As of 2026, agents can expect to earn between ₹2 and ₹15+ per cash withdrawal, with higher commissions (up to ₹25-₹30 in some cases) for transactions of ₹3,000 and above.

Typical AEPS Commission Structure (2026)

Commissions are tiered based on the transaction amount. Higher withdrawal amounts yield higher returns.

| Transaction Amount (INR) | Typical Commission (Approx. per Transaction) |

|---|---|

| ₹100 – ₹999 | ₹1.00 – ₹2.50 |

| ₹1,000 – ₹1,499 | ₹2.00 – ₹4.00 |

| ₹1,500 – ₹1,999 | ₹3.00 – ₹5.50 |

| ₹2,000 – ₹2,499 | ₹4.00 – ₹7.00 |

| ₹2,500 – ₹2,999 | ₹5.00 – ₹8.00 |

| ₹3,000 – ₹3,999 | ₹7.00 – ₹13.00+ |

| ₹4,000 – ₹7,999 | ₹9.00 – ₹16.00+ |

| ₹8,000 – ₹10,000 | ₹10.00 – ₹15.00+ |

Other Revenue Streams & Service Types

- Balance Inquiry: ₹1 – ₹5 per inquiry

- Mini Statement: ₹2 – ₹7 per statement

- Aadhaar Pay: Often 1% or a set fee per transaction (up to ₹50k limit)

- Monthly Incentives: Aeps india offer bonuses for meeting monthly transaction targets (e.g., ₹2,000 monthly bonus).

Onboarding and Setup Costs

- Registration/KYC Fees: Basic Aeps agent registration is low, often ranging from free to ₹1,250.

- Hardware Costs: A certified Aeps biometric fingerprint scanner (e.g., Mantra, Morpho) costs approximately ₹1,500 – ₹3,000.

- API/White Label Setup: Aeps india provide Aeps API integration costs range from ₹12,000 to ₹35,000, while full white label Aeps solutions can cost between ₹15,000 and ₹1.2 Lakhs+.

Key Factors in Commission Structure

- Tiered Model: Higher transaction Aeps volumes often result in higher Aeps commission slabs.

- Provider Incentives: AEPS India offer monthly incentives of ₹2,000+ for meeting specific transaction targets.

- Settlement: Aeps Commissions are typically credited to the agent’s wallet immediately or daily.

Tips to Grow Your AEPS Business Successfully

To grow AEPS business successfully, focus on building customer trust through reliable, secure, and fast transactions, while diversifying services to include bill payments and mobile recharges. Increase visibility via local marketing, maintain high quality Aeps biometric devices, and ensure excellent customer service to foster repeat business and word-of-mouth referrals.

Key Strategies for AePS Business Growth

- Choose the Right Partner: Aeps india one of the india best AePS service provider company in india offering 24/7 support, high success rates, and fast Aeps API integration.

- Onboarding & Compliance: Complete the Aeps e-KYC process, ensuring you have a valid PAN card and Aadhaar-linked bank account. Strictly follow RBI and NPCI guidelines on transaction limits and security to avoid penalties.

- Technical Training: Train staff to handle Aeps biometric devices (fingerprint/iris) properly to minimize transaction failures and improve speed.

- Local Marketing: Promote your services via posters and hoardings. Word-of-mouth in local communities is highly effective for building trust.

- Customer Education: Explain the security benefits of Aadhaar-based payments to hesitant customers, particularly in rural areas.

- Diversify Services: Increase revenue by offering complementary services like mobile recharges, bill payments, and money transfers.

- Cash Management: Maintain sufficient cash in your bank account/counter to handle high-volume withdrawal requests.

- Maintain Equipment: Regularly calibrate and maintain Aeps biometric devices to ensure high transaction success rates and minimize errors.

- Offer Incentives: Provide small discounts or incentives to encourage repeat customers.

- Secure Transactions: Adhere strictly to RBI and NPCI guidelines for security, ensuring safe, compliant, and verified transactions to prevent fraud.

- Strategic Location: Position your outlet in areas with limited access to traditional banking, such as rural, semi-urban, or underbanked areas.

By focusing on reliability, compliance, and active marketing, you can build a sustainable, high volume AePS business.

