AEPS Application: Complete Guide for Retailers and Businesses

The AEPS Application (Aadhaar Enabled Payment System App) has become one of the most powerful digital fintech tools for retailers, distributors, and small businesses in India. With AEPS, shop owners can offer essential banking services like cash withdrawal, balance enquiry, mini statement, and Aadhaar-based money transfer directly from their store using just a fingerprint device. This not only increases customer footfall but also helps retailers earn a high commission income every day.

An AEPS application is a platform that enables transactions via the Aadhaar Enabled Payment System (AEPS), a secure, biometric-based system developed by the National Payments Corporation of India (NPCI) that allows users to conduct basic banking activities like cash withdrawals, deposits, balance inquiries, and fund transfers using just their Aadhaar number and biometrics. These applications are crucial for providing financial inclusion in rural and remote areas, allowing users to perform banking through a network of bank correspondents and micro-ATMs.

If you are a retailer or business owner looking to start AEPS services and earn more, Aeps India is the right AEPS application provider is the most important step. A secure, fast, and reliable AEPS app helps you serve customers better, reduce failures, and grow your income every month.

At Aeps India, we offer a powerful and user-friendly AEPS application that helps retailers, Aeps B2B companies, and fintech startups launch their AEPS business with high success rates, strong security, and top commissions.

In this complete guide, Aeps India explains everything about AEPS applications how they work, why they are important, key features, earning opportunities, setup process, and how retailers can grow their income with Aadhaar banking services. Whether you are a small shop owner, a CSC center, a distributor, or a fintech startup, this guide will help you understand how to use an AEPS Application to build a successful digital service business.

What is AEPS Application

An AEPS (Aadhaar Enabled Payment System) application is a digital platform that allows users to perform financial transactions using only their Aadhaar number and biometric authentication like fingerprints. These applications enable services such as cash withdrawal, cash deposit, balance inquiry, and fund transfers through a bank-led model that links a customer’s Aadhaar to their bank account. They are particularly useful for financial inclusion in remote areas where traditional banking is difficult to access.

AEPS Application Work

The Aadhaar Enabled Payment System (AEPS) is a bank-led model that allows online financial transactions at micro ATM or Point-of-Sale (PoS) terminals using Aadhaar number and biometric authentication. It eliminates the need for debit cards, credit cards, or physical bank visits, primarily serving individuals in rural and remote areas to promote financial inclusion.

How AEPS Works

The system operates through a network of banking correspondents (agents) equipped with micro-ATMs and biometric scanners.

- Visit a Service Point: The customer visits an AEPS-enabled local shop or banking correspondent (BC).

- Provide Details: The customer provides their 12-digit Aadhaar number and specifies their bank name.

- Choose Transaction: The customer selects the desired transaction type (e.g., cash withdrawal, deposit, balance inquiry, mini statement).

- Biometric Authentication: The customer authenticates their identity by placing their finger or performing an iris scan on the biometric device. This data is verified in real-time by the Unique Identification Authority of India (UIDAI) against their database.

- Transaction Completion: Upon successful verification, the transaction is processed, and the customer receives a confirmation receipt.

Key Requirements for Use

To utilize AEPS, a customer needs the following:

- An active bank account linked to their Aadhaar number.

- Their 12-digit Aadhaar number.

- Their biometric data (fingerprint or iris scan) available at the time of the transaction.

- Access to an AEPS-enabled micro-ATM or banking correspondent.

AEPS is a significant initiative by the National Payments Corporation of India (NPCI) to bridge the gap between traditional banking infrastructure and the unbanked masses, particularly in remote areas of India.

Who Can Use AEPS Application

Any Indian citizen with an Aadhaar number linked to a bank account can use an AEPS (Aadhaar Enabled Payment System) application to perform basic banking transactions like cash withdrawal, deposit, and balance inquiries through biometric authentication. Users do not need a smartphone, debit card, or internet connection; they only need to visit an AEPS-enabled micro-ATM with their Aadhaar and biometric details.

