AEPS ID: Complete Guide for Retailers and Business in India

If you want to start AEPS services in India, the first and most important step is getting an AEPS ID. Many retailers, shop owners, and fintech entrepreneurs search for how to get AEPS ID, AEPS ID registration, and best AEPS provider in India to begin their digital banking journey. With the growing demand for Aadhaar-based banking services, having an active AEPS ID can help retailers offer essential financial services and earn Aeps commission on every transaction.

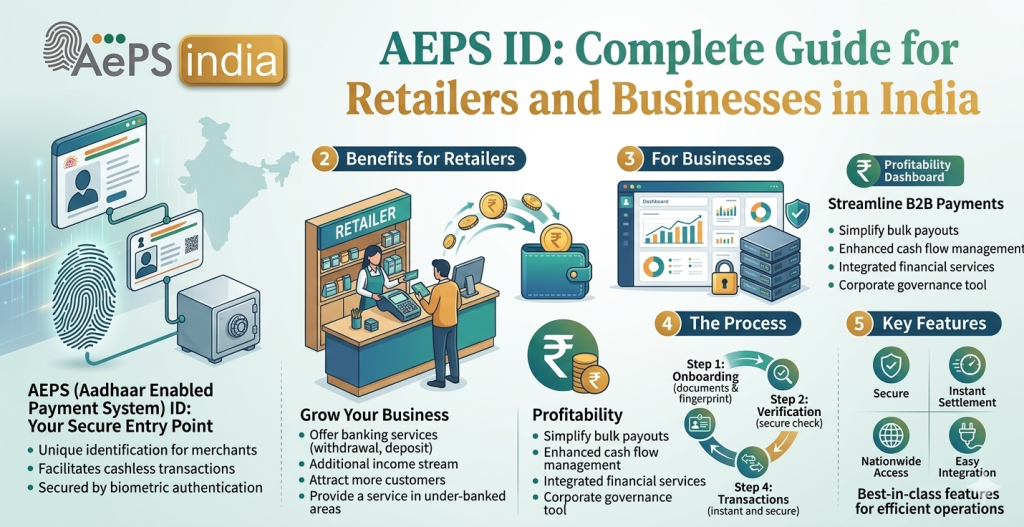

An AEPS ID (Aadhaar Enabled Payment System ID) allows retailers or agents to provide banking services such as cash withdrawal, balance enquiry, mini statement, and Aadhaar-based money transfer using biometric authentication. Customers only need their Aadhaar number and fingerprint to complete secure transactions. This system makes banking services easily accessible especially in rural and semi-urban areas.

An AEPS ID is a unique identifier provided to authorized agents or Business Correspondents (BC) by banks or fintech service providers to access the Aadhaar Enabled Payment System (AEPS). It enables them to process secure, biometric-based banking transactions such as cash withdrawals, deposits, and balance inquiries for customers at local, convenient locations.

The best AePS ID in India for 2026, offering high commissions reliability and ease of use for retailers, include Aeps india (high commission up to ₹15), Noble web studio (free Aeps registration, high Aeps commission, large network). These Aeps india allow instant secure cash withdrawals and balance inquiries using biometric authentication.

For small businesses and digital service providers, starting AEPS service business is a great opportunity to earn extra income. Every transaction completed through the AEPS system gives retailers a commission, which helps them build a steady source of revenue while offering valuable banking services to their community.

Getting an AEPS retailer ID is simple when you partner with a trusted AEPS service provider in India like Aeps india. A good Aeps platform offers secure biometric authentication real-time transaction processing, high success rate, and a transparent commission structure. These features help retailers run AEPS services smoothly and build trust with customers.

The AEPS business model is a low-investment opportunity that allows retailers to convert their shop into a mini banking service point. As digital payments and Aadhaar-based banking continue to grow across India, having an AEPS ID for retailers can help generate regular income while providing convenient banking access to local customers.

Choosing the right Aeps platform and completing your AEPS ID registration is the first step toward building a successful digital banking service in India’s expanding fintech ecosystem.

A trusted Aeps platform like AEPS India makes it easy for retailers to get an AEPS ID for retailers and start providing secure Aadhaar based banking services. With simple registration fast transactions and reliable support businesses can quickly start their AEPS services in India and grow their digital financial service network.

As digital payments and Aadhaar-based banking services continue to expand across the country, the demand for reliable AEPS ID providers in India like Aeps india is also increasing.

In this guide, we will explain everything you need to know about AEPS ID, how it works, its benefits, and how retailers can start AEPS services easily.

What is an AEPS ID

An AEPS ID (Aadhaar Enabled Payment System ID) is a unique agent identification credential provided by banks or fintech providers to Business Correspondents (agents). It allows agents to facilitate, secure and perform biometric-authenticated banking transactions like cash withdrawals, deposits, and balance checks for customers using their Aadhaar number.

AEPS ID Work

An AEPS ID allows users to conduct banking transactions cash withdrawals, balance checks, and mini-statements using only their Aadhaar number and biometric authentication via a BC agent. It facilitates secure, cardless, and interoperable banking, particularly useful for rural areas. Agents earn commissions, often ranging from ₹7-₹10 per transaction.

Key Aspects of AEPS ID Work:

- How it Works: The customer visits an agent (business correspondent), enters their Aadhaar number, selects the bank, and provides a Aeps fingerprint/Aeps iris scan on a Micro ATM software solution

or smartphone. - Services Offered: Cash withdrawal, cash deposit, balance enquiry, and mini-statement.

- Requirements for Agents: To get AEPS ID, you typically need an Aadhaar card, PAN card, bank account, and a registered mobile number.

- Benefits for Agents: Agents earn Aeps commissions from Aeps india, with potential earnings of up to ₹13 or more on higher-value transactions (e.g., ₹3000+).

- Security: As transactions are validated via biometric data (fingerprint or iris), it is highly secure and reduces fraud risks.

- Interoperability: A customer can use their Aadhaar to transact at any bank’s, or any agent’s, micro-ATM/terminal.

Services Available with an AEPS ID

An AEPS ID allows individuals, particularly in rural or remote areas, to access essential Aeps banking services without needing a debit card, credit card or smartphone, relying instead on Aadhaar authentication. The Aeps system is interoperable, meaning a customer can use any bank’s Business Correspondent (BC) agent to access their specific bank account.