Aeps Api Integration for Aeps Onboarding

AePS Aadhaar Enabled Payment System API integration for onboarding involves partnering with an NPCI-approved Aeps india, completing Aeps KYC, and implementing Aeps api integration to enable secure biometric transactions (withdrawal, balance check, mini-statement). Key steps include Aeps india selection, Aeps agent KYC, RD service setup for biometric devices, and Aeps API integrate using documentation.

1. Partner Onboarding & KYC

- Select Provider: Choose a licensed Aeps india.

- Submit Documents: Complete Aeps KYC for the business/retailer, including Aadhaar card (linked to mobile), PAN card, bank account details, and photos.

- Sign Agreement: Finalize the agreement with the Aeps india regarding terms, commission, and fees.

2. Technical Integration (API & SDK)

- Obtain Documentation: Acquire the Aeps API documentation, SDKs, and Aeps API keys from the Aeps india.

- Configure API: Integrate Aeps API for agent Aeps onboarding, transaction management, and transaction status inquiries.

- Setup Callback URL: Configure a secure HTTPS POST URL to receive transaction updates and confirmations from the Aeps india.

- Biometric Integration: Install and integrate the Registered Device (RD) service for UIDAI-compliant biometric devices (fingerprint/iris scanners).

3. Testing & Go-Live

- Sandbox Testing: Test all transaction types, error handling, and security measures in the Aeps india sandbox environment.

- Production Activation: Once testing passes, the Aeps india will move the system to the production environment.

- Activation: Activate Aeps agent account to start live transactions.

4. Key Requirements

- Hardware: UIDAI-certified biometric devices (e.g., Mantra).

- Security: Ensure HTTPS compliance, data encryption for biometric data, and proper error handling for failed transactions.

- IP Whitelisting: White-list your server IP with the Aeps india, and ensure necessary ports (e.g., 25002, 25004) are open for best Aeps API communication.

AEPS Onboarding Security Guidelines and RBI Compliance Requirements

Effective January 1, 2026, the RBI mandates strict AePS onboarding and security protocols to curb fraud, focusing on Full KYC for all operators, mandatory “One-Agent-One-Bank” linking, and 3-month inactivity re-KYC. Key requirements include using Registered Devices (RD) for Aeps biometric authentication, real-time risk-based transaction monitoring by acquiring banks, and prohibition of storing sensitive biometric data on agent devices.

Key Onboarding and Compliance Requirements

- Full KYC for Operators: All AePS Touchpoint Operators (ATOs) must undergo complete, rigorous Aeps KYC verification before onboarding.

- One Operator-One Bank Rule: To enhance accountability, an operator can only be onboarded by a single acquiring bank.

- Active Monitoring: Banks must perform continuous, risk-based monitoring of agent activity, including transaction volume and geolocation, to detect anomalies.

- Re-KYC for Inactivity: Agents with no transactions for three consecutive months must undergo a fresh KYC process before resuming services.

- Documentation: Mandatory submission of Aadhaar, PAN card, and bank account details linked to a mobile number.

Security Guidelines for Transactions

- Registered Device (RD) Services: Only UIDAI-certified, STQC-compliant Aeps devices are allowed to prevent biometric data spoofing.

- Liveness Detection: Enhanced biometric checks are required to ensure the user is present (preventing silicone thumb impressions).

- Two-Factor Authentication: Required for enhanced security in high-risk transactions.

- Biometric Data Protection: Sensitive biometric data must not be stored on agent devices or company servers.

- Real-time Fraud Monitoring: Banks must employ systems to detect and block suspicious transactions immediately.

- Customer Receipts: Agents must provide transaction receipts, and instant SMS alerts are mandatory.

These measures align with RBI’s push to enhance the security and integrity of the Aadhaar Enabled Payment System.

Hardware and Software Requirements for AEPS Onboarding

Onboarding for the Aadhaar Enabled Payment System (AEPS) requires specific, certified hardware and software to ensure secure, biometric-based, and RBI/NPCI-compliant transactions.

Hardware Requirements

Biometric Device: A UIDAI/STQC-certified fingerprint scanner or iris scanner is mandatory.

- Examples: Mantra (MFS100/MFS110).

