Complete Guide to AEPS Banking in India

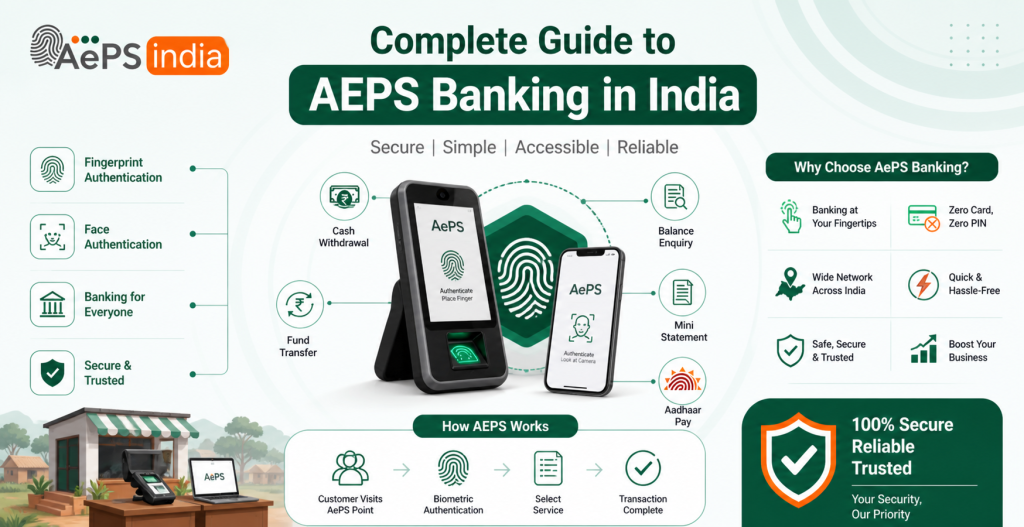

AEPS banking in India has made basic banking services simple, fast, and accessible for everyone. The Aadhaar Enabled Payment System (AEPS) allows customers to use their Aadhaar number and biometric verification to access services like cash withdrawal, balance enquiry, mini statement, and fund transfer without a debit card or PIN. This system is especially helpful in rural and semi-urban areas, where traditional banking access is limited.

Aadhaar Enabled Payment System (AEPS) is a bank-led model authorized by the National Payments Corporation of India (NPCI) that allows customers to perform financial transactions such as cash withdrawals, deposits, and balance inquiries using their Aadhaar authentication (fingerprint/iris scan) at Micro-ATMs or via Business Correspondents. It enables secure, cardless, and PIN-less banking, aimed at increasing financial inclusion in rural areas.

For retailers, CSPs, and fintech businesses, AEPS banking offers a strong opportunity to earn daily commission income while providing trusted banking services to customers. By partnering with a reliable platform like Aeps India, businesses can offer secure, RBI-compliant AEPS services with high success rates and smooth transactions.

Aeps India offers a comprehensive AEPS platform designed for retailers, agents, and Aeps B2B businesses. Our solution is user-friendly, secure, and scalable, enabling businesses to expand their services while increasing revenue and customer trust. With AEPS businesses can serve more customers, reduce transaction time, and stay compliant with RBI and NPCI guidelines.

This complete guide to AEPS banking in India is designed to help customers, retailers, and businesses understand how AEPS banking works, its key features, benefits, eligibility, and usage. If you are looking for a safe digital banking solution or planning to start AEPS services, this guide will give you clear and practical information to make the right decision.

What Is AEPS Banking

AEPS in banking is a system by NPCI that lets customers perform basic banking (cash withdrawal, deposit, balance inquiry, fund transfer) using their Aadhaar number and biometric (fingerprint/iris) authentication at Micro ATMs or Business Correspondents, enabling financial inclusion by making services accessible without cards or internet at merchant points.

AEPS Banking Work

Aadhaar Enabled Payment System (AePS) is a bank-led model allowing users to perform, cash withdrawals, balance inquiries, and mini-statements using their Aadhaar number and fingerprint/iris scan at a micro-ATM or banking correspondent, eliminating the need for physical debit cards or PINs. It enables secure, immediate, and accessible banking services in rural areas.

Core Functions of AePS Banking Work:

- Cash Withdrawal: Users can withdraw cash from their Aadhaar-linked bank accounts.

- Balance Enquiry: Instant checking of account balance.

- Mini Statement: Generating a mini-statement to review recent transactions.

- Fund Transfer: Facilitating transfers between Aadhaar-linked accounts.

- Cash Deposit: Allowing cash deposits at business correspondent locations.

How AePS Transactions Work:

- Visit Agent: Customer visits a banking correspondent or a Micro ATM.

- Authentication: Customer provides their 12-digit Aadhaar number, selects the bank, and chooses the transaction type.

- Biometric Verification: Customer scans their finger or iris for identification.

- Transaction Completion: The system verifies data with the Unique Identification Authority of India (UIDAI) and the issuing bank to process the transaction.

- Receipt: A receipt is issued for the transaction.

Types of AEPS Transactions

Aadhaar Enabled Payment System (AEPS) facilitates essential, secure, and instant banking transactions—specifically cash withdrawal, balance inquiry, mini statement, cash deposit, and Aadhaar-to-Aadhaar fund transfer using only an Aadhaar number and biometric authentication. These transactions are typically performed at micro-ATMs or via banking correspondents.

Key Types of AEPS Transactions:

- Cash Withdrawal (CW): Allows customers to withdraw cash from their linked bank accounts, typically with transaction limits ranging from ₹1,000 to ₹10,000.

- Balance Enquiry (BE): Provides real-time information on the available balance in the user’s account.

- Mini Statement (MS): Enables users to view the last 5 to 10 transactions in their account.

- Cash Deposit (CD): Allows direct deposit of funds into a bank account linked to the user’s Aadhaar, often with limits up to ₹10,000.

- Aadhaar to Aadhaar Fund Transfer: Enables direct money transfer between two Aadhaar-linked bank accounts.

- BHIM Aadhaar Pay: A merchant-centric payment method allowing merchants to accept payments from customers via Aadhaar authentication.

AEPS serves as a vital tool for rural banking, eliminating the need for physical bank branches, debit cards, or PINs for transactions.

AEPS Banking Services Available in India

Aadhaar Enabled Payment System in India provides secure, 24/7 banking services via Business Correspondents (BCs) or micro-ATMs using biometric authentication. Key services include cash withdrawals, deposits, balance inquiries, mini-statements, and Aadhaar-to-Aadhaar fund transfers. Major providers include Aeps india.

Key AEPS Banking Services in India

- Cash Withdrawal: Customers can withdraw cash from their linked bank accounts without a debit card.

- Cash Deposit: Instant cash deposits into Aadhaar-linked accounts.

- Balance Enquiry: Real-time checking of the available account balance.

- Mini Statement: Access to the last few transactions.

- Aadhaar to Aadhaar Fund Transfer: Secure, instant money transfers between two Aadhaar-linked accounts.

- BHIM Aadhaar Pay: Merchant payments using Aadhaar authentication.