Here are the key services available with an AEPS ID:

1. Core Banking Services

- Cash Withdrawal: Customers can withdraw cash directly from their bank account at a local shop or ATM-cum-micro ATM device, typically up to ₹10,000 per transaction.

- Cash Deposit: Funds can be deposited into an Aadhaar-linked account at a BC point.

- Balance Enquiry: Instant checking of the available bank balance.

- Mini Statement: A summary of the last few transactions can be generated.

2. Fund Transfer Services

- Aadhaar-to-Aadhaar Fund Transfer: Secure transfer of money from one Aadhaar-linked account to another Aadhaar-linked account without needing account numbers or IFSC codes.

3. Merchant Payments (Aadhaar Pay)

- BHIM Aadhaar Pay: Allows merchants to accept payments from customers for goods and services using their Aadhaar number and biometric authentication, with daily limits often up to ₹50,000.

4. Government Schemes & Other Services

- Direct Benefit Transfer (DBT): Facilitates the withdrawal of government subsidies, pensions and NREGA wages directly into bank accounts.

- e-KYC: Used for electronic customer verification without submitting physical documents.

- Best Finger Detection: A system to authenticate the best fingerprint to reduce transaction failures.

Read Blog : Best AEPS Service Solution Provider in India: Complete Guide

Documents Required to Get an AEPS ID

To get Aadhaar Enabled Payment System ID for agent registration, you primarily need your Aadhaar card, PAN card, bank account details (cancelled cheque/passbook), and a mobile number linked to your Aadhaar. Additional requirements include a recent passport-sized photo, business/shop address proof, an active email, and a STQC Aeps certified biometric device.

Mandatory Documents for AEPS Agent Registration:

- Aadhaar Card: Must be linked to your mobile number and bank account.

- PAN Card: Mandatory for identity verification.

- Bank Account Details: A cancelled cheque, passbook, or bank statement of your personal or business account.

- Passport-sized Photograph: Recent photo with a neutral background.

- Registered Mobile Number: Active number linked to Aadhaar for OTP verification.

- Proof of Address/Business: Utility bill (electricity/water), rent agreement shop act license or Udyam registration.

- Email Address: For communication and registration.

Essential Hardware & Technical Requirements:

- Biometric Device: A STQC-certified Aeps fingerprint scanner (e.g., Mantra) or iris scanner.

- Smartphone/Computer: An Android phone or laptop with internet access.

Key Requirements to Get an AEPS ID (Agent):

- Age & Nationality: 18+ years old and an Indian citizen.

- Documentation: Valid Aadhaar card and PAN card.

- Banking: A personal bank account to settle transactions.

- Hardware: A smartphone/PC and a registered Aeps biometric device (fingerprint/iris scanner).

- Registration: Must register with an authorized Aeps India.

Note on User Requirements:

- Customers do not need an Aeps ID. They only need an Aadhaar-linked bank account and their fingerprint/iris for authentication at an agent’s terminal.

The Aeps registration process is generally paperless and includes eKYC using Aeps fingerprint scanner. Ensure your mobile number is linked to your bank account for timely transaction alerts.

Who Needs an AEPS ID in India?

An AEPS ID is primarily needed by small business owners, retailers, kirana store owners, and banking correspondents in India who want to offer banking services like cash withdrawal, deposit and balance inquiry to customers. It acts as a tool for digital financial inclusion, allowing agents to earn commissions by turning their shops into mini-ATMs.

Who Needs an AEPS Agent ID?

- Retailers & Shop Owners: Kirana, mobile, or general store owners looking to add, “Aadhaar Banking” to their services.

- Business Correspondents (BC) / Agents: Individuals acting as representatives for banks in rural or underserved areas.

- Digital Service Providers: Individuals running Aeps india..

- Entrepreneurs: Anyone looking to start a low-cost banking business.

Why Use AEPS ID

An AEPS ID is used to provide secure, cardless, and PIN-less banking services specifically cash withdrawal, balance inquiry, and mini-statements using only biometric authentication (fingerprint/IRIS). It enables doorstep banking particularly in rural areas by connecting local agents to any bank account boosting financial inclusion and security.

Key Reasons to Use an AEPS ID:

- Financial Inclusion & Accessibility: It provides essential banking services to rural or remote, underserved areas where bank branches or ATMs are not easily accessible.

- No Card or PIN Needed: Transactions are authorized via biometrics (fingerprint scan), eliminating the need for a physical debit/credit card or a PIN, reducing the risk of fraud.

- Convenience & Speed: It enables instant, real-time, 24/7 banking transactions (cash withdrawal, deposit, balance check).

- High Security: Biometric authentication is unique to the user making transactions highly secure compared to traditional password-based systems.

- Interoperability: The system allows customers of any bank to conduct transactions at any AePS-enabled terminal or micro-ATM.

- For Retailers/Agents: It allows shopkeepers to turn their store into a mini-bank increasing footfall and earning commissions on transactions.

AEPS acts as a debit card for rural areas allowing users to access funds without having to travel long distances to a bank branch.

Read Blog : AEPS Service Portal: Complete Guide

Top Use Cases of AEPS ID

The Aadhaar Enabled Payment System (AEPS) has transformed local retail shops into “mini-banks” in India, offering crucial financial services to rural and underbanked populations. By linking a bank account to an Aadhaar number users can perform transactions through a biometric-based system (fingerprint or iris scan) without a debit card PIN or smartphone.

Here are the top use cases of an AEPS ID:

1. Cash Withdrawal (Micro ATM)

The most common use case is enabling customers to withdraw cash from their bank accounts at local Kirana shops or Business Correspondent (BC) outlets.

- Key Aspect: Functions as a mobile ATM at the doorstep for villagers.

- Limitation: Typically capped at ₹10,000 per transaction, with daily limits often up to ₹50,000.

2. Balance Enquiry & Mini Statements

AEPS enables instant, real-time checking of available balances and generation of the last 5–10 transactions (mini-statement). This helps users track their accounts without visiting a bank branch.

3. Cash Deposit

Customers can deposit cash directly into their Aadhaar-linked accounts at authorized retail outlets. This is particularly useful for small merchants and individuals who cannot visit a bank frequently.

4. Direct Benefit Transfer (DBT) Disbursements

The government uses AEPS to transfer subsidies, pensions, and NREGA wages directly into the beneficiaries’ accounts. Beneficiaries can then easily withdraw these funds from their local AEPS agent.