- Requirement: Must support Registered Device (RD) services for encryption.

Primary Processing Device:

- Android Smartphone/Tablet: Android 5.0 or later, with OTG support to connect the scanner.

- PC/Laptop: Windows 7 or above.

- Micro-ATM/POS Terminal: An all in one Aeps device with a built-in scanner.

- Stable Internet Connection: 4G, Wi-Fi, or broadband for real-time transactions.

- Thermal Printer (Optional/Recommended): For issuing physical receipts to customers.

Software Requirements

- AEPS Application/Portal: The Aeps B2B app or Aeps portal provided by an NPCI-approved Aeps india.

- RD Service Driver: The specific manufacturer’s Registered Device (RD) service driver must be installed on the phone/PC to ensure secure biometric capture.

- Operating System: Android 4.2+ (for app) or Windows 7+ (for PC).

- Web Browser: Updated browser (Chrome/Firefox) if using a desktop web portal.

Mandatory Documents for Onboarding (KYC)

- Aadhaar Card: Must be linked to a mobile number and a bank account.

- PAN Card: For identity and tax compliance.

- Bank Account Details: Cancelled cheque or first page of the passbook for settlement.

- Passport-sized Photographs: Recent photos.

- Business/Shop Address Proof: Utility bill or rent agreement (optional but recommended).

Key Technical & Regulatory Considerations

- One Operator, One Bank: RBI regulations (as of 2026) dictate that an agent can be linked to only one acquiring bank.

- Re-KYC: If an agent is inactive for three months, a fresh KYC is mandatory.

- Geo-Tagging: The Aeps admin app may require the device to be within a specific distance (e.g., 20km) of the registered location.

- Data Security: Raw biometric data cannot be stored on the agent’s phone/PC; it must be encrypted via RD services.

Aeps onboarding Npci Guidelines 2026

Effective January 1, 2026, NPCI and RBI guidelines for AePS onboarding mandate strict full KYC, mandatory agent background checks, and a “One Operator, One Bank” policy to enhance security. Agents inactive for 3 months must undergo re-KYC. Only UIDAI-certified Registered Devices (RD) are permitted, and real-time transaction monitoring is required.

Key 2026 AePS Onboarding Guidelines & Compliance:

- Mandatory Full KYC: Banks must conduct rigorous KYC on all AePS Touchpoint Operators (ATOs) before onboarding, including verification of Aadhaar, PAN, and bank account details.

- One Operator, One Bank Rule: To improve accountability, an agent can only be mapped to one acquiring bank, preventing multiple affiliations.

- Agent Inactivity Policy: If an agent has no transactions for 3 consecutive months, a mandatory re-KYC process must be completed before they can resume services.

- Device Compliance: Only UIDAI-certified, STQC-compliant biometric (fingerprint/iris) devices with active Registered Device (RD) services are permitted to prevent tampering.

- Transaction Monitoring: Banks must monitor transactions in real-time, focusing on volume, frequency, and location to detect fraud.

- Documentation Required: Aadhaar, PAN, bank account proof (cancelled cheque/passbook), and a photograph are essential for registration.

These measures are designed to strengthen the security of Aadhaar-based transactions, ensuring that only verified, active, and compliant operators manage the Aadhaar Enabled Payment System.

How AEPS Onboarding Helps in Financial Inclusion and Rural Banking Growth

The onboarding of the Aadhaar Enabled Payment System (AEPS) has emerged as a cornerstone of financial inclusion in India, transforming rural banking by converting local kirana shops into “mini-banks”. By enabling secure, biometric-based transactions using an Aadhaar number, AEPS eliminates the need for physical bank branches, debit cards, or PINs, making financial services accessible to the unbanked and underbanked rural population.

Here is how AEPS onboarding helps in financial inclusion and rural banking growth:

1. Enhanced Financial Access & Inclusion

- Doorstep Banking: AEPS brings banking services directly to remote villages through Banking Correspondents (BCs) or Bank Mitras, saving villagers time and money on travel to distant bank branches.

- Cardless & PIN-less Transactions: By using biometric authentication (fingerprint or iris scan) linked to the Aadhaar number, AEPS allows users to securely withdraw cash, check balances, and transfer funds without needing to remember complex PINs or carry plastic cards.