- eKYC: Instant, paperless identification for opening bank accounts.

Operational Details

- Authentication: Transactions require Aadhaar number and biometric scan (fingerprint or iris).

- Accessibility: Services are available through authorized agents, micro-ATMs, and banking kiosks.

- Major Banks Involved: State Bank of India, Punjab National Bank, ICICI Bank, HDFC Bank, Axis Bank, Bank of Baroda, Paytm Payments Bank, and India Post Payments Bank.

- Key Fintech Providers: Aeps india.

This system significantly boosts financial inclusion, especially in rural areas, by removing the need for physical bank branches.

Documents Required for AEPS Banking

To register AEPS banking as an agent, essential documents include an Aadhaar card, PAN card, bank account details (passbook or cancelled cheque), a registered mobile number, and a passport-sized photograph. A Aeps biometric scanner (fingerprint/iris) and proof of business address (shop registration) are also required.

Key Documents and Requirements for AEPS Registration

- Aadhaar Card: The primary document for identification and verification.

- PAN Card: Mandatory for identity verification and business compliance.

- Bank Account Details: An active bank account (savings or current) linked to the Aadhaar card, with a passbook or cancelled cheque for verification.

- Mobile Number: A functional mobile number linked to the Aadhaar card for OTPs and transaction alerts.

- Passport-sized Photo: Required for the registration process.

- Proof of Address/Business: Documents for the workplace, such as a shop rental agreement, utility bill (electricity/landline), or trade license.

- Biometric Device: A compatible fingerprint or iris scanner device is necessary for authentication.

Customer Requirements for Using AEPS

- Aadhaar Number: Must be linked to the bank account.

- Bank Name: The customer must know their bank name.

- Biometric Data: Fingerprint or iris scan for authentication.

Important Notes

- The bank account MUST be Aadhaar-enabled.

- The maximum transaction limit for a single AEPS transaction is often set by NPCI, generally up to ₹10,000.

- The Aeps service is available to Indian residents.

AEPS Banking Eligibility Criteria

AEPS (Aadhaar Enabled Payment System) requires users to have an Aadhaar-linked bank account and biometric authentication (fingerprint/iris) to perform transactions. Eligible individuals must be Indian residents, while agents/retailers need a shop, smartphone/PC, a Aeps biometric device, and valid Aeps KYC documents (PAN, Aadhaar).

Key Eligibility Criteria for Customers:

- Aadhaar Linking: The bank account must be seeded (connected) with the user’s Aadhaar number.

- Authentication: Valid Aeps biometric data (fingerprint or iris scan) registered with UIDAI.

- Active Account: The account must be active and not frozen.

Key Eligibility Criteria for Agents (Retailers/Merchants):

- Age: Minimum 18 years.

- Citizenship: Indian national.

- Location: A permanent, physical shop or kiosk, often required to be in a rural area for certain BC models.

- Equipment: A smartphone or PC, stable internet, and a registered Aeps biometric device (fingerprint/iris scanner).

- Documentation: Aadhaar card, PAN card, and bank account details for commission settlement.

Transaction Limits & Details:

- Max Limit: Generally ₹10,000 per transaction.

- Monthly Limits: Banks may restrict transactions to a maximum of 5 to 10 transactions or ₹50,000 to ₹1,00,000 per month.

- Services: Enables cash withdrawal, balance inquiry, mini-statement, and Aadhaar-to-Aadhaar fund transfers.

Important Notes:

- Transactions are generally free for customers, but agents may charge fees.

- RBI has tightened rules in 2026 to increase security, requiring more stringent KYC for operators.

- It is highly recommended to have a dedicated, fixed shop for operating as an AEPS agent.

Who Can Use AEPS Banking Services?

Aadhaar Enabled Payment System (AEPS) can be used by any Indian resident with an Aadhaar-linked bank account, particularly benefiting those in rural or remote areas with limited bank access. It allows users to perform basic banking, such as cash withdrawals, deposits, and balance inquiries, using only their Aadhaar number and biometrics (fingerprint or iris scan) via a Business Correspondent (BC).

Key Requirements for Using AEPS:

- Active Bank Account: Must be linked with a valid 12-digit Aadhaar number.

- Biometric Data: Fingerprint or iris scan must be registered with the Aadhaar database.

- Supported Bank: The account must be with a bank that participates in the NPCI AEPS network.

- Agent/Device: A banking correspondent (BC) with a micro-ATM or Aeps Android app.

Who Specifically Benefits from AEPS?

- Individuals without Debit/Credit Cards: No need for physical cards or PINs.

- Rural Population: People in areas with few ATMs or bank branches.

- Elderly or Illiterate Individuals: Simple Aeps biometric authentication replaces complex, secure, or memorable codes.

- Individuals with Limited Mobile Literacy: No need to navigate complex banking apps.

Who Can Start AEPS Banking Business in India?

Any Indian citizen aged 18 or older, including small shopkeepers, kirana store owners, CSC center operators, and individuals, can start an AEPS banking business. Requirements include a valid Aadhaar/PAN card, an Aadhaar-linked bank account, a smartphone or PC, and a registered Aeps biometric scanner.

Key Requirements to Start AEPS Business:

- Eligibility: Indian citizen, 18+ years old, with basic computer/smartphone knowledge.

- Documentation: Aadhaar Card (linked to bank), PAN Card, and Bank Passbook/Cancelled Cheque.

- Hardware: Smartphone or computer with a stable internet connection.

- Biometric Device: A registered (RD) Fingerprint or Iris scanner is mandatory for authentication.

- Registration: You must register with an Aeps india.

Potential Operators:

- Existing Shop Owners: Kirana stores, medical shops, or mobile recharge outlets can add banking services.

- Individuals: Entrepreneurs can start this as a low-cost, home-based, or small-office business, particularly in rural or semi-urban areas.

Top Use Cases of AEPS Banking

Aadhaar Enabled Payment System (AEPS) enables bank-led, interoperable financial transactions at retail points via biometric authentication, primarily serving rural and unbanked populations. Top use cases include instant cash withdrawals/deposits, balance inquiries, mini-statements, Aadhaar-to-Aadhaar fund transfers, Direct Benefit Transfers (DBT) for government subsidies, and merchant payments (Aadhaar Pay).

Key Use Cases of AEPS Banking:

- Cash Withdrawal & Deposit: Users can withdraw or deposit cash from their Aadhaar-linked bank accounts at local retail outlets (Business Correspondents/kirana shops), reducing the need to visit bank branches or ATMs.

- Balance Inquiry & Mini Statement: Provides immediate, real-time access to account balances and recent transaction history, enhancing financial transparency for users.

- Direct Benefit Transfer (DBT) Disbursement: Enables the efficient delivery of government pensions, subsidies, and welfare payments directly into beneficiaries’ accounts, reducing fraud and delays.

- Aadhaar-to-Aadhaar Fund Transfer: Facilitates secure, instant, and interoperable money transfers between different bank accounts linked to Aadhaar.

