UPI Cash Point – UPI Cash Withdrawal & Cash Out Solution

A UPI Cash Point is a modern digital banking solution that allows retailers and merchants to provide instant cash withdrawal services using UPI-enabled transactions. As digital payments continue to grow across India, UPI Cash Point services are creating new income opportunities for retailers while giving customers quick and convenient access to cash without visiting a bank or ATM.

With a reliable UPI Cash Point Solution, retailers can serve more customers, increase daily footfall, and earn commissions on every successful cash withdrawal transaction. The service is simple, secure, and designed to support both urban and rural users who need easy access to banking services.

A UPI Cash Point is an NPCI-backed system that allows you to withdraw cash directly from nearby authorized retail shops, Kirana stores, or Bank Mitra (Business Correspondent) outlets. Instead of visiting a bank or ATM, the retailer generates a dynamic QR code on their app. You scan it with your preferred UPI app, authenticate the payment with your UPI PIN, and the retailer hands you the physical cash.

AEPS India provides a secure and easy-to-use UPI Cash Point platform with fast transaction processing, real-time settlements, high success rates, and a user-friendly interface. Whether you are a retailer, distributor, CSP, or fintech business, UPI Cash Point can help you expand your service portfolio and grow your monthly income.

In this guide, you will learn everything about What is UPI Cash Point, including how UPI Cash Point works, its benefits, eligibility, business opportunities, earning potential, and why it is becoming one of the fastest-growing digital banking services in India.

What Is a UPI Cash Point?

A UPI Cash Point is a service that allows you to withdraw physical cash at authorized local merchant shops (like Kirana or medical stores) using your smartphone. Instead of visiting a bank or ATM, you simply scan a shopkeeper’s UPI QR code, authorize the transaction via your UPI PIN, and they hand you the cash directly.

This service is also known as UPI CashPoint, UPI Cashout, QR ATM, or UPI-based cash withdrawal. It is powered by NPCI (National Payments Corporation of India) the same organisation that built UPI, IMPS, and the entire digital payment infrastructure of India.

How Does a UPI Cash Point Work?

A UPI Cash Point functions similarly to a digital ATM or a human-operated point-of-sale terminal. It allows customers to walk into authorized local retail shops (kirana stores, mobile shops, etc.) to withdraw cash using their UPI apps (like Google Pay or Paytm).

How it Works

- Initiate Request: Visit an authorized local merchant or Business Correspondent (BC) and tell them the amount of cash you need.

- Generate QR Code: The shopkeeper enters the requested amount into their partner app, which generates a unique, dynamic QR code.

- Scan: Open your preferred UPI app (e.g., Google Pay, PhonePe, Paytm) and scan the merchant’s QR code.

- Authorize: Verify the amount on your phone screen and enter your secure UPI PIN.

- Collect Cash: Once the payment is successful, the merchant directly hands over the physical cash to you.

- Earn Commission: The agent earns a commission from the Aeps india for facilitating the transaction.

Services Offered at a UPI Cash Point

A UPI Cash Point lets users withdraw cash directly from their bank accounts at local retailer shops or merchant outlets without needing a physical debit card. Customers simply scan the merchant’s QR code, authorize the transaction via their UPI app, and instantly receive physical cash.

These merchant-operated locations typically offer the following features and benefits:

- Cash Withdrawal: Customers can instantly withdraw cash by scanning a QR code at Bank Mitra or Business Correspondent outlets.

- Interoperability: The service is compatible with all leading UPI applications, including Paytm, Google Pay, and Paytm, regardless of the user’s banking partner.

- Secure Authentication: Transactions are secured by instant digital authorization and the user’s standard UPI PIN.

- Wider Accessibility: Brings banking services to locations where traditional ATMs or bank branches are unavailable or have run out of cash.

For retailers and business owners looking to provide these services (often powered by platforms like Aeps india), it also serves as an avenue to increase footfall and earn extra income.

Key details of the service include:

- Transaction Limits: You can generally withdraw up to ₹5,000 per transaction, with a daily limit of ₹10,000 and a monthly limit of ₹50,000.

- Frequency: Withdrawals are restricted to a maximum of 2 transactions per day, with a mandatory 30-minute cooling-off period between transactions.

- Retailer Integration: This system runs through fintech operators like Aeps india, turning local neighborhood stores into assisted cash-out points.

You can access these cash points at local partner retail stores in your area using any of your standard UPI applications like Google Pay or Paytm.

Eligibility to Become a UPI Cash Point

To become a UPI Cash Point, you must be an authorized retailer or Business Correspondent (BC) operating a local shop or service outlet.

Eligibility Requirements:

- Retailer Account: You must register with an authorized Aeps india.

- Valid Documents: You need to provide valid identity and address proofs, plus your bank account details for settlements.

- Working Capital: You must have enough physical cash on hand to give to customers when they request withdrawals.

- No Biometrics Required: You do not need a biometric device. Customers will simply scan your generated QR code.

Documents Required for Registration UPI Cash Point

To register as a UPI Cash Point and provide cash withdrawal services, retailers need specific business documents for verification.

| Required Document | Purpose / Description |

|---|---|

| Aadhaar Card | Valid proof of identity. Aadhaar should be linked with your registered mobile number for OTP-based verification and eKYC. |

| PAN Card | Required as proof of tax identity and for regulatory compliance during registration. |

| Bank Account Details | A recent bank passbook, cancelled cheque, or bank statement is required for settlement, commission payouts, and account verification. |

| Shop Proof | Shop Establishment Certificate, Trade License, GST Certificate (if applicable), or a valid Rental/Lease Agreement to verify your business location. |

| Passport Size Photograph | A recent, clear, passport-size color photograph for profile verification and onboarding. |

| Registered Mobile Number | An active mobile number linked with both your Aadhaar and bank account for OTP verification, transaction alerts, and account security. |

For full platform-specific document submission instructions, visit a retailer onboarding portal like Aeps india.