- Support for Low Literacy/Disabled Users: The reliance on biometric data ensures that elderly, disabled, or non-literate individuals can independently access their funds without relying on others.

2. Direct Government Benefit Transfers (DBT)

- Reduced Corruption & Leakage: AEPS enables the seamless transfer of government subsidies, pensions, and wages (e.g., MGNREGA) directly into Aadhaar-linked accounts.

- Instant Cash Availability: Beneficiaries can immediately withdraw their payments at local service points, ensuring they have timely access to funds.

3. Rural Banking Growth & Infrastructure

- Low-Cost Expansion: Aeps india AEPS provides a low cost Aeps, scalable alternative to building physical branches, allowing them to expand their reach in rural areas.

- Interoperability: AEPS allows customers to access their bank accounts from any bank at any authorized AEPS-enabled terminal, enhancing service availability.

- Micro-ATM Revolution: The use of handheld, portable Micro ATM by agents enables, secure, and real-time banking in areas with low infrastructure, facilitating high-volume, low-cost transactions.

4. Boost to Local Economy & Digital Literacy

- New Revenue Streams for Retailers: Local shopkeepers and kirana store owners can act as BCs, earning commissions (₹2–₹15+ per transaction) while increasing footfall in their shops.

- Digital Adoption: Regular interaction with AEPS systems helps bridge the digital divide, increasing financial literacy and encouraging rural populations to embrace digital payments.

5. Increased Security

- Biometric Verification: Transactions require live, unique biometric authentication, which significantly reduces the risk of fraud compared to traditional PIN-based or card-based systems.

Key Onboarding Requirements:

To become an AEPS agent, individuals must complete a Full KYC (Know Your Customer) process,, have an Aadhaar-linked bank account, and use a UIDAI-certified biometric device. As of 2026, regulations require strict “one operator, one bank” rules to ensure accountability and reduce fraud.

Aeps Kyc Mendetiory for AEPS Onboarding

As of January 1, 2026, the RBI mandates strict, full KYC for all Aadhaar Enabled Payment System (AePS) Touchpoint Operators (ATOs) during onboarding to combat fraud. Agents must complete biometric verification, link Aadhaar/PAN, and adhere to a “one-operator-one-bank” rule. Re-KYC is required for agents inactive for three months.

Key Aspects of AEPS KYC for Onboarding:

- Mandatory Requirement: All agents, retailers, and Business Correspondents (BCs) must undergo comprehensive, full KYC.

- Document Submission: Required documents include Aadhaar, PAN, bank account details, and a live photograph.

- Biometric Verification: Agents must authenticate using their own biometrics on a UIDAI-certified Aeps device.

- “One Operator, One Bank” Rule: To improve security, an agent can only be registered with one acquiring bank.

- Re-KYC: If an operator is inactive for three consecutive months, they must complete a fresh Aeps KYC process to resume services.

- Onboarding Process: Acquiring banks are responsible for conducting thorough due diligence before authorizing any operator.

These regulations aim to enhance security and prevent misuse of the AePS network, particularly after reports of fraud related to unauthorized transactions.

Common Problems During AEPS Onboarding and Easy Solutions

Common problems during AePS (Aadhaar Enabled Payment System) onboarding and usage usually stem from data mismatches, biometric failures, or bank-side issues. The system requires exact alignment between Aadhaar records, bank records, and the user’s physical biometrics.

Here are the most common challenges and their easy solutions, based on industry guidelines:

1. Biometric Authentication Failures (Scanner Won’t Read)

- Problem: Fingerprint, thumb, or iris scan fails due to worn-out, dirty, dry, or wet skin, or dirty sensors.

- Solutions:

- Clean and Dry: Wipe fingers and the scanner surface with a clean cloth.

- Moisturize: If skin is too dry, use a small amount of lotion or water, then dry slightly.

- Try Another Finger: If one finger fails, try another registered finger.

- Iris Scan: If fingerprint fails repeatedly, use IRIS authentication if the device supports it.

- Clean Sensor: Ask the agent to clean the device scanner.