- Merchant Payments (Aadhaar Pay): Allows small merchants to accept cashless payments directly from a customer’s bank account using biometric authentication, promoting a digital economy in rural areas.

- eKYC (Electronic Know Your Customer): Facilitates paperless and real-time customer identity verification, essential for opening new accounts or availing services.

- Financial Inclusion: Acts as a vital tool for bringing banking services to remote, unbanked areas by converting local shops into “mini-banks”.

These services are secure, as they require only an Aadhaar number and biometric data (fingerprint or iris scan) for verification.

AEPS Banking for Rural and Semi-Urban Areas

Aadhaar Enabled Payment System (AePS) is a transformative, secure, and user-friendly banking model by NPCI, enabling rural and semi-urban populations to conduct, cash withdrawals, balance inquiries, and mini-statements using only their Aadhaar number and biometric authentication (fingerprint/iris). It eliminates the need for physical bank branches or debit cards, promoting financial inclusion by allowing local agents to provide,,doorstep banking services via micro-ATMs.

Key Aspects of AEPS in Rural & Semi-Urban Areas:

- Financial Inclusion: Reaches underserved areas with limited banking infrastructure by converting local shops into,banking service hubs.

- Key Services Offered: Cash withdrawals (up to ₹10,000 per transaction/₹50,000 daily),,cash deposits, balance inquiries, and,mini-statements.

- Convenience: Removes the need for PINs, passwords, or,physical bank visits.

- Security: Uses,biometric,authentication (fingerprint/iris), which is safer than,traditional,plastic cards.

- Agent Model: Business Correspondents (BCs) use,micro-ATMs, to provide,services in local,communities.

- Direct Benefit Transfer (DBT): Facilitates direct,government subsidies, (e.g., MGNREGA) to,account holders.

- Income Opportunity: Retailers can earn,commissions,by becoming AEPS agents, often earning ₹15,000–₹25,000 per month in,high-volume,areas.

Benefits to Users & Retailers

- For Users: Easy, safe, and,instant,access to money without,traveling to,distant banks.

- For Retailers: Increased,customer footfall,and additional,income,opportunities.

- Technology: Uses,Aadhaar,authentication for,secure,and instant,transactions.

Future Outlook

AEPS is expected to see over 3.5 billion transactions by 2026, driven by,advanced,biometric,solutions and expanding rural,micro-ATM,infrastructure.

Why AEPS Banking is Important in India

Aadhaar Enabled Payment System (AEPS) is crucial for businesses, especially in rural or underserved areas, as it enables secure, cardless, and PIN-less banking transactions (withdrawals, deposits, transfers) using only biometric authentication. It increases foot traffic, generates extra revenue through commissions, and reduces cash handling risks.

Why AEPS is Essential for Business:

- Increased Revenue: Businesses earn commissions on every transaction, such as cash withdrawals, balance inquiries, and mini-statements.

- Customer Attraction: By turning your shop into a “mini-bank,” you attract more customers, especially those without easy access to bank branches or ATMs.

- Enhanced Security: Transactions are highly secure, relying on Aadhaar authentication (fingerprint/iris) which minimizes fraud and risks associated with handling large amounts of cash.

- Operational Efficiency: It simplifies the payment process, allowing customers to pay for goods or services directly from their bank account, supporting both retail and financial service models.

- Financial Inclusion: It provides essential financial services to unbanked, rural populations, allowing them to access government benefits and manage finances safely.

- Convenience: It removes the need for physical debit/credit cards, which is highly beneficial for customers who do not carry them or in areas with low card penetration.

- Competitive Edge: It helps local retailers compete with larger stores by providing additional, modern, and accessible services.

AEPS turns a regular store into a trusted community financial hub, fostering customer loyalty and boosting daily income.

Features AEPS Banking

Aadhaar Enabled Payment System (AEPS) is a secure, NPCI-developed, interoperable banking model enabling users to perform transactions (cash withdrawal, deposit, balance inquiry, mini-statement) using only their Aadhaar number and biometric/Aeps iris scan authentication at micro-ATMs or with business correspondents. It promotes financial inclusion, requires no PIN/card, and facilitates government direct benefit transfers.

Key Features and Benefits of AEPS

- Secure Biometric Authentication: Transactions are authorized using fingerprint or iris scanning, reducing fraud risk.

- Interoperability: Users can access their bank account through any business correspondent (Bank Mitra) using any bank’s AePS enabled system.

- No Card/PIN Required: Eliminates the need to carry debit/credit cards or remember PINs, enhancing ease of use.

- Financial Inclusion: Enables basic banking services in remote areas where bank branches or ATMs are not easily accessible.

- Transaction Types: Supports cash withdrawal, cash deposit, mini-statement, and Aadhaar-to-Aadhaar fund transfers.

- Direct Benefit Transfer (DBT): Facilitates receipt of government subsidies and pensions directly into bank accounts.

- BHIM Aadhaar Pay: Allows merchants to accept payments from customers via Aadhaar authentication.

- Cost-Effective: Often offers free or low-cost transactions, particularly for small-value, rural, or government-linked transactions.

- Real-time Transactions: Provides immediate, instantaneous processing of banking services.

Benefits AEPS Banking

AePS banking offers, Paytm secure, cardless, and PIN-less transactions using only Aadhaar authentication. It enables instant cash withdrawals, deposits, and balance inquiries via local banking agents or micro-ATMs, specifically benefiting rural, elderly, and unbanked populations. Key advantages include high-security biometric verification, 24/7 access, and seamless delivery of government benefits (DBT).

Key Benefits of AePS Banking:

- Financial Inclusion & Accessibility: Provides banking services, especially to rural and remote areas where bank branches or ATMs are not available.

- No Card/PIN Required: Eliminates the need to carry physical debit cards or remember PINs, using only Aadhaar number and fingerprint for authentication.

- High Security: Biometric authentication (fingerprint or iris scan) makes transactions highly secure and reduces fraud risks.

- Direct Benefit Transfer (DBT): Facilitates the direct receipt of government subsidies and pensions into bank accounts, reducing corruption and delays.

- Interoperability: Allows users to access accounts from any bank using a single, uniform platform (Micro ATM or Business Correspondent).

- Convenience for All: Simple interface enables people with low digital literacy or without smartphones to manage their finances.

- Interoperability: Customers can use any bank-enabled micro-ATM to access their accounts, regardless of their specific bank.

- Instant Services: Provides immediate, real-time access to services like cash withdrawal, deposits, balance inquiries, and mini-statements.

- For Retailers/Agents: Enables shopkeepers to become banking correspondents, generating additional income through commissions on transactions.

- Empowerment for Vulnerable Groups: Provides financial independence for seniors, the disabled, and those with limited mobility.

AEPS API Integration for AEPS Banking

AEPS API integration enables secure, real-time banking transactions cash withdrawal, balance inquiry, and mini-statements using biometric authentication. The process requires partnering with an Aeps india, completing KYC, integrating Aeps API with RD-compliant biometric devices, and passing through a sandboxed testing phase before going live.

