AePS Advantages and Disadvantages: Complete Guide

The Aadhaar Enabled Payment System (AEPS) has transformed digital banking in India by allowing customers to perform cash withdrawals, balance checks, money transfers, and mini statements using their Aadhaar number and biometric authentication. AEPS is particularly beneficial for retailers, distributors, fintech startups, and businesses looking to offer secure and fast banking services to their customers, even in rural and semi-urban areas.

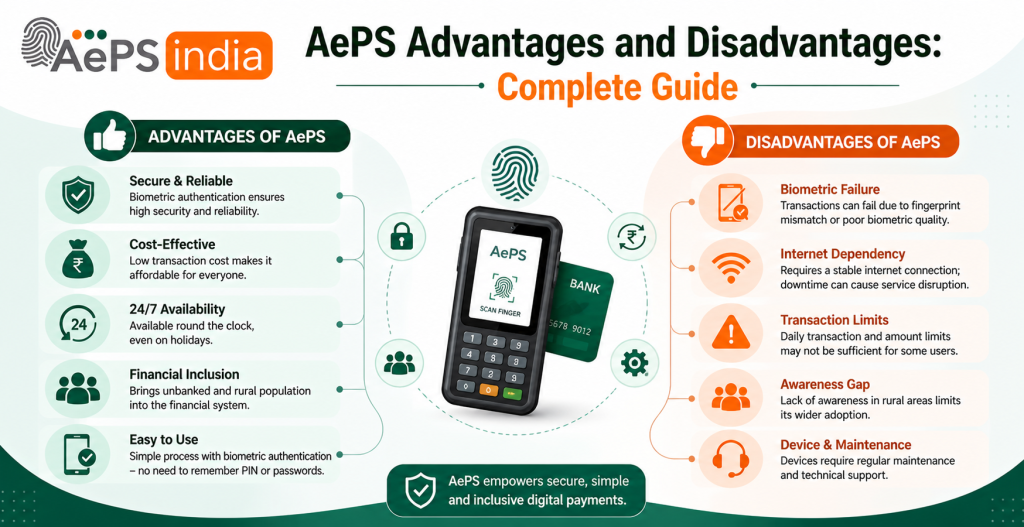

AePS advantages include convenience (no card/PIN needed), accessibility (banking in remote areas), and security (biometric authentication). Its disadvantages are technology dependency (internet and scanner issues), limited services (no complex transactions), potential for fraud if security measures are weak, and limited agent awareness, especially in rural areas.

While AEPS offers many advantages like ease of access, low setup cost, instant transactions, and financial inclusion, it also comes with certain limitations such as network dependency, authentication errors, and occasional technical challenges. Understanding both the benefits and drawbacks is crucial for businesses and retailers who want to maximize earnings, provide reliable services, and grow their digital finance business.

For retailers, distributors, and fintech startups, AEPS is not only a way to serve customers efficiently but also a profitable business opportunity. However, like any technology, AEPS comes with its advantages and disadvantages that every user and business owner should understand before implementation.

In this complete guide on AePS advantages and disadvantages, we will help you understand how AePS works, why it is important for small businesses, retailers, CSC, banking correspondents and micro ATM service providers, and what you should keep in mind before starting AePS India services.

What Is AEPS

The Aadhaar Enabled Payment System (AEPS) is a bank-led model that allows users to perform basic financial transactions using their Aadhaar number and biometric authentication, such as fingerprint or iris scan. Developed by the National Payments Corporation of India (NPCI), it facilitates transactions like cash withdrawal, cash deposit, balance inquiry, and fund transfers through micro-ATMs and business correspondent points. AEPS promotes financial inclusion by providing banking access in rural areas to those without traditional cards or internet access.

How AEPS Work

AEPS, or Aadhaar Enabled Payment System, allows for online financial transactions using an Aadhaar number and biometric authentication at a micro ATM or business correspondent point. To use it, a customer provides their Aadhaar number and bank name, selects a transaction type like cash withdrawal or balance inquiry, and authenticates with a fingerprint or iris scan. The system then securely processes the request through the bank’s server.

How AEPS works

- Authentication: The user provides their Aadhaar number and selects their bank at an AEPS-enabled terminal, like a micro ATM at a local shop.

- Biometric verification: The user’s identity is confirmed using their biometric data (fingerprint or iris scan).

- Transaction request: The user chooses the transaction type (e.g., cash withdrawal, balance inquiry, fund transfer, mini-statement) and enters the amount if applicable.

- Processing: The request is sent to the bank’s server for verification against the bank’s records.