2. Aadhaar Not Linked to Bank Account

- Problem: The transaction fails because the Aadhaar number is not seeded with the specific bank account.

- Solution: Visit your bank branch and request to “link Aadhaar for DBT (Direct Benefit Transfer) and AePS”.

3. Name or Date of Birth Mismatch

- Problem: The name or DOB in the bank records does not match the Aadhaar card exactly.

- Solution: Visit an Aadhaar Enrollment Centre to update your details to match your bank passbook, or update bank records to match Aadhaar.

4. Incorrect Bank Selected / Multiple Accounts

- Problem: If you have multiple bank accounts linked to your Aadhaar, the system may default to the wrong one.

- Solution: Ask the agent to check which bank is mapped in the NPCI mapper or select the correct bank during the transaction.

5. Account Inactive or Dormant

- Problem: The bank account has not been used for a long time, making it inactive.

- Solution: Make a small deposit or withdrawal at the bank branch to reactivate the account.

6. Technical Issues: Timeouts and Network Failures

- Problem: Slow internet at the agent location or server downtime (Bank or NPCI).

- Solutions:

- Wait: Retry the transaction after a few minutes.

- Check Status: If money is debited but transaction fails, check the balance before trying again to avoid double debits.

- Switch Network: Move to a spot with better signal strength.

7. Exceeded Transaction Limits

- Problem: Daily or per-transaction limits set by the bank are exceeded.

- Solution: Try again the next day or check with the bank regarding limits.

Summary Table for Quick Fixes

| Issue | Root Cause | Immediate Action |

|---|---|---|

| Error 103 | Aadhaar not mapped | Visit bank, link Aadhaar |

| Error 202 | Biometric Mismatch | Clean fingers/Try another finger |

| Error 501 | Insufficient Balance | Add funds to account |

| Error 909 | Timeout/Network Issue | Wait 15-30 mins, check balance |

| Error 203 | Biometric Locked | Unlock via UIDAI website |

Proactive Tips for Smooth Onboarding

- Check Linkage Status: Use the NPCI mapper tool on their website to verify which bank is linked to your Aadhaar.

- Keep Biometrics Updated: If you are a laborer or elderly, update your biometrics at an Aadhaar center every few years.

- Use Authorized Agents: Only use authorized CSP (Customer Service Point) agents or bank officials.

How to Select the Best AEPS Onboarding Company in India

Aeps india one of the best AEPS onboarding company in India requires prioritizing safety, transaction reliability (98%+ success rate), high commissions (₹5-₹15), and instant settlement capabilities (T+0 or T+1). Choose NPCI/RBI-compliant Aeps india offering 24/7 support, user friendly Aeps portals, and value-added services like mini-ATMs and utility payments.

Key Factors for Evaluating AEPS Providers

- Regulatory Compliance & Security: Ensure the Aeps india is authorized by the National Payments Corporation of India (NPCI) and provides secure, encrypted, and compliant transactions.

- User Interface (UI): The b2b Aeps app or Aeps b2b portal should be easy to use for both agents and end-customers.

- Transaction Success Rate & Uptime: Aeps india with a proven track record of high success rates (ideally

98%+98%+) and minimal downtime.

98%+98%+) and minimal downtime. - Settlement Speed: Aeps india that provide instant or same-day (T+0 or T+1) settlements to ensure your working capital remains fluid.

- Commission & Fees: Aeps platforms offering transparent, competitive commissions (e.g., up to ₹13-₹15 per transaction). Check if they offer free or low-cost ID activation.

- Onboarding & Support: Prioritize firms with fast, simple KYC and 24/7 customer support (via phone/WhatsApp).

- Additional Services: Aeps india should allow for diversified income streams through services like Bill Payments (BBPS), Mobile/DTH Recharge, and Mini ATMs.

Top Considerations for Onboarding

- Free vs. Paid ID: Aeps india offer free AEPS ID registration, which is ideal for beginners.

- Additional Services: Aeps india offer supplementary services like DMT (Domestic Money Transfer), Bharat BillPay (BBPS), and recharge options to increase income streams.

- Documentation: Prepare necessary KYC documents, including Aadhaar card, PAN card, and a bank account for quick registration.