Business & Legal Steps

- Choose a Certified AEPS API Provider: Select a Aeps india that is registered with the NPCI and complies with all Reserve Bank of India (RBI) and Unique Identification Authority of India (UIDAI) guidelines.

- Business Registration & KYC: Register your business with the Aeps india and complete the Know Your Customer (KYC) verification process. This usually requires submitting documents such as:

- Aadhaar Card

- PAN Card

- Bank account details (cancelled cheque or passbook copy)

- Company registration documents (if applicable)

- Passport-sized photograph.

- Sign Agreements: Finalize an agreement with the Aeps india that outlines the terms, conditions, transaction fees, and commission structures.

- Acquire and Register Biometric Devices: Purchase UIDAI certified biometric Aeps devices (fingerprint or iris scanners) and install the manufacturer’s Registered Device (RD) service software. These devices must be registered with Aeps india is an AEPS provider for secure data capture.

- Train Agents: Ensure that your agents or end-users are properly trained on how to use the system, handle transactions, manage errors, and provide customer support.

Technical Integration & Deployment Steps

- Obtain API Credentials and Documentation: Aeps india will issue necessary Aeps API keys, client Aeps ID, access tokens, and comprehensive technical documentation (Aeps API endpoints, request/response formats, security protocols) once your registration and verification are complete.

- Development and Integration:

- Develop the user-facing interface for services like cash withdrawal, balance inquiry, and mini-statements.

- Write the back-end logic to make Aeps API calls to the Aeps india endpoints, send transaction requests, and process responses.

- Implement the Aeps biometric devices for Aeps Software Development Kit (SDK) to securely capture and encrypt the customer’s biometric data.

- Testing in a Sandbox Environment: Thoroughly test the entire integration within the Aeps india sandbox (testing) environment to ensure seamless transaction flows and correct error handling before going live.

- Go Live (Production Deployment): After successful testing, the Aeps india will migrate your credentials to the live/production environment. Replace your sandbox credentials with live Aeps API keys and deploy the Aeps application to your live server.

- Monitoring and Support: Continuously monitor transactions for success/failure, reconcile settlements, and establish a mechanism to handle customer complaints and technical issues.

AEPS Registration Process

AEPS registration enables agents to offer banking services like cash withdrawals and balance inquiries. The process involves selecting a Aeps india, completing KYC (Aadhaar/PAN), verifying credentials, installing certified Aeps biometric devices, and activating the agent account to begin secure transactions.

Steps for AEPS Agent Registration:

- Choose an AEPS Service Provider: Select a reputable, government-approved Aeps india offers secure Aeps software, technical support, and competitive commissions.

- Submit Registration Details: Fill out the agent registration form, providing personal details (name, email, address, mobile number), PAN card, and bank account details.

- Complete KYC Verification: Upload mandatory documents Aadhaar card, PAN card, and a photograph for KYC (Know Your Customer) verification. A video KYC or physical verification may be required.

- Register Biometric Device: Purchase a UIDAI-certified Aeps device (fingerprint scanner). Register this Aeps device with the Aeps india to ensure secure, encrypted authentication for transactions.

- Verification and Approval: Aeps india verifies the submitted documents and background. Once approved, the AEPS service activated on your account.

- Installation & Activation: Install the app or software on your smartphone/computer and register your biometric device.

- Training & Login: Complete training on transaction processes, and receive your unique Aeps Agent ID to start operations.

Key Requirements:

- Eligibility: Must be 18+ years old with a valid bank account.

- Connectivity: A stable internet connection is required.

- Documentation: Aadhaar must be linked to the bank account for authentication.

Aeps Banking Onboarding Process

The Aeps onboarding process for the Aadhaar-enabled Payment System (AePS) differs based on whether you are an end-user (customer) looking to make transactions or an agent (retailer/business) looking to offer services.

1. AePS Onboarding for Customers (To Use Services)

For customers, there is no formal “registration” to use AePS; it is a matter of ensuring the service is active on your bank account.

- Link Aadhaar to Bank Account: Visit your home branch, use a bank ATM, or use internet banking to ensure your 12-digit Aadhaar number is linked to your bank account.

- Enable AEPS: Ensure the AePS/digital payment facility is activated by your bank.

- Visit an Agent: Go to an authorized Business Correspondent (BC) or a Micro-ATM point.

- Provide Details: Give your Aadhaar number, select your bank, and choose the transaction type (cash withdrawal, balance check).

- Biometric Authentication: Place your finger on the biometric scanner for verification.

2. AePS Agent/Retailer Onboarding (To Offer Services)

To become an AePS agent and offer services, you must go through a formal Aeps onboarding and KYC process with an Aeps API provider like Aeps india.

- Step 1: Choose a Service Provider/Aggregator: Select a reputable, NPCI-approved AePS service provider like Aeps india.

- Step 2: Submit Registration Documents (KYC): Fill out the Aeps registration form and submit the following documents:

- Aadhaar Card (linked to a mobile number).

- PAN Card.

- Bank Account Details (cancelled cheque or passbook).

- Photograph.

- Business/Shop Address Proof.

- Step 3: Complete E-KYC/Video KYC: Complete the digital Aeps KYC process, which may include a video call or biometric verification to satisfy RBI guidelines.

- Step 4: Acquire and Register Biometric Device: Purchase a UIDAI-certified, STQC-certified fingerprint/iris scanner (e.g., Mantra, Morpho) and register it in the Aeps portal.

- Step 5: Install App and Training: Download the AePS mobile app or Aeps b2b portal, install the RD (Registered Device) service for your scanner, and complete training on transactions.

- Step 6: Activation: Once the Aeps admin verifies all documents, your account is activated, and you can begin offering services.

Key Requirements & New 2026 Rules

- Age: Must be 18 years or older.

- Re-KYC: If an agent is inactive for 3 consecutive months, they must complete a fresh KYC process before resuming services.

- One Operator, One Bank: Each agent can be linked to only one acquiring bank.

- Hardware: A stable internet connection and an Android phone or PC are mandatory.

AEPS KYC Important for Business

Aadhaar Enabled Payment System KYC for businesses is a mandatory, paperless, and biometric-based verification process that allows merchants, agents, or retailers to authenticate their identity for offering banking services like cash withdrawals, balance inquiries, and mini-statements. Businesses must register with an authorized best AEPS provider like Aeps India, submit documents (Aadhaar, PAN, bank details), and use a UIDAI-certified biometric device. This process ensures compliance, security against fraud, and enables instant, secure, and regulated financial transactions.

Key Aspects of AEPS KYC for Businesses

- Mandatory Requirements: To become an AEPS agent or business correspondent, you must provide your Aadhaar number for e-KYC, PAN card, and bank account information for verification.

- Biometric Authentication: A mandatory fingerprint scanner or iris scanner (e.g., Mantra) must be used to link your identity during registration and to process customer transactions.

Steps to Register:

- Select a Provider: Choose a Aeps india.

- Submit Documentation: Provide personal/business details, including PAN, Aadhaar, and bank account (passbook or cancelled cheque).

- Video/Physical KYC: Complete verification via video call or in-person with the Aeps india.