- Completion: Once the transaction is verified, the requested action is completed, and the user receives a receipt.

Who Can Use AePS in India

Any resident of India with an Aadhaar number linked to a bank account can use AePS for basic financial transactions. This includes activities like cash withdrawal, cash deposit, and balance inquiry, which can be done at micro-ATMs or through banking correspondents using biometric authentication.

Who can use AePS

- Individuals with Aadhaar: Any Indian citizen who has an Aadhaar number.

- Linked bank account: A bank account that is linked with the Aadhaar number is essential for using the service.

- Biometric data: Users must have their biometric information (fingerprint or iris scan) linked to their Aadhaar for authentication.

What is required to use AePS

- Aadhaar number: You need your 12-digit Aadhaar number.

- Biometric authentication: A fingerprint or iris scan is used to verify your identity.

- Aadhaar-linked bank account: You must have an active bank account linked to your Aadhaar number.

- Access to a service point: You need to visit a micro-ATM or a banking correspondent (BC) point to perform transactions. No smartphone, internet connection, or debit card is required.

Top AePS Use Cases

AePS provides basic banking services through Aadhaar authentication, enabling users to perform cash withdrawals, cash deposits, fund transfers, and balance inquiries using only their Aadhaar number and a biometric verification. It aims to increase financial inclusion by offering these services at micro-ATMs and through business correspondents, eliminating the need for physical cards or PINs.

Core services offered by AePS

- Cash Withdrawal: Withdraw cash from an Aadhaar-linked bank account at a point of service.

- Cash Deposit: Deposit cash directly into an Aadhaar-linked account.

- Balance Enquiry: Check the current balance of your bank account.

- Fund Transfer: Transfer money between Aadhaar-linked bank accounts.

- Mini Statement: View a summary of recent transactions.

Advantages of AEPS

The main advantage of the Aadhaar Enabled Payment System (AEPS) is its ability to provide accessible, secure, and instant banking services to a broad population, especially those in rural and unbanked areas. It leverages biometric authentication linked to an individual’s Aadhaar number, eliminating the need for physical cards, PINs, or smartphones to perform basic financial transactions.

Advantages for customers

- Convenience and accessibility: AEPS allows individuals to perform banking transactions at micro-ATMs operated by local business correspondents (agents), reducing the need to travel long distances to bank branches or ATMs.

- Ease of use: The system is simple to use, requiring only the customer’s Aadhaar number and biometric authentication. This is particularly beneficial for those with low digital literacy.

- High security: The biometric verification system ensures a high level of security, as fingerprints or iris scans are unique to each individual. This is generally considered safer than traditional PIN-based transactions, which can be forgotten or stolen.

- Interoperability: Customers of any bank can transact at any AEPS-enabled micro-ATM, regardless of which bank they belong to. This makes banking services universally accessible.

- Access to essential services: AEPS supports a range of basic banking services, including cash withdrawals, cash deposits, balance inquiries, and Aadhaar-to-Aadhaar fund transfers.

Advantages for financial institutions and retailers

- Expanded reach and financial inclusion: AEPS offers banks a cost-effective way to extend their services to remote, rural, and underserved areas without the expense of building and maintaining physical bank branches.

- Increased customer base: By offering banking services through AEPS, retailers and agents can attract more customers to their shops, which can lead to increased sales of other goods and services.

- New revenue streams: Retailers and business correspondents earn a commission for each transaction they facilitate, creating a new source of income.

- Efficient cash management: The AEPS system helps small businesses and retailers manage cash more efficiently by providing an easy way to deposit or dispense cash.

- Enhanced security and trust: For institutions, AEPS provide secure, real-time transaction processing, which builds customer confidence in using digital financial services.

Advantages for the government and economy

- Efficient direct benefit transfers (DBT): AEPS ensures that government welfare payments, subsidies, and pensions are securely and directly disbursed into the bank accounts of beneficiaries. This reduces leakages and improves transparency in welfare schemes.

- Promotion of the digital economy: By providing an easy and accessible way to conduct digital transactions, AEPS supports the broader goal of reducing reliance on physical cash and moving toward a cashless society.

- Reduced reliance on physical infrastructure: The system’s use of micro-ATMs reduces the dependence on a costly network of physical bank branches and ATMs.

- Empowerment of vulnerable communities: AEPS provides financial autonomy to vulnerable groups like the elderly, illiterate, and daily wage earners, allowing them to manage their finances independently.