Who can use AEPS

- Indian citizens: Anyone who is a resident of India is eligible.

- Aadhaar cardholders: You must have a valid Aadhaar number.

- Bank account holders: Your Aadhaar number must be linked to an active bank account that is part of the AEPS network.

What you need to use AEPS

- Aadhaar number: To authenticate your identity.

- Biometric data: Your fingerprint or iris scan, linked to your Aadhaar, for authentication.

- Bank account: An active bank account linked with your Aadhaar.

- Access to a Micro-ATM: You need to visit a point-of-sale terminal or micro ATM provided by a Aeps India.

AEPS Application Services Offered

AEPS (Aadhaar Enabled Payment System) application services allow customers to perform basic banking transactions at micro-ATMs or banking correspondent points using their Aadhaar number and biometric authentication (fingerprint or iris scan).

The core services typically offered include:

- Cash Withdrawal: Customers can withdraw cash from their Aadhaar-linked bank accounts at a local merchant or banking correspondent location (functioning as a micro-ATM) using only their Aadhaar number and biometric authentication (fingerprint or iris scan).

- Balance Inquiry: Users can instantly check their bank account balance through the AEPS app providing real-time financial information without needing to visit a physical bank branch.

- Mini Statement: Customers can obtain a summary of their recent transactions, helping them keep track of their account activity.

- Cash Deposit: The application allows for cash to be deposited into an Aadhaar-linked account, adding a crucial banking service at local touchpoints.

- Aadhaar-to-Aadhaar Fund Transfer: Secure money transfers can be made between two Aadhaar-linked bank accounts (Aadhaar-to-Aadhaar fund transfer), facilitating interbank and intrabank transactions.

- Direct Benefit Transfer (DBT) Disbursement: The government uses AEPS to disburse subsidies, social security pensions, and other welfare scheme benefits directly and transparently into the beneficiaries’ bank accounts, reducing corruption and leakage.

- BHIM Aadhaar Pay: This is a merchant-centric service that enables small businesses to accept cashless payments from customers using their Aadhaar number and biometrics, promoting digital transactions at the point of sale.

Additional Services

Beyond core banking, AEPS applications may also facilitate:

- eKYC (Electronic Know Your Customer): AEPS provides a real-time, paperless method for identity verification, which is used by banks and other financial institutions to onboard new customers quickly and securely.

- Government Benefit Disbursements: A secure channel for citizens to access Direct Benefit Transfer (DBT) payments, subsidies, and pensions.

- Micro Merchant Payments: Allowing small businesses to accept digital payments with simple infrastructure.

- Aadhaar Seeding Status Check: The ability to check if an Aadhaar number is successfully linked to a bank account.

These services play a crucial role in promoting financial inclusion, especially in rural and underserved areas, by making essential banking services accessible without the need for physical bank branches or complex documentation.

Documents Required for AEPS Application Activation

To activate AEPS application, you need your Aadhaar Card, PAN Card, and Bank Account details (including a cancelled cheque or bank passbook for verification). You will also need a passport-sized photograph and a functional mobile number linked to your Aadhaar and bank account.

Mandatory documents

- Aadhaar Card: Must be linked to your bank account.

- PAN Card: Required for KYC verification.

- Bank Account Details: An active savings account with the first page of the passbook, a cancelled cheque, or a bank statement for verification.

- Passport-sized photograph: A recent photo on a neutral background.

Other important requirements

- Mobile Number: Must be registered with your bank and linked to your Aadhaar.

- Biometric Device: A UIDAI-certified fingerprint scanner or biometric device is needed for transactions.

- Smartphone or Computer: To access the AEPS portal.