- Device Setup: Register Aeps biometric device on the portal and download the AEPS application.

- Activation: Once approved, typically within 24-48 hours, you receive credentials to begin transactions.

Benefits of AEPS KYC for Businesses

- Increased Trust & Security: Real-time Aadhaar authentication ensures only legitimate transactions occur, significantly reducing fraud.

- Fast Onboarding: The process is entirely digital, enabling faster approvals to start your business.

- High Transaction Success Rates: Properly verified, compliant, and registered agents have higher transaction success rates.

Key Reasons AEPS KYC is Important for Businesses:

- Regulatory Compliance: The Reserve Bank of India (RBI) mandates strict KYC and ongoing monitoring for all AEPS Touchpoint Operators (ATOs) to prevent money laundering and ensure legal safety.

- Fraud Prevention: KYC verifies the identity of agents and users, reducing the risk of unauthorized individuals operating, which prevents “ghost” accounts and fraudulent activities.

- Enhanced Security: Utilizing Aadhaar-linked biometric authentication (fingerprint/iris) ensures that transactions are highly secure and tamper-proof.

- Business Growth: A verified, compliant, and trained agent builds trust in the community, leading to higher footfall and increased commissions from banking services.

- Financial Inclusion: It empowers businesses, particularly in rural areas, to act as local, accessible banks, supporting the digital India initiative.

Regulatory Compliance

Businesses must comply with NPCI and government guidelines, ensuring all transactions are securely processed through certified biometric devices. Failure to maintain proper KYC can result in the suspension of the agent Aeps ID.

Security & Safety in AEPS Banking

AEPS security relies on Aadhaar authentication,, biometric verification (fingerprint/iris), and, encryption to ensure, safe, transactions. Key,, safety, measures include using authorized Aeps agents, verifying, device integrity,, checking transaction, amounts, receiving, receipts, and monitoring SMS alerts. Users must protect personal,, data and never, share, biometrics.

Core Security Measures in AEPS

- Biometric Authentication: Transactions require unique fingerprint or iris scans, making it difficult for unauthorized users to access accounts.

- Encryption: Data is encrypted during transmission, rendering it unreadable to unauthorized parties.

- Trusted Agents: Only, authorized, business correspondents or bank branches should be used.

- Device Safety: Users should check for tampered, or suspicious,, biometric devices.

- Transaction Alerts: Immediate SMS notifications allow users to track activity.

Essential Safety Tips for Users

- Never Share Credentials: Do not share your Aadhaar number or biometrics with anyone.

- Verify Transactions: Always check the amount and transaction type before approving with a, biometric, scan.

- Request Receipts: Ensure you receive a, physical, or digital, receipt for every, transaction.

- Monitor Accounts: Regularly check bank statements for, unauthorized, transactions.

- Report Fraud: Immediately, report, any, suspicious, activity to your bank or the NPCI.

Data Privacy and Compliance

- ISO Standards: Many institutions follow ISO 27001 for information security management.

- Data Protection: Personal information, including Aadhaar details, must be kept secure.

- Authorized Access: Only, authorized, personnel, can operate,, AEPS terminals.

By following these, precautions, users can minimize the, risk of, fraud, in, AEPS, transactions.

AEPS Banking Charges and Commission Structure

AEPS (Aadhaar Enabled Payment System) typically offers agents/retailers a Aeps commission of ₹2–₹25 per cash withdrawal, increasing with transaction value (e.g., ~0.40% or up to ₹25 max for higher amounts), while charges for users are generally free or minimal. Maximum daily withdrawal is ₹50,000, with a single transaction cap of ₹10,000.

AEPS Commission Structure (For Retailers/Agents)

Commissions are usually tiered, meaning higher transaction amounts generate better returns. Effective April 2025, a common structure is:

- ₹100 – ₹999: ~₹2.00

- ₹1,000 – ₹1,999: ~₹3.00 – ₹4.00

- ₹2,000 – ₹2,999: ~₹5.50 – ₹8.00

- ₹3,000 – ₹3,999: ~₹9.00 – ₹12.00

- ₹4,000 – ₹4,999: ~₹16.00

- ₹5,000 – ₹5,999: ~₹20.00

- ₹6,000 – ₹6,999: ~₹24.00

- ₹7,000 & Above: ~₹25.00 (Max Cap)

- Percentage-based: Some structures offer 0.40% commission with a maximum cap of ₹25/- per transaction.

Banking Charges for Customers

- Cash Withdrawal/Deposit: Often ₹5 to ₹25 per transaction, though some banks may charge less.

- Mini Statement/Balance Enquiry: Typically ₹5 + GST, though some may offer this free.

- Service Charges: ₹20 + GST per transaction if exceeding limits.

Other Potential Earnings/Fees:

- Fund Transfer: 0.05% of the amount (max cap: ₹5/-).

- Account Opening: ~₹25 per account (for funded accounts).

- Monthly Incentives: Agents may receive up to ₹2,000 for meeting monthly transaction and account targets.

Key Features and Limits

- Maximum Transaction Limit: ₹10,000 per transaction.

- Daily Transaction Limit: ₹50,000 per day.

- Transaction Types: Cash Withdrawal, Balance Inquiry, Mini Statement, and Fund Transfer.

- Settlement: Typically, commission payouts are processed weekly or monthly depending on the BC (Business Correspondent) model.

Note: The specific Aeps commission rates and charges may vary based on the Aeps india.

AEPS Device and Biometric Requirements for Aeps Banking

AEPS (Aadhaar Enabled Payment System) requires a STQC/UIDAI-certified biometric scanner (fingerprint or iris) that supports Registered Device (RD) services for secure, real-time authentication. Essential hardware includes a 4G-enabled Android smartphone or computer and stable internet connectivity, often paired with a Bluetooth thermal printer for receipts.

Key AEPS Device Requirements

- Biometric Scanner: Must be UIDAI-certified (fingerprint or iris) to ensure security and compliance. Common brands include Mantra (e.g., MFS110 L1),.

- Registered Device (RD) Service: The device must support RD services to securely encrypt biometric data before transmission, as mandated by UIDAI.

- Connectivity: A stable internet connection (4G, Wi-Fi, or Dongle) is mandatory for real-time transaction processing.

- Operating System: Android 4.2 or higher for mobile-based AEPS apps.

- Software/Application: A secure AEPS application or portal (e.g., banking correspondent app) is needed.

- Optional/Peripheral: A thermal printer for receipts, particularly for business operators.

Biometric Requirements for Users

- Aadhaar Linkage: The user’s bank account must be linked with their Aadhaar number.

- Valid Biometrics: Accurate, up-to-date fingerprints or iris scans are necessary for successful authentication.

- No Physical Card: The system operates without a physical debit card or PIN.

Commonly Used Devices

- Standalone Scanners: Mantra MFS100/MFS110 (approx. ₹3,000–₹7,000).

- Micro ATM/All-in-One POS: Includes printer and scanner (approx. ₹10,000–₹30,000+).

Ensure all Aeps devices purchase from Aeps india to guarantee STQC certification.