Recommended Steps to Choose

- Evaluate Reputation: Check reviews and testimonials of the Aeps india to gauge their reliability.

- Test the Platform: Use a demo if available to test the speed and user interface.

- Review Support Turnaround: Test their customer service responsiveness before committing.

Disclaimer: Aeps India are frequently mentioned in the industry, but users should conduct their own due diligence.

Why AEPS India is the Right Choice for AEPS Onboarding Solutions

Aeps india is an top AEPS onboarding provider is considered the right choice because they transform retail shops into secure “mini-banks” through quick, paperless, and compliant processes. Aeps india are crucial for enabling Aadhaar-based transactions like cash withdrawals, balance inquiries, and mini-statements using only a customer’s biometric authentication.

Here is why choosing a top AEPS provider for onboarding is essential:

1. Fast, Simple, and Paperless Onboarding

- Rapid Activation: Aeps india offer digital e-KYC processes that allow retailers to activate AEPS services within 1–3 business days.

- Minimal Documentation: Aeps Onboarding generally requires basic documents (Aadhaar, PAN, Bank details), making it accessible for small shop owners.

- No High Investment: Requires minimal infrastructure, often just a smartphone or computer and a certified biometric scanner.

2. High Transaction Success and Security

- High Success Rates: Aeps india ensure high transaction success rates (often 98%+) due to robust, multi-bank connected servers.

- NPCI/RBI Compliance: They ensure all Aeps onboarding, agent KYC, and transactions are fully compliant with National Payments Corporation of India (NPCI) and RBI guidelines, protecting agents from legal risks.

- Secure Authentication: The use of STQC-certified biometric devices (fingerprint/iris scanners) ensures safe, fraud-resistant transactions.

3. Attractive Earnings and Quick Settlements

- High Commissions: Aeps india offer competitive commissions, often ranging from ₹2 to ₹15+ per transaction, depending on the volume and transaction value.

- Instant/Daily Settlements: To maintain cash flow, Aeps india offer same-day or instant settlement of funds (T+0 or T+1) to the agent’s wallet.

4. Technical and Operational Support

- 24/7 Support: Aeps india offer around-the-clock technical assistance for transaction failures, device troubleshooting, and portal management.

- User-Friendly Apps/Portals: Aeps india provide intuitive, easy-to-use mobile aeps apps and web portals that require minimal training for daily operations.

- Training & Marketing: Assistance is provided to train agents on using the technology and marketing the services to local customers.

5. Business Growth and Diversification

- Increased Footfall: Offering banking services increases customer visits, helping retailers boost sales of other products by up to 20%.

- Value-Added Services: Aeps india enable access to additional income streams, including Domestic Money Transfer (DMT), BBPS (bill payments), mobile/DTH recharge, and Micro ATM service.

- White Label Solutions: Aeps india offer white label AEPS API to build their own branded, customized Aeps banking platform.

By choosing a trusted AEPS service provider like Aeps india, retailers can securely tap into the growing digital economy, creating a stable and long-term income source.

Future Trends AePS Onboarding

Future trends in AePS (Aadhaar Enabled Payment System) onboarding are heavily defined by the January 1, 2026, RBI mandates, which focus on stringent security, rigorous KYC, and enhanced fraud management. The system is evolving from a simple, high-risk,, walk-in model to a secure, “one operator-one bank” framework with AI-driven monitoring.

Here are the key future trends in AePS onboarding and service, based on 2026 standards:

1. Stricter Regulatory Compliance (Effective Jan 2026)

- Mandatory Full KYC & Re-KYC: All AePS Touchpoint Operators (ATOs) must undergo strict full KYC, similar to bank employee screening. Inactive agents (no transactions for 3 consecutive months) will face mandatory re-KYC to resume services.

- “One Operator, One Bank” Rule: To improve accountability and prevent fraud, an agent is restricted to being linked with only one acquiring bank.

- Rigorous Due Diligence: Acquiring banks are now responsible for the entire,, on-the-ground,,,, auditing of their agents, reducing the reliance on third-party aggregators.

- Location Constraints: Transaction activity must be consistent with the registered geographic location of the operator.