5. Aadhaar-to-Aadhaar Fund Transfer

AEPS allows for secure, direct fund transfers between two different Aadhaar-linked bank accounts. This enables peer-to-peer or peer-to-merchant transfers without needing bank account numbers or IFSC codes.

6. BHIM Aadhaar Pay (Merchant Payments)

This best Aeps service enables merchants to accept digital payments from customers through Aadhaar authentication. It serves as an alternative to POS machines and in many cases allows for higher transaction limits.

7. eKYC & Customer Authentication

AEPS allows for instant, paperless, and secure customer identity verification. This is used for opening new bank accounts, SIM activation or availing other services making the process faster and more secure.

8. Income Generation for Retailers

For shop owners, the AEPS ID offers a steady revenue stream. Retailers earn Aeps commissions often ranging from ₹2 to ₹15+ per transaction depending on the volume and value.

Key Requirements (as of 2026):

- Mandatory L1 Devices: Use of STQC-certified Aeps L1 biometric devices is required for improved security.

- One Operator, One Bank Rule: Agents are restricted to linking with one acquiring bank to reduce fraud.

- Re-KYC: Agents inactive for three months must undergo a fresh KYC process.

Key Aspects of AEPS ID

An AEPS ID allows secure, cardless banking transactions using biometric authentication (fingerprint/iris) linked to an Aadhaar number. Key aspects include instant cash withdrawal, balance enquiry, mini-statements, and interoperability across banks, promoting financial inclusion, especially in rural areas. It requires bank-linked Aadhaar and offers high security.

Core Aspects of AEPS

- Biometric Authentication: Transactions are verified using unique fingerprints or iris scans, eliminating the need for PINs or debit cards.

- Interoperability: Users can access services at any AEPS enabled micro ATM or banking correspondent regardless of their specific bank.

- Essential Banking Services: Facilitates cash withdrawal deposit, balance enquiry and mini-statements.

- Security & Safety: Transactions are secure as they require biometric validation reducing fraud.

- Direct Benefit Transfer (DBT): Facilitates the direct transfer of government subsidies into Aadhaar-linked bank accounts.

- No Physical Card/PIN: Replaces the need for a physical ATM card and PIN, making it ideal for rural or less tech-savvy users.

- Real-time Validation: Identifies users instantly via the UIDAI database.

Requirements for AEPS Access

- Aadhaar Linking: The user’s bank account must be linked to their 12-digit Aadhaar number.

- Agent Registration: To operate as an AEPS agent, one must be at least 18, possess a PAN card, an Aadhaar card, a functional bank account, and a smartphone.

- Security Measures: Always ensure the AEPS software and mobile operating systems are updated to maintain data security.

Why Get an AEPS ID?

Getting AEPS ID enables shopkeepers and agents to provide essential card-less banking services like cash withdrawals, deposits and balance inquiries using just biometrics. It increases customer footfall, builds trust, and generates commissions on transactions making it a lucrative secure and easy-to-use business tool.

Key Reasons to Get an AEPS ID:

- Earn Commissions: Aeps india allow you to earn Aeps commissions for every cash deposit, withdrawal, or balance inquiry.

- Customer Convenience: You can turn your shop into a local “Micro-ATM,” allowing customers to avoid traveling long distances to bank branches.

- No Card or PIN Needed: Transactions are completed using only Aadhaar authentication and a biometric scanner, which is ideal for rural areas.

- High Security: Biometric authentication reduces fraud risks making it a safe method for both agents and customers.

- Interoperability: You can serve customers from any bank, as the system works across all banks that are part of the NPCI network.

- Service Diversification: Beyond cash, you can offer mini-statements and support for Government Direct Benefit Transfers (DBT).

Read Blog : Complete AEPS Setup Guide for Retailers in India

Why AEPS ID Services Are Growing in India

AEPS ID services are rapidly growing in India due to their critical role in driving rural financial inclusion, allowing doorstep banking (cash withdrawal/deposit) via biometrics without needing cards or PINs. It is driven by the need for Direct Benefit Transfers (DBT), high security, and 24/7 interoperability, enabling local retailers to act as mini-banks.

Key Drivers for the Growth of AEPS in India:

- Financial Inclusion & Accessibility: AEPS bridges the urban-rural divide bringing banking services to remote areas with limited ATMs or bank branches.

- Ease of Use & Biometric Security: Transactions require only an Aadhaar number and fingerprint/iris scan, making it accessible to non-tech-savvy users while reducing fraud risks.

- Direct Benefit Transfer (DBT) Access: It facilitates the easy withdrawal of government subsidies, pensions, and welfare payments directly at local shops.

- Business Opportunity for Retailers: Local shopkeepers can become business correspondents (BCs), increasing foot traffic to their stores (15–20% increase) and earning Aeps commissions on transactions.

- Interoperability: Customers can access their bank account through any AEPS enabled device, regardless of the bank ensuring convenience.

- Low Investment & High ROI: Retailers only need a smartphone and a Aeps biometric scanner to start creating a low-cost high-margin business model.

- Government Support: The initiative aligns with the “Digital India” vision, promoting a cashless economy and reducing dependency on cash handling.

Role of an AEPS ID Provider for Retailers and Agents

Aeps india is an AEPS ID provider acts as a vital bridge between local retailers/agents and the NPCI network, enabling small shops to function as mini-banks. Aeps india provide secure technology, biometric device integration, and Aeps API access for services like cash withdrawals, balance inquiries and fund transfers. By partnering with an Aeps india retailers can increase footfall earn commission (approx. ₹7–₹15+ per transaction) and provide crucial banking access to rural populations.

Key Roles of an AEPS ID Provider:

- Technology & Platform Provider: They develop Aeps software and maintain secure Aeps software provider, web portals, and mobile Aeps apps that allow for real-time transactions.

- Agent Onboarding & Training: They handle the registration, Aeps KYC, and Aeps onboarding of retailers as Business Correspondents (BCs) and provide training to use the system.

- Hardware Support: Aeps india often supply or support necessary biometric devices (fingerprint or iris scanners) required for Aadhaar-based authentication.

- Transaction Processing & Security: They ensure safe and secure connectivity to the National Payments Corporation of India (NPCI) network for instant, cardless and PIN-less transactions.

- Settlement & Commission Management: They facilitate fast settlement of funds into the agent’s bank account and manage the Aeps commission structure, with earnings often ranging from ₹7–₹10 per transaction and up to ₹13–₹15 for higher value withdrawals.