AEPS Banking Business Model Explained

The Aadhaar Enabled Payment System (AEPS) is a bank-led model designed by the National Payments Corporation of India (NPCI) that allows customers to access their bank accounts and perform basic financial transactions using their Aadhaar number and biometric authentication (fingerprint or iris scan). It is primarily designed to facilitate banking in rural, underserved, or remote areas, acting as a “digital bridge” between consumers and banking services without requiring debit cards, PINs, or smartphones.

Core Components of the AEPS Model

- Customer: An account holder with an Aadhaar-linked bank account.

- Business Correspondent (BC) / Agent: Authorized personnel (often local shop owners/kirana merchants) who possess a micro-ATM or a smartphone with a connected biometric scanner.

- Micro-ATM / POS Machine: The hardware terminal used to scan the fingerprint and initiate transactions.

- UIDAI: Performs the biometric authentication of the customer.

- NPCI: Facilitates the settlement and acts as the central switch.

- Issuer Bank: The customer’s home bank where the account is held.

- Acquiring Bank: The bank that has deployed the Micro-ATM terminal.

How the AEPS Transaction Process Works

- Initiation: The customer visits a Business Correspondent (BC) and provides their Aadhaar number and the name of their bank.

- Transaction Selection: The agent selects the desired transaction type (Cash Withdrawal, Balance Enquiry, etc.) on the Micro-ATM.

- Authentication: The customer places their finger on the biometric scanner.

- Verification: The system sends the data to the Unique Identification Authority of India (UIDAI) for biometric verification.

- Authorization: Upon successful verification, the transaction is processed, and the bank account is debited/credited in real-time.

- Confirmation: The agent receives a confirmation, and the customer gets a receipt or SMS notification.

- Settlement: Upon successful validation, the transaction is processed via NPCI’s switch, and the cash is handed over by the agent.

Key Transactions Supported

- Cash Withdrawal: Withdrawing money directly from the bank account.

- Cash Deposit: Depositing cash into an Aadhaar-linked account.

- Balance Enquiry: Checking the current account balance.

- Mini Statement: Viewing recent transaction history.

- Aadhaar-to-Aadhaar Fund Transfer: Transferring money between accounts linked to the same or different Aadhaar numbers.

The Business Model: How Stakeholders Earn

The AEPS model is a commission-based system that allows agents to generate income.

- Retailers/Agents: Earn a commission for every transaction they facilitate, ranging from ₹5 to ₹15+ depending on the transaction value (e.g., up to ₹13 for a ₹3,000+ withdrawal).

- Distributors: Earn commissions based on the total volume of transactions done by their network of retailers.

- Banks: Benefit from reduced operational costs of setting up physical branches in remote areas, and they earn transaction fees (interchange fee).

4. Revenue Model (Commission Structure)

AEPS operates on a commission-based model. Agents and distributors earn money based on the volume and value of transactions.

- Agent Commission: Retailers can earn up to ₹10-13 or more per transaction of ₹3,000 or higher.

- Tiered Commission: Commissions are generally higher for higher-value withdrawals.

- Additional Revenue: Agents may also earn commissions on balance inquiries (e.g., ₹2 per query).

- Distributor Model: Distributors earn a commission on the total transactions done by their network of retailers.

Key Features and Advantages

- Interoperability: A customer of any bank can transact at any AEPS-enabled micro-ATM or retailer terminal, regardless of the bank the retailer is affiliated with.

- Financial Inclusion: Reaches rural, unbanked, and underbanked populations, including illiterate individuals who cannot remember PINs.

- Doorstep Banking: Enables basic banking at local shops, saving customers the cost and time of traveling to distant bank branches.

- High Security: Relies on unique biometric authentication, reducing risks associated with stolen cards or PINs.

- Direct Benefit Transfer (DBT): Facilitates direct transfer of government subsidies, pensions, and MGNREGA payments.

Limitations and Challenges

- Technical Failures: High rates of transaction failure due to poor internet connectivity in rural areas or biometric mismatches (e.g., worn-out fingerprints).

- Lower Commission Rates: The rise of UPI has led to a decrease in the volume of transactions for some, impacting the income of agents.

- Transaction Limits: NPCI has set a maximum limit of ₹10,000 per transaction to prevent fraud, with some banks limiting total daily withdrawals to ₹50,000.

- Security Risks: Though secure, it is vulnerable to fraud if biometrics are stolen or cloned.

- Default Activation: The service is often enabled by default if the account is linked to Aadhaar, posing security risks if the agent is not trusted.

- Infrastructure Dependency: Requires reliable electricity and internet connectivity, which may be lacking in remote areas.

Security Considerations

- Biometric Matching: As fingerprints can sometimes be replicated, it is crucial to use authorized and secure terminals.

- RRN Number: Every transaction generates a 12-digit Retrieval Reference Number (RRN) to uniquely identify it for dispute resolution.

- Real-time Fraud Detection: The system is continuously upgraded with better technology to detect anomalies.

Future Scope

- Integration with AI/ML: Used for real-time fraud detection and risk management.

- Expanded Services: Future inclusion of micro-loans, insurance premium payments, and more, extending beyond basic banking.

AEPS is a critical financial inclusion tool that has transformed rural banking by utilizing biometric authentication to make banking accessible at the local kirana store.

Disclaimer: AEPS is in its infancy, and while secure, it is recommended to use only verified agents.

AEPS Banking RBI/NPCI Guidelines

RBI and NPCI guidelines for the Aadhaar Enabled Payment System (AePS) focus on enhancing security through mandatory biometric authentication (fingerprint/iris) and strict due diligence for agents, effective January 1, 2026. Key rules require linking Aadhaar to bank accounts, prohibiting unauthorized agents, enforcing, transaction limits (typically ₹10,000 per withdrawal), and mandating KYC for AePS Touchpoint Operators (ATOs) to prevent fraud.

Key RBI/NPCI Guidelines (Effective Jan 1, 2026)

- Operator Due Diligence: Acquiring banks must conduct thorough KYC and due diligence on AePS Touchpoint Operators (ATOs), with mandatory renewals for inactive operators.

- Transaction Monitoring: Banks are required to monitor transaction patterns (volume, frequency, location) to identify potential fraud.

- Secure Authentication: Transactions require biometric authentication (fingerprint or iris scan) via registered, non-tampered devices.

- Prohibition of Extra Charges: Agents (BCs) are strictly prohibited from charging extra fees to customers for AePS services.

- Account Selection: Only the primary account linked to the Aadhaar number can be used for transactions.

Usage Guidelines for Customers

- Mandatory Linking: Bank accounts must be linked with Aadhaar.

- Transaction Limits: Daily withdrawal limits are generally capped at ₹10,000 per transaction, with total daily limits around ₹50,000, varying by bank.

- Verification: Always verify transaction details on the micro-ATM screen before providing biometric consent.

- Receipts: Ensure a digital or physical receipt is received for every transaction.

- Security: Avoid sharing Aadhaar details with unknown individuals and regularly check bank statements.