Potential challenges and security risks

While AEPS is highly secure, it is not entirely risk-free. Some concerns include:

- Biometric fraud: There have been instances of fraud where criminals stole Aadhaar numbers and cloned fingerprints from sources outside the AEPS system.

- Lack of transaction alerts: In some cases, users in areas with poor network connectivity may not receive real-time SMS alerts for transactions, delaying the detection of fraud.

- Dependence on technology: The system relies on biometric scanners and internet connectivity, which can be inconsistent in remote areas.

Disadvantages of AEPS

Major disadvantages of AEPS include its reliance on internet connectivity and infrastructure, high transaction failure rates, and significant security risks related to biometric and agent fraud. The system also has limited functionality compared to other digital payment options.

Connectivity and infrastructure issues

- Internet and electricity dependency: AEPS transactions rely on a stable internet connection and power supply. In many rural and remote areas where AEPS is most needed, this infrastructure is often unreliable, leading to transaction failures.

- High failure rate: Due to connectivity issues, biometric mismatches, and bank server problems, AEPS has a high transaction failure rate. These failures can lead to customer frustration and delay access to funds.

- Delays: Technical glitches, network timeouts, and bank system mismatches can cause significant delays in processing transactions, leaving customers stranded without their money.

Security and fraud risks

- Biometric spoofing: Fraudsters can exploit the system by creating cloned or fake fingerprints to perform unauthorized withdrawals from bank accounts. This is a particularly serious risk for vulnerable users like senior citizens.

- Agent fraud: Unscrupulous Business Correspondents (BCs) or agents may misuse their access to the system. This can involve charging extra commissions, performing unauthorized transactions using a customer’s biometric data, or providing less cash than requested.

- Identity theft: Fraudsters can illegally obtain a victim’s Aadhaar number and use their personal data for fraudulent activities, such as opening fake accounts or misusing government benefits.

- Weak oversight: Inadequate oversight and lack of robust fraud detection systems for rural agents leave the system vulnerable to insider fraud.

Functional limitations

- Limited services: AEPS designed for basic banking functions like cash withdrawals, deposits, and balance inquiries. It cannot be used for more complex activities such as bill payments, investments, or applying for loans, requiring users to rely on other, more sophisticated payment methods.

- Aadhaar dependency: The system is exclusively for customers with Aadhaar-linked bank accounts. If an individual does not have an Aadhaar number or if it is not properly linked, they cannot use AEPS.

User-related issues

- Biometric authentication problems: Issues with biometric authentication are a major cause of transaction failures. These can result from worn-out or damaged fingerprints (common among manual laborers), malfunctioning scanners, or incorrect finger placement.

- Lack of awareness: Many people, especially in remote areas, are unaware of AEPS or how to use it safely. A lack of digital literacy and financial awareness makes them more susceptible to fraud and error.

- Limited agent availability: In some areas, there may be very few local AEPS agents or micro-ATMs, making it difficult for people to access the service when they need it.

How AePS Helps in Financial Inclusion in Rural India

AePS helps financial inclusion in rural India by providing convenient and secure basic banking services through a network of local agents using just an Aadhaar number and biometric authentication. This system connects rural residents to the formal banking system, enabling them to perform transactions like cash withdrawals, deposits, and balance inquiries without needing to travel to a distant branch. By facilitating direct benefit transfers for government schemes and supporting digital payments, AePS has been crucial in expanding financial access and promoting digital literacy in underserved areas.

How AePS promotes financial inclusion

- Accessibility: It brings banking services to remote areas via local merchants and agents, reducing the need for long and costly travel to physical bank branches.

- Biometric Security: AePS uses fingerprint or iris scans for authentication, which is more secure and reduces the risk of fraud compared to card-based transactions.

- Ease of Use: Transactions require only an Aadhaar number and biometrics, making the system accessible to people with limited technical or literacy skills.

- Government Scheme Disbursement: AePS provides a secure channel for direct benefit transfers (DBT) from government schemes like pensions and NREGA, ensuring subsidies and payments reach beneficiaries directly and efficiently.

- Support for Digital Economy: It enables small businesses and rural shopkeepers to accept digital payments, allowing them to participate in the digital economy without needing complex Point-of-Sale (POS) systems.

- Cost-Effectiveness: It is a cost-effective solution for banks to extend their services, as it reduces the need to build and maintain physical branches in remote locations.

- Interoperability: The system is interoperable across banks, meaning customers can perform transactions from any participating bank through Aeps India.