2. Hyper-Secure Technology & Authentication

- Advanced Biometrics & Liveness Detection: Moving beyond simple fingerprint scans, new, systems require AI-powered, multi-modal biometrics (fingerprint, iris, face) combined with, mandatory liveness detection to prevent spoofing with, fake, silicon, fingerprints.

- L1-Certified Devices: Mandatory migration to L1-certified, biometric,, devices, which offer better encryption and security over, older, L0, devices.

- AI-Driven Risk Management: Implementation of, Artificial Intelligence (AI) and Machine Learning (ML) for, real-time transaction, monitoring, behavioral analysis, and, fraud, detection,.

3. Shift in Onboarding Experience

- Digital & Instant Onboarding: Despite stricter rules, the onboarding process is becoming faster through digital, paperless, e-KYC and video KYC, often resulting in, agent, activation within 1–2 days.

- Embedded Finance & Multi-Service Hubs: Retail agents are transforming into,, complete, rural, financial, hubs. Onboarding now includes,, not just, cash, withdrawal, but,, training for, insurance premium collection, micro-loans,, PAN card services, and utility bill payments (BBPS).

- Mobile-First Design: Enhanced, user-friendly, mobile apps are, now standard, allowing,, agents, to easily monitor, transactions, and manage,, wallets.

4. Integration with Digital Ecosystems

- Deeper UPI/Wallet Linking: AEPS integrating with, Unified Payments Interface (UPI) and,, digital, wallets for better,, cash, flow management.

- Blockchain Exploration: There is an, increasing, exploration of, blockchain technology to ensure,, immutable, and, transparent, transaction, records,.

Key Takeaways for Agents & Retailers

- High Revenue Potential: Despite higher compliance, the,,,,, commission-based,, model remains, lucrative, with earnings potential up to, ₹15, per, transaction,.

- Focus on Security: Agents must adhere strictly to “no data storage” policies and, use, certified, devices to avoid, penalty or, suspension.

- Increased Trust: The, tightening, of, rules by, RBI enhances, customer, trust in, local,, Kirana, stores, and, shops acting as, Banking, Correspondents,.

Conclusion

AEPS onboarding is becoming one of the best opportunities for new businesses, retailers, and entrepreneurs who want to enter the digital financial services market in India. With the growing demand for Aadhaar Enabled Payment System services, especially in rural and semi-urban areas, starting an AEPS business is a smart and profitable decision. It helps provide essential banking services like cash withdrawal, balance inquiry, mini statement, and money transfer to customers who may not have easy access to traditional banks.

AEPS (Aadhaar Enabled Payment System) Onboarding is the registration process for agents (merchants) to become authorized banking correspondents, enabling them to offer services like cash withdrawals, deposits, and balance inquiries using biometric authentication. It involves KYC, connecting with an Aeps india, and setting up hardware.

AEPS (Aadhaar Enabled Payment System) Onboarding is the registration process for agents (Business Correspondents) to become authorized to offer banking services such as cash withdrawal, deposit, and balance inquiry using biometric authentication. It involves submitting KYC documents (Aadhaar, PAN, bank details) through a Aeps india to access NPCI’s network.

By following the proper AEPS onboarding process, completing KYC verification, and choosing top AEPS API and AEPS software solutions, new businesses can quickly launch their services and start earning good Aeps commissions. AEPS not only helps retailers increase their income but also supports financial inclusion and rural banking services, which are very important for India’s digital growth.

The complete AEPS onboarding process is simple, secure, and designed to help new businesses start quickly with minimal investment. By completing proper AEPS registration, KYC verification, and Aeps admin software integration, businesses can offer reliable banking services to customers, especially in rural and semi-urban areas where banking access is limited. This not only helps businesses grow their transaction volume but also supports financial inclusion and digital banking expansion across India.

Partnering with a trusted Aeps platform like AEPS India ensures smooth onboarding, advanced AEPS API integrated, high transaction success rates, and strong technical support. Businesses can easily manage retailers, track transactions, and generate higher commissions through secure and scalable AEPS solutions.

If you want to start a low-investment and high-demand fintech service, AEPS onboarding in India is a smart and future-ready choice. With the increasing use of Aadhaar-enabled payment systems and digital banking services, businesses that start AEPS services today can achieve long-term growth and success in the Indian financial market.