- Compliance & Support: They ensure transactions follow RBI and NPCI guidelines and provide support to resolve technical issues.

Benefits to Retailers and Agents:

- Additional Revenue: Earn Aeps commission on every transaction, boosting income.

- Increased Footfall: Attract more customers, increasing sales of regular products.

- Improved Reputation: Become a trusted community hub for financial services.

- Reduced Risk: Less reliance on physical cash management.

Why Retailers Need an AEPS ID

Retailers in India, particularly in rural and semi-urban areas, need an Aadhaar Enabled Payment System (AePS) ID to transform their shops into mini-banking hubs, thereby attracting more customers, generating extra income through commissions and enhancing community trust. The system allows shopkeepers to offer essential banking services such as cash withdrawals, balance inquiries and mini-statements using only a customer’s Aadhaar number and fingerprint eliminating the need for debit cards or PINs.

Here is why retailers need an AePS ID:

1. New Revenue Stream (Commission Income)

- Earn Per Transaction: Retailers earn Aeps commission on every successful AePS transaction, such as cash withdrawals, balance checks or mini-statements.

- High Earning Potential: High volume Aeps retailers can earn a significant monthly income, with potential earnings of up to ₹15 or more per transaction especially for cash withdrawals between ₹3,000–₹10,000.

2. Increased Footfall and Business Growth

- Attract New Customers: Aeps india offering Aeps banking service attracts customers who may not have easy access to bank branches or ATMs, increasing the number of people visiting the shop.

- Cross-Selling Opportunities: Customers who come for banking services often make impulse purchases such as buying groceries or other items boosting the retailer’s primary business.

3. Reduced Cash Handling and Operational Efficiency

- Cash Recycling: Retailers can use the cash from their daily sales to fulfill withdrawal requests, reducing the need to frequently travel to a bank to deposit cash, which improves security.

- Digital Records: Every transaction is recorded digitally, which simplifies accounting and reduces the risks of manual errors.

4. Build Community Trust and Loyalty

- Become a Trusted Hub: By providing crucial services to the community, retailers build strong, trusted relationships with residents, making their shop a go-to location.

- Assisted Banking: It helps the elderly and those with low digital literacy easily manage their funds.

5. Secure and Compliant Transactions

- Biometric Security: AePS transactions are safe because they require the customer’s unique fingerprint, which prevents fraud and card skimming.

- Government-Regulated: The system is overseen by the National Payments Corporation of India (NPCI) and the Reserve Bank of India (RBI), ensuring a secure, standard-driven environment.

Summary Table: Benefits for Retailers

| Feature | Benefit |

|---|---|

| Additional Income | Commissions on every withdrawal/inquiry (up to ₹15+ per transaction) |

| Increased Traffic | Higher footfall leads to 15-20% more sales of regular products |

| Safety | Reduced need to keep large amounts of cash on hand |

| Community Impact | Bridges the banking gap in rural/remote areas |

| No Card Needed | Attracts customers who lack debit cards or PINs |

To buy AePS ID a retailer must be a legitimate business owner (e.g., kirana store, pharmacy) and apply through an authorized Aeps india by completing a simple KYC process.

Read Blog : Start AEPS Service in India and Earn High Commission

AEPS ID Important for Retailers and Business

An Aadhaar Enabled Payment System ID is highly important for retailers and businesses in India, particularly for those in rural or semi-urban areas. Aeps india enables them to transform their shops into mini-banks by providing essential banking services like cash withdrawals, balance inquiries and mini-statements using only a customer’s Aadhaar number and fingerprint, reducing reliance on physical debit cards and PINs.

Key Benefits of Having an AePS ID for Businesses:

- Additional Revenue Stream: Retailers earn Aeps commission on every successful transaction, with potential earnings of ₹10,000 to ₹30,000+ monthly, particularly high (up to ₹15+) on transactions between ₹3,000–₹10,000.

- Increased Customer Footfall: Aeps india providing Aeps banking services retailers attract more customers including those who may not be regular shoppers leading to increased impulse purchases and improved overall sales.

- Reduced Cash Handling Risk: Retailers can use the cash received from daily sales to fulfill customer cash withdrawal requests, reducing the need to carry cash to the bank thus lowering theft risk.

- Enhanced Trust and Reputation: As a government-backed (NPCI) and secure, biometric-based system, offering AePS builds credibility and makes the local shop a trusted community pillar.

- Financial Inclusion: Retailers help bridge the banking gap in underserved, rural areas allowing customers to access their money or Direct Benefit Transfers (DBT) near their homes.

Important Considerations for Retailers:

- Inactivity Rule: If an agent is inactive for three months, a fresh KYC process is mandatory.

- Security: Never store customer biometric data or Aadhaar numbers locally on the device.

- Settlement: Aeps platforms offer T+0 (instant) or T+1 (next day) settlement to maintain cash flow.

Features AEPS ID

An AePS ID allows banking correspondents to facilitate secure, cardless transactions using biometric authentication (fingerprint/iris) linked to a user’s Aadhaar. Key features include 24/7 cash withdrawals, deposits, balance inquiries, and mini-statements at micro-ATMs. It is highly secure interoperable across banks and promotes financial inclusion.

Key Features of an AEPS ID:

- Secure Biometric Authentication: Uses unique fingerprints or iris scans, eliminating the need for PINs, passwords, or cards.

- Core Banking Services: Provides essential best Aeps service like cash withdrawal, cash deposit, balance inquiry, and mini-statement generation.

- Interoperability: Customers can access their Aadhaar-linked account at any bank’s micro-ATM or agent outlet regardless of their home bank.

- Cardless & PINless: Transactions require only the Aadhaar number and biometric verification, ideal for rural and remote areas.

- Fund Transfers: Facilitates instant money transfers between Aadhaar-linked accounts.

- Real-Time Settlement: Agents often receive instant settlement of funds into their wallet along with immediate commission crediting.

- Instant Onboarding: Quick, paperless KYC process (KYC) to activate Aeps ID using PAN, Aadhaar, and bank details.

- High Accessibility & Inclusivity: Ideal for rural areas providing access to banking without smartphones or internet access.

- Secure & Always On: High-security authentication via UIDAI Aeps certified devices, available 24/7.

- Direct Benefit Transfer (DBT): Facilitates access to government schemes such as pensions and MNREGA at the user’s doorstep.

- Agent Benefits: Retailers/agents can earn Aeps commissions on transactions (up to ₹13 or more) and manage cash flow by recycling it.