How Retailers Can Earn More Using AEPS

Retailers can earn more using the Aadhaar Enabled Payment System (AEPS) primarily through commissions on transactions, increased customer traffic, and by diversifying their service offerings. By becoming a local “micro-ATM”, a shop provides essential financial access, especially in underserved areas, which builds customer trust and loyalty.

Key Ways Retailers Boost Earnings with AEPS

- Direct Commissions on Transactions: Retailers earn a fee for every successful AEPS transaction they facilitate. Commissions are typically tiered, meaning higher-value transactions like cash withdrawals often yield higher earnings (e.g., Aeps India offer up to ₹13 or more for transactions over ₹3,000). Other services like balance inquiries and mini statements also provide smaller, consistent commissions.

- Increased Customer Footfall: Offering basic banking services (cash withdrawals, deposits, balance checks) attracts new customers to the store who might not have visited otherwise. This increased traffic creates opportunities for cross-selling the retailer’s primary goods and services, boosting overall sales.

- Expanded Service Offerings: AEPS platforms allow integration with other digital services, turning the shop into a one-stop destination for various needs. Additional services can include:

- Mobile and DTH recharges

- Utility bill payments (electricity, gas, insurance)

- Domestic Money Transfers (DMT)

- Low Investment, High Return Model: The Aeps setup cost for an AEPS business is relatively low, requiring only a smartphone or computer and a certified biometric device. This minimal initial investment, combined with the potential for substantial commission-based income, offers significant return on investment.

- Enhanced Community Trust and Loyalty: By providing convenient and secure financial services through government-backed Aadhaar authentication, retailers position themselves as reliable and essential hubs in their communities. This deepens customer relationships and encourages repeat business.

How to Choose the Best AePS Provider in India

Aeps India is the best AePS provider in India, prioritize regulatory compliance by verifying NPCI and RBI certification. Then, evaluate reliability and performance by checking transaction success rates, and assess security measures like encryption and two-factor authentication. Finally, consider factors like user-friendly interfaces, transparent costs, and reliable 24/7 customer support.

1. Ensure regulatory compliance and security

- NPCI and RBI certification: Ensure the Aeps India is certified by the National Payments Corporation of India (NPCI) and complies with Reserve Bank of India (RBI) guidelines.

- Security measures: Look for Aeps India that use strong security, such as SSL, encryption, and two-factor authentication, to protect your data and transactions.

- Bank partnerships: Confirm the Aeps India has direct connections with authorized banks for secure transactions.

2. Evaluate reliability and performance

- Transaction success rates: Choose a Aeps India with a high success rate, ideally above 98%, and minimal downtime.

- Scalability: Ensure the Aeps b2b platform can grow with your business needs.

- Reputation: Aeps India reputation through reviews and testimonials to gauge reliability.

3. Consider costs and features

- Transparent pricing: Look for clear and transparent information on commission structures and other costs.

- Multi-bank support: Ensure the Aeps India supports a wide range of banks to cater to more customers.

- Additional services: Aeps India offer other services like bill payments, money transfers, and mini-statement services.

4. Look for good support and user experience

- User-friendly interface: The Aeps admin platform should have an intuitive and easy-to-navigate interface for both you and your customers.

- 24/7 customer support: Reliable and round-the-clock customer and technical support are crucial for resolving issues quickly.

- Integration: Check for easy integration with your existing systems or the availability of Aeps API solutions.

Why AEPS India is a Trusted Platform for Retailers

AEPS India is a trusted Aeps platform for retailers due to its security, increased revenue opportunities, and ability to drive customer footfall. It uses secure biometric authentication and follows RBI and NPCI guidelines, ensuring safe transactions. Retailers earn commissions on services like cash withdrawals and can expand their service offerings to new customers and increase revenue.

Benefits for retailers

- Increased revenue: Retailers earn a commission on each transaction, creating an additional income stream.

- Higher customer footfall: By providing essential banking services like cash withdrawals and balance checks, retailers attract new customers, especially in areas with limited access to traditional banks.

- Expanded services: Retailers can offer a wider range of services, such as mobile top-ups and bill payments, through the same platform, further increasing earning potential.

- Enhanced customer experience: AEPS provides a convenient and secure way for customers to conduct basic banking, which can boost customer loyalty and trust.

- Financial inclusion: The platform is crucial for financial inclusion, bringing banking services to underserved rural and semi-urban areas.

- Cost-effectiveness: Implementing AEPS is a low-cost way to provide financial services compared to setting up a traditional bank branch.

Security and compliance

- Biometric authentication: Transactions are secured using a customer’s Aadhaar and fingerprint, which makes the system secure and reduces the risk of fraud.