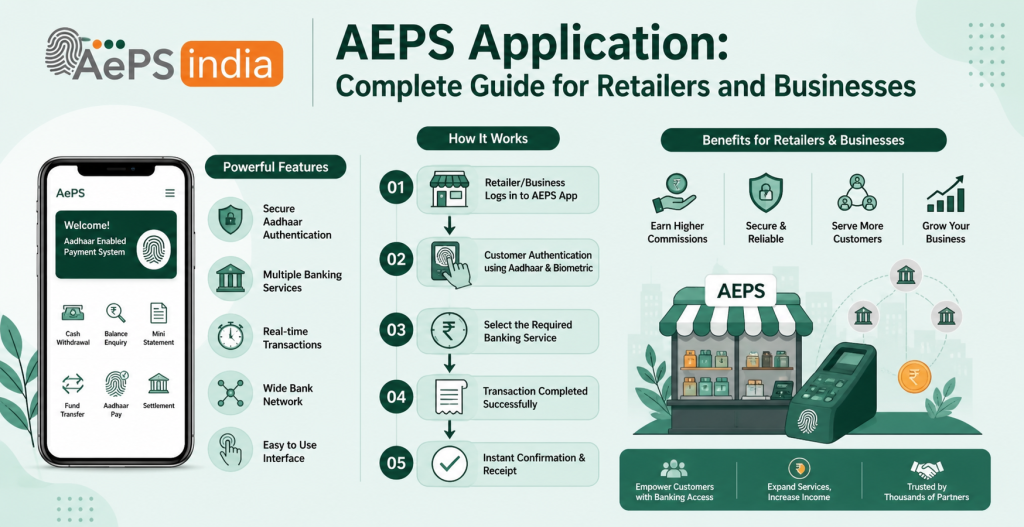

Why Retailers and Business Need an AEPS Application

Retailers and businesses need an AEPS application to create a new revenue stream through commissions, attract more customers to their store by offering essential banking services, and build customer loyalty. This application enables them to provide secure, basic banking services like cash withdrawals, deposits, and balance inquiries in their community, fostering financial inclusion, especially in areas with limited access to traditional banks.

Benefits for retailers and businesses

- Generate new income: Businesses earn a commission on each transaction, creating a new and consistent revenue stream.

- Attract more customers: By offering in-demand services like cash withdrawals and balance inquiries, retailers can increase foot traffic and customer engagement.

- Increase sales of other products: More customers visiting the store for banking services can lead to increased sales of the business’s primary products and services.

- Boost customer loyalty: Providing a convenient and essential service enhances the customer experience, encouraging repeat business and building stronger relationships.

- Promote financial inclusion: Businesses become crucial points for financial services, helping to serve the unbanked and underbanked population in their local area.

- Streamline operations: AEPS allows for faster, more efficient, and real-time transactions, improving customer satisfaction and business productivity.

- Expand service offerings: An AEPS app integrated with other digital services like bill payments and recharges, making the business a one-stop shop.

How AEPS Application Helps Earn More Income

An AEPS application helps earn more income by providing commissions on transactions like cash withdrawals and deposits, attracting more customers to a store, and increasing sales of other products. It creates a new, low-investment revenue stream that is especially profitable in areas with limited banking access.

Earn direct income

- Commissions on transactions: You earn a commission on every AEPS transaction, such as cash withdrawals, cash deposits, and balance inquiries.

- Higher value transactions, higher commission: The commission earned is often directly related to the transaction amount, so larger withdrawals generate more income.

Increase business and sales

- Increased footfall: By providing basic banking services, you attract customers to your shop, who may then purchase other goods or services.

- Cross-selling opportunities: Customers who come to withdraw cash can be encouraged to make additional purchases like mobile recharges or other items from your store.

Lower investment, higher returns

- Low startup cost: A AEPS setup only requires a smartphone, an internet connection, and a certified biometric device, making it a cost-effective way to generate income.

- High earning potential: The ability to earn steady income through commissions with minimal investment makes it a profitable business opportunity.

Expand services and reach

- Serve unbanked customers: AEPS allows customers to perform banking transactions without needing an ATM card or internet banking, reaching people in rural and semi-urban areas.