Compliance for Business Correspondents (BCs)

- Authorized Agents: Only use devices and services from authorized banking agents.

- KYC Compliance: Ensure all operator KYC documents are submitted and verified by the acquiring bank.

- Reporting: Promptly report any suspicious transactions or technical anomalies.

Role of AEPS Service Providers in India for Aeps Banking

Aeps india is an AEPS service providers in India are crucial intermediaries, bridging the gap between banks and citizens by enabling secure, cardless, and PIN-less banking transactions via Aadhaar authentication. They empower local agents to operate as “mini-banks,” providing cash withdrawals, deposits, balance inquiries, and direct benefit transfers (DBT) to rural/underserved populations, thereby driving financial inclusion.

Key roles and functions of AEPS service providers include:

- Technology & Platform Provision: They provide the necessary, secure Aeps API, Aeps admin software, and infrastructure that enable agents to conduct transactions.

- Agent Network Management: They recruit, train, and manage Business Correspondents (agents/retailers), often equipping them with biometric devices.

- Financial Inclusion Drivers: By enabling local kirana stores or shops to act as banking points, they facilitate access to banking in remote, underbanked, or rural areas.

- Facilitating Basic Banking: They allow users to perform essential services, including cash withdrawal, cash deposit, balance enquiry, and mini statements.

- Interoperability & Security: They ensure seamless transactions across different banks, adhering to safety guidelines using biometric (fingerprint/iris) authentication to prevent fraud.

- Government Scheme Support: They facilitate the distribution of government-provided benefits, such as pensions and NREGA wages.

By transforming small retail shops into financial hubs, these Aeps india enhance customer convenience, offering a 24/7, low-cost setup for essential, secure banking.

How to Choose the Best AEPS banking Service Provider in India

Aeps india is the best AEPS service provider in India requires prioritizing security, high transaction success rates (98%+), and fast, same-day settlement (T+0/T+1) to maintain cash flow. Look for NPCI/RBI-compliant Aeps platforms offering competitive Aeps commission structures (e.g., ₹5-₹15 per transaction) and 24/7 technical support. Key factors include user-friendly interfaces, multi-bank support, and additional services like Mini ATM or BBPS.

Key Factors to Evaluate When Choosing an AEPS Provider

- Commission Structure: Look for competitive, transparent commission structures, such as Aeps india ₹12–₹15 per transaction. Higher, consistent commissions ensure better daily earnings for retailers.

- Transaction Success Rate: Select a Aeps india with a proven, high success rate (98% or higher) to avoid failed transactions and maintain customer trust.

- Settlement Speed: Ensure the Aeps india offers instant or same-day, 24/7, 365-day settlement to prevent blocking your working capital.

- Platform Reliability & Security: The Aeps india must be NPCI/RBI certified. Test the app or web portal for low downtime and high transaction success rates (ideally 98% or higher).

- Platform Stability: The Aeps admin portal or app should be user-friendly, stable, and have low downtime.

- Customer Support & Service: 24/7, responsive, and reliable technical support is crucial to resolve failed transactions and minimize business losses.

- Onboarding Fees: Check if the Aeps india offers a free or low cost AEPS ID, particularly useful for new retailers in rural or semi-urban areas.

- Security and Authorization: Ensure the Aeps india is authorized by the National Payments Corporation of India (NPCI) and adheres to RBI guidelines for safe, encrypted data handling.

- Additional Services: The best Aeps platforms offer a “one-stop shop” with additional services like Mini ATM, Money Transfer (DMT), Bharat Bill Payment System (BBPS), and recharges to maximize income streams.

- Ease of Use: Choose a user friendly Aeps app with easy onboarding (KYC) and real-time transaction reports.

Why Choose Aeps india for AEPS Banking Solutions

Aeps india is the right Aeps provider for AEPS banking solutions is crucial for ensuring secure, fast, and compliant financial services that can turn a local retail shop into a “mini-bank”. Aeps india offers the necessary technology, including mobile apps, web portals, and Aeps biometric device integration, to facilitate cash withdrawals, deposits, balance inquiries, and fund transfers.

Here is why you should choose a Aeps india for AEPS banking solution:

1. High Success Rates and Reliability

- Minimal Downtime: Aeps india ensure 98%+ transaction success rates, which is vital for building customer trust in rural and underserved areas where AEPS is often the only banking access.

- Real-time Processing: Transactions are processed immediately, with real-time, 24/7, or daily settlement of funds to the agent’s account.

2. Security and Regulatory Compliance

- NPCI/RBI Certified: Aeps india ensures that all transactions are compliant with National Payments Corporation of India (NPCI) and Reserve Bank of India (RBI) guidelines.

- Data Protection: Aeps india provide secure, encrypted Aeps platform and utilize biometric authentication (fingerprint/iris) to prevent fraud.

- No Data Storage: In accordance with UIDAI guidelines, Aesp india do not store sensitive biometric data on their servers.

3. Increased Revenue and Business Growth

- Attractive Commissions: Aeps india offer competitive commission structures (e.g., up to ₹13 or more per transaction) that generate a steady, daily income stream for agents.

- Increased Footfall: Offering banking services attracts more customers to retail shops, potentially leading to increased sales of primary products.

- Low Setup Costs: The entry cost is minimal, requiring only a smartphone/computer, internet connection, and a biometric device.

4. Comprehensive Services (One-Stop Shop)

- Beyond Banking: Aeps india often bundle AEPS with other services such as:

- Micro ATM: Full ATM functionality.

- Domestic Money Transfer (DMT): Sending money to any bank account.

- Utility Bill Payments (BBPS): Electricity, gas, water, and insurance payments.

- Mobile/DTH Recharge.

- Direct Benefit Transfer (DBT): Facilitating government subsidies.

5. Support and Technical Training

- 24/7 Customer Support: Responsive technical support is provided to resolve failed transactions or technical glitches immediately.

- Training & Onboarding: Aeps india offer training on how to use the biometric device, the Aeps app, and how to manage transactions securely.

- White-Label Solutions: For fintech startups, Aeps india can offer white label Aeps solutions, allowing you to run Aeps business under your own brand.

By choosing a Aeps india, agents can transform their businesses into essential financial hubs while providing safe, convenient banking to the unbanked population.

Future Trends AEPS Banking

The Future Trends for Aadhaar Enabled Payment System (AEPS) in 2026 are focused on enhanced security, regulatory compliance, and deeper integration into the rural financial ecosystem, with transaction volumes expected to exceed 3.5 billion annually.

Here are the key future trends in AEPS banking:

1. Advanced Security and Fraud Prevention

- Mandatory Liveness Detection & AI: To combat rising spoofing and synthetic ID frauds, AI-driven liveness detection is mandatory to ensure the user is physically present.

- Multi-Modal Biometrics: The industry is moving beyond single-fingerprint scans to incorporate face and iris recognition for stronger 2FA (Two-Factor Authentication).

- AI/ML Fraud Analytics: Real-time analysis of transaction patterns will be used to detect and block suspicious, high-velocity transactions.