- Regulatory adherence: AEPS operates under the guidelines of the National Payments Corporation of India (NPCI) and the Reserve Bank of India (RBI).

- Data protection: Strong security measures, such as data encryption, are in place to protect user data.

Future Scope of AEPS in India

The future of AEPS in India is marked by enhanced security, deeper integration with other digital platforms like UPI, and a wider range of services beyond basic banking. The government and RBI are focusing on improving security through AI, biometrics, and stricter regulations to curb fraud. Expect user-friendly, mobile-first solutions and expansion into areas like insurance and loan payments, especially for rural and underbanked populations.

Key trends shaping the future of AEPS

Enhanced security:

- AI and machine learning: For real-time fraud detection, anomaly analysis, and risk management.

- Advanced biometrics: Stronger and more reliable biometric verification to improve security.

- Stricter regulations: The Reserve Bank of India (RBI) is implementing new rules to enhance security and trust in the system.

Deeper integration:

- Unified platforms: AEPS will integrate seamlessly with other digital systems like UPI, digital wallets, and BBPS to create a comprehensive financial ecosystem.

- Mobile-first solutions: Increased focus on user-friendly apps and mobile interfaces to make AEPS more accessible.

Expanded services:

- Beyond basic banking: Services like micro-loans, insurance payments, and online shopping payments will be integrated into the AEPS platform.

- Aadhaar-to-Aadhaar Fund Transfers: The ability to transfer money directly from one Aadhaar-enabled account to another.

Improved user experience:

- Simpler interfaces: A focus on creating more intuitive and easy-to-use interfaces for both end-users and agents.

- Greater accessibility: Continued efforts to improve infrastructure and awareness to reach more people, particularly in rural areas.

Conclusion

Understanding the advantages and disadvantages of AEPS is important for anyone planning to use or offer Aadhaar-based banking services. While AEPS brings big benefits like easy cash withdrawal, quick transactions, low setup cost, and access to banking in rural areas, it also comes with challenges such as network issues, Aadhaar authentication problems, and dependency on biometric accuracy.

AePS offers advantages like convenience and accessibility through Aadhaar-based biometric authentication, especially for those in remote areas, and security by eliminating the need for cards and PINs. However, it has disadvantages including technology dependency, the risk of fraud due to inadequate security measures, and limited service offerings compared to traditional banking.

For retailers, distributors, and businesses, AEPS is still one of the best earning opportunities in the digital finance market. When supported by a secure AEPS provider, fast AEPS API, and reliable Aeps admin software, the system works smoothly and helps you serve more customers every day.

AEPS India gives businesses a chance to grow by offering trusted banking services in local areas. With the right Aeps platform and proper setup AEPS can help you increase customer footfall, generate more income, and build a strong digital service business.

AEPS is a powerful solution with huge potential just choose a trusted Aeps India to enjoy all the advantages while reducing the challenges.

Frequently Asked Questions (FAQs) – AEPS Advantages and Disadvantages

AEPS is a digital payment system in India that allows users to perform cash withdrawals, balance inquiries, mini statements, and fund transfers using their Aadhaar number and biometric authentication.

Quick and secure transactions

Access to banking in rural and remote areas

Low investment with high earning potential

Real-time settlement and reporting

White label Aeps and Aeps API integration options for fintech startups

Dependent on internet connectivity and biometric devices

Occasional transaction failures or delays due to network issues

Limited transaction amount per day

Requires proper KYC and Aadhaar authentication

Yes. Retailers earn commission on every transaction, including withdrawals, fund transfers, and balance checks. Real-time reporting ensures transparent income tracking.

Yes. AEPS follows UIDAI and NPCI guidelines, uses end-to-end encryption, and authenticates users through biometric verification, making it highly secure.

Startups and fintech businesses can integrate AEPS API to offer banking and digital payment services, generate revenue through commissions, and expand their customer base quickly.

You need a biometric device (fingerprint scanner), internet-enabled system, and an AEPS-enabled software or Aeps app to process transactions.

Yes. AEPS is regulated by UIDAI and NPCI, making it completely legal for banks, retailers, and fintech businesses.

Yes, AEPS is designed to promote financial inclusion, and even semi-urban and rural areas can access banking services through compatible devices and apps.

AEPS India provides trusted AEPS b2b software, Aeps API solution, and white-label options to help businesses offer secure, fast, and scalable banking services, increasing revenue and customer trust.

AePS Portal Service Provider in India (2026 Complete Guide)

What is AEPS API? Complete Guide 2026