- Enhance customer trust: By offering convenient and secure financial services, you can build trust with your customers and become a reliable local banking point.

Features AEPS Application

An AEPS application key features include basic banking services like cash withdrawal, deposit, and balance inquiry, all secured by biometric authentication (fingerprint/iris scan). It is interoperable across banks, meaning users can access accounts from different banks through a single aeps application. Other features include real-time transaction processing, fund transfers, mini-statements, and a focus on promoting financial inclusion by providing services in remote areas.

Core banking features

- Cash withdrawal and deposit: Allows users to deposit or withdraw cash from their Aadhaar-linked bank accounts.

- Balance inquiry: Users can check their account balance in real-time.

- Mini-statement: Provides a summary of recent account transactions.

- Fund transfer: Facilitates money transfers between Aadhaar-linked accounts.

Security and authentication

- Biometric authentication: Uses fingerprints or iris scans to authenticate transactions, eliminating the need for cards or PINs.

- Aadhaar-based ID: Uses the Aadhaar number as a unique identifier for accessing bank accounts.

Accessibility and interoperability

- Interoperability: Supports transactions across multiple banks.

- Wide accessibility: Transactions can be performed at various points of service, such as banking correspondents and micro-ATMs, making it suitable for remote areas.

- Easy to use: The interface is simple, designed for users with minimal technical knowledge.

Other features

- Real-time processing: Ensures transactions are processed and confirmed instantly.

- Promotes cashless economy: Encourages the use of digital transactions, reducing reliance on cash.

- Supports government disbursements: Can be used for Direct Benefit Transfers (DBT) and social security pensions.

Benefits AEPS Application

The benefits of AEPS (Aadhaar Enabled Payment System) applications include enhanced financial inclusion, particularly in rural areas, by providing basic banking services through biometric authentication. It offers ease of use by eliminating the need for cards or PINs, and its high security is based on biometric (fingerprint) authentication. AEPS also streamlines government subsidy disbursements, allows for various transactions like cash withdrawal, deposit, balance inquiry, and fund transfers, and promotes a cashless economy.

Convenience and accessibility

- Simplified transactions: Users can perform banking transactions using only their Aadhaar number and fingerprint, eliminating the need to remember PINs or carry cards.

- Wider reach: It provides access to banking services in remote and underserved regions through micro-ATMs and business correspondents.

- On-demand services: Basic banking services like cash withdrawal, deposit, fund transfer, and balance inquiry are available through various touchpoints.

Security and inclusion

- Biometric security: Transactions are secured by biometric authentication, making them highly resistant to fraud.

- Financial inclusion: AEPS helps bring unbanked and underbanked populations into the formal financial system.

- Bank information privacy: It allows transactions without revealing sensitive bank account details.

- Seamless government payments: It is used to facilitate the direct disbursement of government entitlements like pensions and subsidies.

Cost-effectiveness and efficiency

- Cost-effective solution: The Aeps system reduces the dependency on physical bank branches and paper-based transactions, making it a cost-effective solution for both financial institutions and customers.

- Promotes cashless economy: By enabling easy digital transactions, it supports the growth of a cashless economy.

Steps to Start AEPS Application

To apply for the AEPS (Aadhaar Enabled Payment System) application, you must register with a Aeps India, complete KYC by submitting documents like your Aadhaar and PAN, get a compliant biometric device, and then integrate the AEPS software or app. After registration, you can use the system to provide customer services like cash withdrawals and balance inquiries through biometric authentication.

1. Choose a Aeps India

- Select a trusted AEPS service provider like Aeps India.

- Complete the registration form on their Aeps India website or app.

2. Complete the Know Your Customer (KYC) process

- Provide necessary personal and business information.

- Submit required documents, including your Aadhaar card, PAN card, and bank details for verification.

- Aeps India may also require physical verification.

3. Register your hardware

- Purchase a UIDAI-certified biometric device (fingerprint or iris scanner).

- Register the device with the Aeps India through their Aeps admin portal or application.