Frequently Asked Questions (FAQs) – AEPS Onboarding: Complete Step-by-Step Guide for New Businesses

AEPS onboarding is the registration process that allows businesses, retailers, and service providers to start offering Aadhaar Enabled Payment System (AEPS) services. After onboarding, businesses can provide services like cash withdrawal, balance inquiry, mini statement, and money transfer using Aadhaar authentication.

Any retailer, shop owner, CSC operator, fintech startup, or small business owner can start an AEPS service business. You only need basic documents, a biometric device, and partnership with a top AEPS service provider like AEPS India.

AEPS onboarding is available for retailers, distributors, fintech companies, banking correspondents, and digital payment service providers. Any business that wants to offer Aadhaar-based banking services can apply through Aeps india.

To complete AEPS registration, businesses usually need:

Aadhaar card

PAN card

Business registration details

Bank account details

Passport-size photograph

Mobile number and email ID

These documents help verify identity and ensure safe onboarding.

The AEPS onboarding process usually takes a few hours to a few working days depending on document verification, KYC approval, and Aeps setup. Aeps india offer quick and hassle-free onboarding support.

After successful onboarding, businesses can provide:

AEPS cash withdrawal services

Aeps Balance inquiry services

Aeps Mini statement services

Aeps based fund transfer

Aeps Micro ATM banking services

These services help businesses attract more customers and increase earnings.

Yes, AEPS onboarding follows strict verification and compliance guidelines. Transactions are protected using biometric authentication and Aadhaar verification, making AEPS one of the most secure digital banking solutions in India.

AEPS onboarding helps businesses expand financial services, earn commission on transactions, improve customer reach, and grow in the digital payment sector. It also helps businesses support financial inclusion in rural and semi-urban areas.

The investment required for AEPS onboarding is usually low and depends on the Aeps india, infrastructure, and service features. Aeps india offer cost-effective Aeps onboarding solutions for startups and small businesses.

Businesses earn commission on every successful AEPS transaction such as cash withdrawal, fund transfer, or balance enquiry. Higher transaction volume helps increase overall income and business growth.

Yes, AEPS is specially designed to support rural banking and financial inclusion. It allows people in remote areas to access banking services without visiting bank branches, which increases demand for Aeps india.

Yes, the AEPS business model is highly profitable because retailers earn commission on every transaction. With increasing demand for digital banking and rural financial services, AEPS provides regular income opportunities.

No, you do not need advanced technical skills. Most AEPS software providers like Aeps india offer easy-to-use dashboards and full technical support, making it simple for beginners to operate.

To start AEPS services, you need:

Android mobile or computer

Biometric fingerprint scanner

Stable internet connection

AEPS software or application

These tools help complete secure Aadhaar-based transactions.

AEPS transactions are highly secure because they use biometric authentication and Aadhaar verification. Aeps india also use encrypted payment gateways and advanced security systems.

Yes, AEPS plays a major role in financial inclusion in India. It helps rural customers access banking services without visiting bank branches, making financial services more accessible and convenient.

The AEPS business investment is low compared to other fintech services. You mainly need a biometric device, internet connection, and registration with a Aeps india.

Businesses should choose an Aeps india that offers secure Aeps API integration, fast Aeps onboarding, reliable transaction processing, strong technical support, and compliance with government regulations.

Yes, advanced AEPS API solutions are built to handle large transaction volumes with fast processing and high success rates. This allows businesses to serve more customers without service interruptions.

To select the Aeps india, businesses should check service reliability, transaction success rate, pricing, customer support, security features, and Aeps integration process. Choosing a Aeps india ensures smooth Aeps onboarding and long-term business growth.

Yes, AEPS business is one of the fastest growing opportunities in the digital payment and fintech sector. With increasing demand for Aadhaar based banking services, businesses can generate stable income and expand their customer reach easily.

Yes, businesses can combine AEPS services with:

Mobile recharge services

DMT (Domestic Money Transfer)

Bill payment services

PAN card services

BBPS services

This helps create a complete digital payment solution and increases earning potential.

What Is AEPS Debit Facility in India? Complete Guide

AEPS Provider Explained: Benefits, Features, and How It Works