Benefits for Agents/Retailers

- High Commissions: Retailers earn Aeps commissions per transaction, often between ₹2 to ₹15.

- Low Investment: Requires only a smartphone/PC internet and a Buy Aeps biometric device.

- Instant Settlements: Aeps india allow quick or instant Aeps commission settlement to the agent’s wallet.

Benefits AEPS ID

An AEPS ID allows merchants and agents to offer banking services cash withdrawal, balance inquiry, and mini-statements using only biometric authentication, eliminating the need for debit cards or PINs. Key benefits include earning Aeps commissions per transaction, increased footfall, secure transactions and promoting financial inclusion.

Key Benefits of AEPS ID for Agents/Retailers:

- Generate Extra Income: Earn commission on every transaction (cash withdrawal, balance inquiry, mini-statement).

- Increased Footfall & Sales: Turning your shop into a “mini-bank” attracts more customers, enhancing local sales.

- Reduced Cash Management Risk: Utilize cash from daily sales to fulfill customer withdrawals, reducing the need to transport cash to banks.

- Instant Activation & Services: Provides on-the-spot, real-time transaction processing.

- Easy Setup & Operation: Requires only a smartphone/computer an internet connection and a Purchase Aeps biometric device (fingerprint scanner).

Key Benefits for Customers (Via Agents):

- Doorstep Banking: Access essential services without visiting a bank branch or ATM.

- Cardless & PINless: Transactions are secured using only Aadhaar numbers and biometric (fingerprint/iris) authentication.

- Direct Benefit Transfer (DBT): Facilitates safe and direct receipt of government subsidies and pensions.

- Interoperability: Customers can access any Aadhaar-linked bank account at any AEPS-enabled agent location.

- Convenience for Customers: Easy access to cash withdrawals, deposits, and fund transfers.

- Rural Accessibility: Crucial for reaching remote areas with limited banking infrastructure.

- Safe Transactions: Biometric authentication provides high-security against fraud and theft.

AEPS ID are commonly offered by best Aeps platforms and banks to business correspondents (bank mitras) looking to digitize their services and increase revenue.

Read Blog : Best AEPS Portal in India for Retailers – Complete Guide

How to Get an AEPS ID in India

To apply an AEPS ID, choose an NPCI-authorizedAeps india, submit KYC documents (Aadhaar, PAN, bank details), and pass biometric verification. Upon approval (usually 24-48 hours), install the Aeps app, connect a Aeps certified biometric device and start processing transactions.

Steps to Obtain an AEPS ID:

- Choose an Authorized AEPS Service Provider: Select a reputable NPCI-approved Aeps india.

- Fill Out the Application/Registration Form: Visit the Aeps india website or Aeps b2b app and enter personal details (Name, Address, Mobile Number) and business information.

- Complete KYC Verification: Submit required documents: Aadhaar card, PAN card, passport-sized photo, and bank account details (cancelled cheque/passbook).

- Aadhaar card (linked with a mobile number).

- PAN card.

- Bank account details (cancelled cheque/passbook).

- Proof of business/shop address.

- Complete Biometric Verification: A representative may visit, or you will use a fingerprint/iris scanner to complete digital real-time biometric KYC to verify your identity against Aadhaar records.

- Activation and Approval: The Aeps india verifies documents (1-2 days). Once approved, your Merchant ID (MID) or Agent ID activated.

- Set Up Hardware and Software: Purchase Aeps certified L1 or L2 biometric device, install the Registered Device (RD) Aeps service software on your smartphone or PC and log in to the Aeps portal.

Important Tips

- Eligibility: Must be 18+ years old, possess a valid PAN/Aadhaar, and have a bank account.

- Costs: While Aeps b2b platforms offer free registration, others may charge for kit, training, or device.

- Commission: You earn Aeps commissions on cash withdrawals balance inquiries, and mini statements.

AEPS ID Commission Structure and Earning Potential

AEPS ID allow retailers to earn commissions ranging from ₹2 to ₹15+ per transaction, typically yielding ₹10,000–₹30,000+ in monthly income through high-volume cash withdrawals. Maximum earnings (₹13–₹15+) are achieved on transactions between ₹3,000–₹10,000, with additional income from balance inquiries and mini-statements.

AEPS Commission Structure (2026 Retailer Level)

Aeps Commissions are tiered based on the transaction amount with higher withdrawal amounts generating higher earnings.

- ₹100 – ₹999: ~₹2.00 per transaction

- ₹1,000 – ₹1,499: ~₹3.00 per transaction

- ₹1,500 – ₹1,999: ~₹4.50 per transaction

- ₹2,000 – ₹2,499: ~₹5.50 per transaction

- ₹2,500 – ₹2,999: ₹5 – ₹7 per transaction

- ₹3,000 – ₹10,000: ₹13 – ₹15+ per transaction (Highest slab)

- Balance Inquiry/Mini Statement: ~₹0.50 – ₹5 per transaction

Earning Potential

An active Aeps agent with a high-volume, rural-based or high-traffic location can generate significant monthly income.

- Monthly Earning Scenario: If a retailer averages 50 transactions a day at a ₹15 commission rate, the monthly income could be roughly ₹22,500 (

50×₹15×30 days).

50×₹15×30 days). - Total Income Boost: Combining AEPS with other services like Domestic Money Transfer service (DMT) and BBPS Service can raise total monthly earnings to ₹45,000–₹60,000.

Key Factors for High Earnings

- High-Value Transactions: Focus on withdrawals between ₹3,000–₹10,000 for maximum commission slabs.

- Settlement Choice: Retailers can choose between instant (T+0) or next-day (T+1) settlement to manage cash flow.

- Setup Requirements: A smartphone/computer, internet connection, and an L1 Aeps certified biometric fingerprint scanner are required.

- Top Providers: Aeps India and Noble web studio offer competitive Aeps rates.

Common 2026 Commission Structure Examples

- Aeps India: Up to ₹15 commission for Super Prime Retailers.

- Noble web studio: ₹2 for transactions between ₹100–₹999.

Aeps ID Cost Structure

AEPS ID cost structure involves low upfront Aeps agent registration fees (often ₹0–₹3,000), and potential, though declining transaction charges of ₹5–₹20 per withdrawal. Retailers earn commissions of ₹10–₹15+ per transaction, while full white label Aeps, best Aeps API, or Aeps portal setup for businesses ranges from ₹12,000 to over ₹1 lakh.