4. Integrate the application

- Install the AEPS application provided by the Aeps India on your smartphone or computer.

- If required, integrate AEPS API into your own existing business Aeps platform.

5. Start transacting

- Log in to the Aeps India application and start serving customers.

- When a customer wants to use a service, authenticate them using their Aadhaar number and biometric scan (fingerprint or iris).

- Provide services like cash withdrawal, balance inquiry, and fund transfer.

- Always provide a printed receipt for each transaction.

AEPS Application Commission Structure

AEPS commission varies by Aeps India, but generally, retailers earn a percentage or a fixed amount per transaction, which increases with the transaction value. For example, a retailer might earn about ₹2 for transactions between ₹100-₹999 and up to ₹13 or more for transactions of ₹3000 and above. In addition to cash withdrawals, commissions can also be earned from other services like balance inquiries and fund transfers.

Commission structure

- Tiered commissions: Aeps India typically use a tiered system where the commission increases with the transaction amount. For example:

- ₹100-₹999: Around ₹2 per transaction

- ₹1000-₹1499: Around ₹3 per transaction

- ₹1500-₹1999: Around ₹4.5 per transaction

- ₹2000-₹2499: Around ₹5.5 per transaction

- ₹3000 and above: Up to ₹13 or more per transaction.

- Percentage-based commissions: Aeps platforms may offer a percentage of the transaction value as a commission, such as 1.25%.

- Other services: Retailers can also earn commissions on services other than cash withdrawal, such as:

- Balance inquiry: Approximately ₹2-₹5

- Mini statement: Approximately ₹3-₹7

- Fund transfers and BBPS: Between ₹3 and ₹8

How to maximize earnings

- Encourage customers to use AEPS for their transactions to increase your commission-earning potential.

- Offer additional services like fund transfers and bill payments to generate more income.

- Consider offering integrated services, such as mobile recharges, to create a one-stop-shop for customers.

Security Features You Must Check Before Using Any AEPS App

When selecting and using any AEPS app, you must check for robust security features and follow specific user best practices to protect your information and funds.

Essential Security Features to Look for in an AEPS App

- NPCI and RBI Certification: The Aeps India should be certified by the National Payments Corporation of India (NPCI) and follow Reserve Bank of India (RBI) guidelines.

- Biometric Authentication: Look for an Aeps app that uses a UIDAI-certified, STQC-compliant biometric device for fingerprint or iris scans, which is a core security feature of AEPS.

- Data Encryption: Sensitive information should be protected with end-to-end encryption during transmission and storage.

- Secure Biometric Data Handling: The app should not store raw biometric data locally or on its servers, using it only for one-time authentication with UIDAI.

- Fraud Detection Mechanisms: The system should include fraud detection tools and real-time monitoring.

- Access Controls and KYC: Aeps India must implement strict Know Your Customer (KYC) protocols for onboarding agents and merchants.

- Real-Time Transaction Alerts: The Aeps app provide instant notifications for every transaction.

User Best Practices for Security

- Only Use Trusted Service Points: Transact at authorized AEPS locations like bank branches or verified merchant kiosks.

- Keep Aadhaar Details Confidential: Avoid sharing your Aadhaar number or biometric information carelessly. Consider using your Aadhaar Virtual ID (VID).

- Lock Your Biometrics: Use the UIDAI website or mAadhaar app to lock your biometric data, unlocking it only when necessary for a transaction.

- Monitor Account Activity: Regularly check your bank statements and transaction history for any issues.

- Inspect the Biometric Device: Before a transaction, confirm the biometric scanner is untampered and certified.

- Enable Alerts: Ensure your mobile number is linked to your bank account and Aadhaar to receive transaction alerts.

- Report Suspicious Activity: Report unauthorized transactions to your bank and the National Cyber Crime Reporting Portal immediately.