- Secure L1 Devices: Mandatory migration to Level 1 (L1) certified biometric devices to replace older, vulnerable L0 devices.

2. Strict Regulatory Compliance (Jan 1, 2026 Rules)

- One Operator, One Bank: To prevent misuse, each AEPS operator (agent) can only be linked to a single acquiring bank.

- Mandatory Re-KYC: Agents inactive for three consecutive months must undergo a fresh, mandatory KYC process.

- Rigorous Onboarding: Banks must conduct thorough background checks on all Touchpoint Operators (ATOs) before onboarding.

3. Transformation into Comprehensive Rural Financial Hubs

- Beyond Cash Withdrawal: AEPS agents (nanopreneurs/Kirana stores) are evolving into full-service, one-stop financial hubs offering micro-loans, insurance, and investment products in addition to cash services.

- Integration with UPI & Wallets: Deeper integration with UPI and digital wallets is creating a more connected ecosystem.

- Embedded Finance: AEPS functions are being embedded into non-financial applications, making banking services more accessible.

4. Technological Advancements & Efficiency

- Blockchain for Transparency: Exploration of blockchain technology is underway to ensure immutable, transparent transaction records.

- API-First & Cloud-Based: Easier integration via secure, robust Aeps API (Application Programming Interfaces) for fintech platforms to scale efficiently.

- Mobile-First Design: Enhanced, user friendly Aeps mobile interfaces designed for rural agents with lower digital literacy.

5. Increased Adoption and Reach

- Women-Led Financial Inclusion: Growth of “Banking Sakhis” and women business correspondents to deliver last-mile banking services.

- Micro-ATM Expansion: The agent network is expected to cross 1.9 million by 2026, driven by high demand in Tier-3 and below towns.

6. New Business Models

- AEPS-Powered Lending: Fintechs are leveraging AEPS transaction history (subsidy inflows, withdrawal patterns) as alternative data for credit scoring to provide loans to small merchants.

These trends indicate that by 2026, AEPS will act as the “UPI for rural India,” transitioning from a mere cash-out tool to a comprehensive, secure identity-based payment framework.

Conclusion

AEPS banking has become one of the most trusted and simple ways to deliver basic banking services across India. With the Aadhaar Enabled Payment System, customers can easily access cash withdrawal, balance enquiry, and mini statement services without a debit card or internet banking. This makes AEPS banking especially valuable in rural and semi-urban areas, where access to traditional banking is limited.

Aadhaar Enabled Payment System (AEPS) is a National Payments Corporation of India (NPCI)-developed model that allows bank customers to perform basic financial transactions (cash withdrawal, deposit, balance check, Mini Statement) using only their Aadhaar number and biometric authentication (fingerprint or iris scan) at a Business Correspondent (BC) or micro-ATM.

For retailers, CSPs, and fintech businesses, AEPS banking offers a strong opportunity to earn daily commission income while helping customers with essential financial services. A secure and reliable AEPS platform ensures fast transactions, high success rates, and full RBI and NPCI compliance, which builds long-term customer trust.

With AEPS India, businesses get a secure, NPCI-compliant best AEPS platform that ensures smooth transactions, high success rates, and strong customer trust. A well-managed AEPS banking setup helps retailers grow their business, serve more customers, and earn stable commissions every day.

As digital payments continue to grow, AEPS banking services in India will remain an important part of the fintech ecosystem. Choosing the right AEPS solution provider, completing proper KYC, and focusing on secure operations will help businesses succeed and scale faster in the long run.

As India continues to move towards a cashless and digitally connected economy, AEPS banking will play a key role in financial inclusion and digital empowerment. Understanding AEPS fully helps customers and businesses make better use of this system and benefit from safe, fast, and Aadhaar-based banking services across the country.

By choosing a trusted Aeps provider like Aeps India, businesses can start AEPS banking quickly with easy onboarding, strong security, and continuous technical support. In conclusion, AEPS banking in India is not just a service it is a growing business opportunity that supports financial inclusion, customer convenience, and sustainable income for businesses.

If you want to start AEPS banking services in India or need a trusted AEPS service provider, contact us today Aeps india to get secure AEPS solution, fast onboarding, and reliable support for your business.

Frequently Asked Questions – Complete Guide to AEPS Banking in India | Aeps India

AEPS banking is a digital payment system that allows users to access banking services using their Aadhaar number and biometric authentication. It enables cash withdrawal, balance enquiry, mini statement, and Aadhaar-to-Aadhaar fund transfer without the need for a debit card.

Retailers, businesses, fintech companies, and common customers can use AEPS banking. It is especially useful in rural and semi-urban areas where ATMs and bank branches are limited.

Customers authenticate their identity using Aadhaar and fingerprint verification at an AEPS-enabled terminal. Once verified, transactions like cash withdrawal, balance check, mini statement, or fund transfer are processed securely and instantly.

AEPS banking helps businesses:

Earn daily commissions on transactions

Expand services to rural and semi-urban areas

Offer secure, RBI-compliant banking services

Increase customer trust and retention

Cash withdrawal from bank accounts

Balance inquiry

Mini statements

Interbank fund transfers

Retailers can partner with AEPS India to get a secure AEPS platform, complete KYC, integrate it into their system, and start offering real-time banking services to their customers.

Yes, AEPS transactions require a biometric device and an AEPS enabled software platform to authenticate customers securely.

Partner with a trusted AEPS solution provider like Aeps India to get white-label AEPS software, Aeps device setup, and full onboarding support, ensuring smooth integration and high transaction success rates.

Yes. AEPS banking is RBI and NPCI-compliant, using biometric verification and encryption to ensure all transactions are safe and fraud-proof.

Absolutely. Aeps India provides Aeps API integrate and white label Aeps solution so businesses can seamlessly offer AEPS banking services under their own brand.

Businesses must complete AEPS KYC, which includes submitting proof of identity, business details, and bank account information. This ensures compliance and secure transactions.

Yes. AEPS allows instant fund transfers between bank accounts using Aadhaar authentication, making it safe and fast for businesses and customers.

Absolutely. AEPS uses biometric authentication, Aadhaar-based verification, and bank-grade security protocols to protect every transaction.

Businesses can register with trusted AEPS service providers in India like Aeps india to start offering AEPS transactions. Choosing a reliable provider ensures easy onboarding, compliance, and technical support.

Yes. AEPS banking works using biometric devices or fingerprint scanners, so customers don’t need a smartphone or debit card to transact.

Retailers earn a small percentage per transaction, which varies based on the service type cash withdrawal, balance inquiry, or fund transfer providing a steady daily income.

Businesses need an AEPS-enabled device with biometric scanner to process transactions securely.

AEPS transactions are real-time, usually processed in a few seconds.

Yes, the platform supports multiple agents, distributors, and daily transaction management, making it ideal for growing digital banking services.

Aeps India offers a secure, reliable, and easy-to-integrate AEPS platform for retailers, agents, and fintech businesses with strong customer support.

Trusted AEPS Provider in 2026: Features, Benefits & Business Opportunities

Reliable AEPS Software: Complete Guide 2026