Key Cost Breakdown for AEPS ID and Services (2026):

- Retailer/Agent Registration (ID Cost): Often free to ₹1,250 for basic activation. Some premium Aeps ID might cost up to ₹3,000.

- Hardware Costs: A certified Aeps biometric scanner (e.g., Mantra) is necessary, costing approximately ₹1,500–₹3,000.

- Transaction Charges (Customer/Agent): While some banks offer free transactions others may charge a fee for withdrawals or mini-statements often ranging from ₹5–₹20 + 18% GST.

- Agent Commission (Income): Agents earn Aeps commissions, with high volume Aeps, high-value transactions (₹3,000–₹10,000) yielding higher income often up to ₹13–₹15+ per transaction.

Setup/API Integration (For Businesses):

- Basic/White Label Aeps Portal: ₹5,000 – ₹35,000.

- Advanced/Custom Aeps API Integration: ₹45,000 – ₹1,20,000+.

- Annual Maintenance: ₹10,000 – ₹1,00,000 per year.

Important Considerations:

- Aeps india: is highlighted for offering free AEPS ID registration.

- Hidden Fees: Look out for settlement fees when transferring funds from the wallet to a bank account.

- Factors: Aeps india generally have lower fees, and high volume Aeps agents can negotiate better commission Aeps structures.

Read Blog : BBPS Service Provider: Complete Guide for Businesses in India

How Retailers Earn Commission Using AEPS ID

Retailers earn commissions via AEPS by acting as banking agents, facilitating cash withdrawals, balance inquiries, and mini-statements for customers using biometric authentication. They earn a tiered commission, typically ₹2–₹15+ per transaction with higher amounts (₹3,000–₹10,000) yielding the maximum plus bonuses for high-volume daily or monthly transactions.

Highest AEPS commissions in 2026 reach up to ₹13–₹15+ per transaction for high-value withdrawals (₹3,000–₹10,000), offered by Aeps India and Noble Web Studio. The structure is usually tiered, with lower amounts (₹1–₹4) for smaller transactions, plus additional earnings from mini-statements (₹2–₹7) and Aadhaar Pay.

Top 2026 AEPS Commission Rates (Retailer Level)

- ₹3,000 – ₹10,000: ₹13 – ₹15+ per transaction

- ₹2,500 – ₹2,999: ₹5 – ₹7 per transaction

- ₹2,000 – ₹2,499: ~₹5.50 per transaction

- ₹1,500 – ₹1,999: ~₹4.50 per transaction

- ₹1,000 – ₹1,499: ~₹3.00 per transaction

- ₹100 – ₹999: ~₹2.00 per transaction

How Retailers Earn Commission via AEPS

- Cash Withdrawal Commission: The primary revenue source. Highest Aeps Commission are tiered based on transaction value, with higher amounts resulting in higher payouts.

- ₹100–₹999: ~₹2.00

- ₹1,000–₹1,499: ~₹3.00

- ₹3,000–₹10,000: Up to ₹13–₹15+

- Balance Inquiry & Mini-Statements: Fixed, smaller fees are earned for these services, usually ₹1–₹5 per transaction.

- Aadhaar Pay/Merchant Payments: Retailers can earn up to 1% commission on high-value transactions using Aadhaar Pay.

- Volume-Based Incentives: Additional bonuses are often awarded to agents processing high volumes (e.g., 150–200+ transactions monthly).

- Monthly Income Potential: Active agents can earn ₹10,000–₹30,000+ monthly, depending on transaction volume.

Key Features of High-Commission Providers

- High-Value Focus: Maximum earnings are locked at transactions between ₹3,000 and ₹10,000.

- Additional Revenue: Mini-statements and balance inquiries offer an extra ₹0.50 – ₹7 per check.

- Settlement: Aeps india offer instant (T+0) or next-day (T+1) settlement.

- Incentives: High-volume agents can earn an extra ₹2,000+ monthly.

- Top Platforms (2026): Aeps India and Noble Web Studio.

Key Requirements to Start Earning

- Registration: Register with a reputable Aeps india and complete KYC (PAN card, Aadhaar, bank details).

- Equipment: A smartphone or PC stable internet, and a registered Aeps biometric fingerprint scanner (e.g., Mantra).

- Settlement: Retailers can opt for immediate (T+0) or next-day (T+1) settlement to manage cash flow.

Tips for Maximizing Earnings

- Increase Footfall: Promote services to attract more customers enhancing overall sales.

- Cross-Sell Services: Combine AEPS with other services like Domestic Money Transfer API service (DMT), BBPS Api Service, and mobile recharges.

- Maintain Adequate Cash: Ensure sufficient cash is available to handle high-value withdrawals.

Biometric Device Requirements for AEPS ID

To obtain an AePS ID, you must use a Standardisation Testing and Quality Certification (STQC) certified biometric device that supports Registered Device (RD) service. The scanner typically a finger or iris scanner, must be compatible with Android or Windows costing between ₹1,500–₹5,000. Common devices include Mantra.

Key Requirements for AePS Biometric Devices:

- Mandatory Certification: Must be STQC certified and UIDAI-registered.

- RD Service Support: The device must support Registered Device (RD) services to ensure secure, encrypted biometric data transmission.

- Device Type: Fingerprint scanners are the most common; iris scanners are also acceptable.

- Compatibility: The device must be compatible with your smartphone (Android) or computer’s OS.

- Connectivity: USB or Bluetooth connectivity for mobile/desktop use.

Security and UIDAI Compliance in AEPS ID

The Aadhaar Enabled Payment System (AePS) is a secure, bank-led model that allows financial transactions (cash withdrawal, balance inquiry, etc.) using Aadhaar authentication at Micro-ATMs or Business Correspondent (BC) locations. Security is built on biometric authentication (fingerprint or iris scan), which is matched in real-time with the Unique Identification Authority of India (UIDAI) database.

1. Mandatory UIDAI Compliance for Agents (BCs)

- KYC Registration: Banking Correspondents (BCs) or agents must undergo a rigorous, RBI-mandated KYC process, including Aadhaar and PAN verification, before initiating services.

- One Operator-One Bank Policy: Effective January 2026, agents must be linked to only one acquiring bank to enhance accountability.

- Inactivity Re-KYC: Agents inactive for three consecutive months must undergo a fresh KYC process before resuming services.

- Certified Devices: Only STQC (Standardisation Testing and Quality Certification) certified biometric devices (fingerprint/iris scanner) with active Registered Device (RD) services are permitted to prevent tampering.