Choosing the Best AEPS Application Provider

Aeps India is the best AEPS application provider, prioritize Aeps India that are NPCI and RBI compliant, offer high reliability with a proven transaction success rate, and provide a robust and secure Aeps platform. Additionally, evaluate Aeps India based on features like a user-friendly interface, multi-bank support, a strong Aeps admin panel for management, and responsive 24/7 customer support.

Key factors to consider

Security and Compliance:

- Ensure the Aeps India is certified by the National Payments Corporation of India (NPCI) and follows all Reserve Bank of India (RBI) guidelines.

- Look for strong data encryption and other security measures to protect sensitive financial and personal information.

Reliability and Performance:

- Check for a high transaction success rate and minimal downtime, aiming for 98%+.

- Look for real-time transaction processing, including fast biometric authentication and instant confirmation.

Features and Functionality:

- Assess the Aeps admin panel to see if it’s robust enough for managing agents, monitoring transactions, and setting commissions.

- Ensure the Aeps application supports a wide range of banks to provide flexibility for your customers.

- Consider additional features like mobile recharge, bill payments, or ticket booking to increase revenue.

Ease of Use and Integration:

- Choose a platform with a user-friendly interface that is easy for both agents and customers to use.

- Verify that the Aeps API integrate seamlessly with your existing systems and infrastructure.

Cost and Support:

- Best Aeps commission structures and understand all fees to ensure the Aeps India is cost-effective.

- Evaluate the quality and responsiveness of their customer support, ideally with 24/7 availability via call, chat, or WhatsApp.

Scalability and Reputation:

- Select a platform that can scale with your business as transaction volume increases.

- Read user reviews and testimonials to gauge the company’s reputation for service quality and support.

Why Aeps India Is the Best AEPS Application Provider

Aeps India is the best AEPS application provider is determined by factors like strong security, high transaction success rates, regulatory compliance (NPCI/RBI certification), reliable 24/7 customer support, and an easy-to-use interface. Other key features include seamless integration capabilities, transparent commission structures, and a wide range of services beyond just AEPS, such as bill payments.

Key factors to consider when choosing an AEPS provider

- Security and compliance: The Aeps India must be certified by the NPCI and follow RBI guidelines, using strong data encryption and biometric authentication.

- Reliability and performance: Look for high transaction success rates (ideally

98%+98%+), low downtime, and fast settlement times (e.g., T+1).

98%+98%+), low downtime, and fast settlement times (e.g., T+1). - Customer support: 24/7 technical and customer support is crucial for promptly resolving issues and minimizing service disruptions.

- User-friendliness: The platform should be intuitive and easy for both agents and customers to use, with a clear and simple interface.

- Integration and scalability: Aeps India offers seamless integration through secure Aeps API and can scale with your business growth.

- Comprehensive services: Beyond core AEPS functions like cash withdrawal and deposit, look for additional services like bill payments, mobile recharge, and Micro ATM services.

- Cost and commission: Compare commission structures and understand all costs, including licensing fees, to ensure transparency and profitability.

- Multi-bank support: The system should support transactions across a wide network of banks.

Future Trends AEPS Application

Future trends for AEPS applications focus on enhanced security through AI and biometrics, deeper integration with platforms like UPI and digital wallets, and an expansion of services beyond basic banking to include micro-loans and insurance. Other key trends include the use of blockchain technology for transparency, a mobile-first user experience for better accessibility, and stricter RBI regulations.

Key future trends for AEPS applications

Enhanced Security:

- Utilizing Artificial Intelligence (AI) and Machine Learning (ML) for real-time fraud detection and risk management.

- Implementing more advanced biometric and eKYC methods for faster and more secure user verification.

Deeper Integration:

- Integrating seamlessly with other digital payment platforms like UPI, Bharat Bill Pay (BBPS), and digital wallets to create a unified financial ecosystem.

- Expanding through embedded finance, making financial services accessible within non-financial applications.

Expanded Service Offerings:

- Moving beyond core banking functions to include a wider range of services like micro-loans, insurance, bill payments, and mobile recharges.

Improved User Experience:

- Prioritizing mobile-first design and more intuitive, user-friendly interfaces for easier adoption, especially in rural areas.

Increased Transparency and Efficiency:

- Adopting blockchain technology to increase transparency and security in transactions.

- Focusing on real-time settlement for faster and more efficient processing.

Regulatory Compliance:

- Adhering to new and stricter security controls mandated by the RBI.

Broader Reach:

- Continuing to expand AEPS services into more rural and underbanked areas to further financial inclusion.

Conclusion

The AEPS Application has become one of the most powerful tools for retailers, distributors, and growing businesses who want to offer fast, secure, and convenient digital financial services. With AEPS, you can easily provide cash withdrawal, balance inquiry, mini statements, and Aadhaar-based banking services to customers even in areas where banking access is limited. This not only improves customer trust but also helps retailers earn a steady income every day.

An AEPS application is a mobile or web-based interface that uses the Aadhaar Enabled Payment System to allow users to perform basic banking transactions like cash withdrawal, deposit, fund transfer, and balance inquiry through biometric authentication. These applications, often used by Business Correspondents, enable a bank-led model for financial transactions at micro-ATMs and other AEPS touchpoints, promoting financial inclusion, especially in rural areas.

For any business looking to start or scale a digital financial service, Aeps India is a reliable AEPS software provider is the most important step. A trusted company like Aeps India ensures high uptime, fast transaction speed, strong security, real-time reporting, and easy integration. Their AEPS solutions are designed to help retailers grow faster, earn more, and deliver better service in their local market.

By using a professional AEPS application, you can build your fintech business with confidence, attract more customers, and increase your monthly income. AEPS is not just a service it is a long-term business opportunity for anyone who wants to join India’s digital banking revolution.

Start your AEPS business today with the right partner and move one step closer to secure income, strong growth, and a successful fintech journey.

Frequently Asked Questions (FAQs)

An AEPS application is a digital platform that allows retailers and businesses to offer banking services like cash withdrawal, balance enquiry, mini statement, and Aadhaar-based payments using Aadhaar authentication.

Retailers earn a commission on every AEPS transaction. The more customers use services like withdrawal or balance enquiry, the more daily income retailers generate.

Yes. AEPS is fully secure because it works on UIDAI authentication, Aadhaar verification, and bank-approved systems. This makes every transaction safe and encrypted.

You only need:

A smartphone or computer

A biometric device

A stable internet connection

AEPS login from a trusted provider like Aeps India

Using the AEPS app, you can provide:

Cash Withdrawal

Balance Enquiry

Mini Statement

Aadhaar Pay

Fund Transfer

Aeps India offers a fast, secure, and high-success AEPS solution with real-time support, smooth settlement, and an easy Aeps dashboard designed for retailers and distributors.

Yes. With AEPS b2b software or best Aadhaar Enabled Payment System API from Aeps India, you can easily start your own AEPS business, add retailers, and grow as a distributor or super distributor.

Retailers don’t need special approval. However, using AEPS through a certified Aeps India ensures compliance with NPCI and UIDAI standards.

You can use any NPCI-approved biometric device such as Mantra, Morpho, Startek, Tatvik, etc.

AEPS transactions are instant, and settlement with on Aeps India. Aeps India offers fast response, real-time data, and high uptime.

Yes, AEPS designed for all locations, even with low internet connectivity. It works smoothly across rural India.

Yes. AEPS services are active 24/7, allowing retailers to offer banking support anytime.

The best commission provide Aeps India, but with Aeps India, retailers earn competitive commissions on every successful transaction.

Yes. With AEPS, customers can withdraw cash using only their Aadhaar number and fingerprint, no card or PIN required.

Yes. AEPS is extremely convenient for rural customers who may not have access to nearby banks or ATMs. It makes banking simple, fast, and accessible.

Best AePS Cash Withdrawal API Provider in India

AEPS Service API – A Complete Guide for Businesses