2. Security Features in Transactions

- Biometric Authentication: The primary security layer where the user’s fingerprint or iris scan matches against the UIDAI database, confirming identity in real-time.

- No Data Storage: To protect privacy, raw biometric data is never stored locally on agent devices or micro-ATMs. It is encrypted at the source and transmitted in secure packets.

- Liveness Detection: Technology that detects if the biometric input is from a live person, preventing spoofing using cloned fingerprints or photos.

- Data Encryption: All transaction data is encrypted during transmission, rendering it unreadable to unauthorized parties.

- Transaction Limits: NPCI caps AePS withdrawals to ₹10,000 per transaction to mitigate risk.

3. User Protection Guidelines

- Locking Biometrics: Residents can lock their biometrics (fingerprint/iris) through the UIDAI website or mAadhaar app to prevent unauthorized access, unlocking only when needed.

- Virtual ID (VID): Users are encouraged to use a 16-digit Virtual ID instead of their 12-digit Aadhaar number for added privacy.

- Real-time Alerts: Enrolling for SMS alerts with the bank ensures immediate notification of any fraudulent activity.

4. Security Risks and Countermeasures

- Dishonest Agents: Agents might attempt to misuse data. Strict compliance and using authorized BCs reduce this risk.

- Phishing Attempts: Users should never share their Aadhaar number or biometric details on suspicious sites or over the phone.

- Penalty for Violations: Unauthorized access to the Central Identities Data Repository (CIDR) or tampering with data is a punishable offense under the Aadhaar Act 2016, leading to imprisonment of up to 10 years and heavy fines.

AePS transactions are designed with multi-layered security ranging from real-time biometric verification to advanced encryption to ensure that only the rightful account holder can authorize a transaction.

Read Blog : AEPS Software Service: Complete Guide 2026

Aeps India is the Best AEPS ID Provider in India

Aeps India one of the best AEPS ID provider in India requires prioritizing safety, high transaction success rates (>98%), and, in 2026, compliance with NPCI/RBI standards, including 2FA and liveness detection. Look for instant (T+0) settlement, competitive commissions (₹5–₹15+), 24/7 support, and a stable Aeps app. Top providers include Aeps india and Noble web studio.

Key Factors to Evaluate When Choosing an AEPS Provider:

- Security & Compliance: Ensure the Aeps India is authorized by the NPCI and adheres strictly to RBI/UIDAI guidelines for biometric security.

- Transaction Success Rate & Stability: Aeps India promising high uptime (99.9%) and low failure rates to avoid “server down” issues.

- Commission Structure: Look for a transparent competitive structure, ideally offering ₹5–₹15+ per transaction depending on the volume.

- Settlement Speed: Aeps India offer instant (T+0) or same-day (T+1) settlement to keep your working capital fluid.

- System Uptime: Aeps India offering 99.9% uptime to prevent service interruptions particularly in rural areas.

- Customer Support: 24/7 technical support is crucial for resolving failed transactions quickly.

- Additional Services: Select platforms that bundle other services like Mini ATM service, Bill Payments (BBPS), and Domestic Money Transfer service (DMT) for higher income.

- Cost of ID: Aeps India offer free or low cost Aeps registration versus those with high joining fees.

Why Choose AEPS India as a Trusted AEPS ID Provider

Aeps India is a trusted AEPS ID provider ensures secure, NPCI-compliant transactions with 99.9% uptime, offering high success rates, instant (T+0) settlements, and 24/7 support. These Aeps India enable competitive commissions, typically ₹12–₹15 per transaction, and offer comprehensive integrated Aeps services like Micro ATMs and BBPS.

Key Reasons to Choose a Trusted AEPS Provider:

- Security & Compliance: Aeps India adhere to strict NPCI and RBI/UIDAI guidelines, utilizing encrypted biometric authentication to prevent fraud.

- High Reliability & Uptime: A reputable Aeps platform guarantees 99.9% uptime, ensuring fewer transaction failures and building trust in rural and urban markets.

- Instant Settlements (T+0/T+1): Aeps India offer immediate (T+0) or same-day (T+1) settlement options, keeping working capital flowing.

- High Commissions & Transparent Structure: Agents can maximize income with competitive, transparent Aeps commission structures ranging from ₹5 to ₹15+ per transaction.

- 24/7 Technical Support: Dedicated support via phone, WhatsApp, or email is crucial for immediately resolving failed transactions and avoiding business loss.

- Comprehensive Services & Scalability: Beyond withdrawals Aeps India offers integrated, value-added services like, Micro ATM, BBPS, (bill payments), and, DMT, (money transfer) to diversify income.

Choosing a Aeps India ensures a secure and profitable, business operation.

Future Trends AEPS ID

The future of the Aadhaar Enabled Payment System (AEPS) in India is rapidly evolving toward a highly secure, AI-driven, and comprehensive rural financial ecosystem, aiming for over 3.5 billion transactions annually by 2026. As of January 1, 2026, new regulatory norms (RBI/NPCI) focus on enhancing security through stricter agent KYC, mandatory L1-certified devices, and “One Operator, One Bank” rules to combat fraud.

Key future trends for AEPS IDs and platforms include:

1. Enhanced Security and Compliance (2026 Mandates)

- L1-Certified Devices: Mandatory use of STQC-certified Level 1 (L1) fingerprint or iris scanners, which offer superior encryption at the device level, replacing older L0 devices.

- “One Operator, One Bank” Rule: Agents are restricted to linking their terminal with only one acquiring bank, increasing accountability and curbing fraudulent activities.

- Mandatory Re-KYC: Agents inactive for three consecutive months must undergo a fresh KYC process before resuming services.

- AI-Driven Liveness Detection: Advanced AI to verify the physical presence of the user, preventing spoofing attempts using silicone molds, photographs, or synthetic prints.

2. Technological Advancements

- Multi-Modal Biometrics: Moving beyond fingerprints to include iris and facial recognition, ensuring higher accessibility for the elderly or manual laborers with worn-out fingerprints.

- Face Authentication as 2FA: Face recognition (1:1 matching against Aadhaar data) is becoming a standard for two-factor authentication to increase security and success rates.

- Voice-Based Payments: Development of voice-activated, regional language systems to make banking accessible to semi-literate users.

- Blockchain Integration: Utilization of blockchain technology to create transparent, immutable transaction records for better security and audit trails.

3. Service Expansion and “Mini-Bank” Evolution

- Comprehensive Financial Hubs: Local Kirana stores are evolving from mere cash-out points into “micro-banking” hubs, offering insurance, micro-loans, digital gold, and UPI-ATM services.

- Unified Ecosystems (AEPS 3.0): Deeper integration with UPI, BBPS (Bharat Bill Payment System), and Aadhaar Pay for a seamless digital payment experience.

- Aadhaar-to-Aadhaar Transfers: Enhanced capacity for direct, secure transfers between Aadhaar-linked accounts.

4. Retailer and Agent Trends

- Instant Settlement (T+0): Demand for same-day or instant settlement (T+0) is becoming standard to keep working capital liquid for agents.

- High-Volume Incentives: Tiered commission structures and monthly bonuses (e.g., for processing >150 transactions) continue to make AEPS a profitable business model for local retailers.

- Mobile-First Approach: High-performance, mobile-responsive AEPS applications on Android Aeps devices are replacing specialized desktop setups offering higher reliability (>99.9% uptime).

These trends reflect a transition towards an identity-based payment framework that is both secure for users and highly accessible in rural India.

Conclusion

Getting an AEPS ID in India is one of the easiest ways for retailers and small business owners to enter the digital banking sector and earn regular commission income. Aeps india help of a best AEPS service provider, retailers can quickly activate AEPS ID and start offering essential Aadhaar-based banking services to customers.

An AEPS ID allows retailers to provide services such as AEPS cash withdrawal, balance enquiry, mini statement, and Aadhaar to Aadhaar fund transfer using secure biometric authentication. These services are especially valuable in rural and semi-urban areas where customers prefer nearby shops for quick and convenient banking access.

An AEPS ID is a unique credential assigned to banking agents, Business Correspondents (BCs), or retailers to access the Aadhaar Enabled Payment System platform. It enables authorized users to facilitate secure, Aadhaar-based banking transactions such as cash withdrawals, deposits, and balance inquiries using a smartphone and biometric device.

Starting an AEPS retailer business requires a few simple things, including a biometric fingerprint device, a stable internet connection, and a reliable AEPS portal platform. Once the AEPS ID is activated, retailers can begin processing transactions immediately and earn commission on every successful transaction.

Aeps india is the right AEPS portal provider in India is very important to ensure smooth operations. A reliable platform offers high transaction success rate, real-time processing, secure biometric verification, instant settlement system, and complete reporting Aeps dashboard. These features help retailers provide fast service and build long-term customer trust.

A reliable Aeps platform like AEPS India offers a simple and secure way to get an AEPS ID for retailers. With easy registration, fast transaction processing, and strong technical support, retailers can start their AEPS banking services without any complicated setup.

As digital payments and Aadhaar-based banking continue to grow across the country, the demand for AEPS services in India will keep increasing. Getting an AEPS ID from a Aeps india can help retailers expand their digital service business, support financial inclusion, and build a steady source of income in the fast-growing fintech industry.

If you want to get an AEPS ID and start AEPS services in India, the expert team at AEPS India is ready to help you. Contact us today to learn more about our secure AEPS platform, easy retailer Aeps onboard, and complete support for starting AEPS business successfully.

FAQ – AEPS ID in India

An AEPS ID is a unique identification provided to retailers or agents who want to offer Aadhaar Enabled Payment System (AEPS) services. With an AEPS ID in India, retailers can perform banking transactions like cash withdrawal, balance enquiry, and mini statement using Aadhaar authentication and biometric verification.

Anyone who wants to provide AEPS banking services can apply for an AEPS ID, including:

Retail shop owners

Mobile recharge shop owners

CSC operators

Digital payment agents

Small business owners

These users can start offering Aadhaar-based banking services in their local area.

To get an AEPS ID in India, you need to register with a top AEPS service provider like AEPS India. After completing the KYC verification and registration process, the provider will create your AEPS retailer ID, allowing you to start AEPS services from your shop or business location.

With a valid AEPS ID for retailers, you can offer several banking services, including:

Cash Withdrawal

Balance Enquiry

Mini Statement

Aadhaar-based banking transactions

These services allow customers to access their bank accounts easily without visiting a bank branch.

To apply for an AEPS ID, retailers usually need the following documents:

Aadhaar card

PAN card

Bank account details

Passport size photo

Active mobile number

These documents are required to complete the AEPS retailer registration process.

The AEPS system works through Aadhaar authentication and biometric fingerprint verification. A customer enters their Aadhaar number, selects their bank, and verifies the transaction using their fingerprint. After successful Aadhaar verification API, the transaction is completed instantly.

Retailers earn commission on every AEPS transaction they perform through their AEPS ID. As more customers use the service for cash withdrawal or balance enquiry, retailers can generate a regular income from these transactions.

To start AEPS services with an AEPS ID, retailers need the following:

Android smartphone or computer

Biometric fingerprint scanner

Stable internet connection

These tools help complete secure Aadhaar based banking transactions.

Yes, AEPS transactions are secure because they use Aadhaar authentication and biometric fingerprint verification. This ensures that only the real account holder can perform the transaction, making the system reliable and safe.

The AEPS ID activation process is usually quick. After submitting documents and completing the verification process, retailers can receive their AEPS login ID within a short time depending on the service provider.

To get an AEPS ID in India, you need to register with a Aeps india is an best AEPS service provider company in india. After completing the registration process and verification, you will receive your AEPS retailer ID and can start offering AEPS services.

Many rural areas have limited access to banks and ATMs. AEPS services help people withdraw money and check their bank balance easily through nearby retailers. This improves financial inclusion and digital banking access.

A trusted platform like AEPS India provides a reliable AEPS ID for retailers with fast transactions, secure systems, and strong technical support. It helps retailers start their AEPS business in India and provide convenient banking services to customers.

Before selecting an AEPS service provider, retailers should check:

High transaction success rate

Secure transaction system

Fast transaction processing

Easy-to-use retailer portal

Reliable customer support

Choosing a trusted provider helps retailers run a successful AEPS business.

AEPS India is a trusted platform that provides secure and reliable AEPS ID services in India. It offers fast transaction processing, easy retailer onboarding, biometric device support, and dedicated technical support, helping retailers successfully run their AEPS service business.

Latest AEPS Software Trends Every Retailer Should Know

Top AEPS Company in India 2026 – Best AEPS Service Providers for Retailers