Who Can Use UPI Cash Point

Any user with a smartphone, an active bank account, and a UPI app (like Google Pay or Paytm) can use a UPI Cash Point. You can withdraw cash at authorized local retail stores or UPI-enabled ATMs by scanning a QR code and authorizing the transaction using your UPI PIN.

Who can use it:

| Business Type | Why UPI Cash Point is a Good Fit |

|---|---|

| Kirana and grocery stores | Customers often need cash while shopping, making it easy to offer cash withdrawal services along with daily essentials. |

| Mobile phone shops and repair centres | These businesses already have trusted local customers, making UPI Cash Point services a natural addition. |

| CSC (Common Service Centre) operators | Since they already provide government and digital services, adding UPI Cash Point can increase customer convenience and income. |

| Bank Mitras and Banking Correspondents (BCs) | They can expand their banking services by offering UPI-based cash withdrawal to more customers. |

| Medical stores and pharmacies | With a steady flow of daily visitors, these shops have excellent potential for frequent cash withdrawal transactions. |

| Petrol pumps | Many customers need cash while travelling or refuelling, making petrol stations a convenient cash access point. |

| Stationery shops near schools and colleges | Students regularly use UPI for payments, creating a good opportunity to provide UPI Cash Point services. |

| Tailors, hardware shops, and local retail stores | Any shop with regular and loyal customers can easily increase footfall and earn extra income by offering UPI Cash Point services. |

Why Use UPI Cash Point

UPI Cash Point lets you get cash without a physical debit card by scanning a QR code at a participating ATM or a local store.

Here is why you should use it:

- No Card Needed: You do not need to carry a physical debit card. This removes the risk of card theft or losing your card.

- Better Safety: You authorize the cash using your private UPI PIN on your phone. This lowers the chance of digital card fraud.

- Easy Access: You can get cash from any UPI-enabled ATM or participating merchant near you.

- Multi-Account: You can pick which linked bank account to take money from using a single app.

Where to USE it UPI Cash Point

Use a UPI Cash Point in two main places:

1. Local Retail Shops (Bank Mitras)

Use participating local stores, like, grocery shops or mobile recharge stores, to withdraw cash without an ATM.

How: The shopkeeper enters the amount on their partner app. You scan their QR code and pay via any UPI app. The shopkeeper hands you the physical cash.

2. UPI-Enabled ATMs

Use compatible ATMs to withdraw cash without a debit card.

How: Select “UPI Cash Withdrawal” on the ATM screen. Enter your desired amount. Scan the dynamic QR code on the screen with your smartphone and enter your UPI PIN to authorize.

Top Use Cases of UPI Cash Point

UPI Cash Point enables users to instantly withdraw or deposit cash at local shops or micro-ATMs without physical debit cards.

- Cardless ATM Withdrawals: HDFC Bank and other National Financial Switch (NFS) networks allow users to scan dynamic QR codes on ATM screens to receive physical cash without carrying a debit card.

- Neighborhood Cash-Outs: Customers visit authorized Business Correspondents or Bank Mitras in rural or remote locations. Users scan the local agent’s QR code via a smartphone and immediately receive physical cash.

- Emergency Cash Access: Users without a nearby bank branch or ATM can obtain cash at thousands of participating local grocery shops, pharmacies, and small merchant outlets.

- Assisted Cash Deposits: Users without smartphone access hand physical cash to authorized local agents. The agents use UPI Cash Point integrations to credit the exact amount directly into the user’s linked bank account.

Do’s While Using UPI Cash Point

Follow these rules for a safe UPI Cash Point transaction:

- Verify the QR code: Only scan the dynamic QR code displayed on the official ATM or agent screen.

- Keep your UPI PIN private: Never share your UPI PIN or enter it anywhere except your own private mobile app.

- Check the amount: Confirm the cash amount on your screen matches the amount you requested before paying.

- Wait for confirmation: Only collect your physical cash after your UPI app shows a successful payment message.

- Review transaction history: Check your banking notifications to confirm the exact deducted amount.

Why Is UPI Cash Withdrawal Important for India in 2026?

UPI cash withdrawal is important in 2026 because it provides cardless access to cash, eliminates the need to carry physical debit cards, and protects users from card skimming and cloning. It ensures immediate liquidity for consumers without requiring plastic cards, making emergency cash retrieval faster and more secure.

India has more than 500 million active UPI users, but many people still live in areas where ATMs are far away or often run out of cash. With UPI Cash Withdrawal, your shop can become a convenient cash access point for your local community. Customers can withdraw cash easily using UPI, and you earn a commission on every successful transaction.

Key Benefits and Rules for 2026:

- Security: Withdrawals are authorized by scanning a dynamic QR code on the ATM screen and entering your UPI PIN.

- Convenience: You do not need to carry a debit or credit card to access your funds.

- Bank Fees: Major banks like HDFC Bank and Punjab National Bank now count UPI ATM withdrawals within your standard monthly free ATM transaction limits.

- Charges: Once your free monthly quota is crossed, transactions typically attract a fee of about ₹23 to ₹27 (inclusive of taxes) per withdrawal.

You can easily use this service by selecting “UPI Withdrawal” on a supported machine and scanning the code with any UPI app on your smartphone.

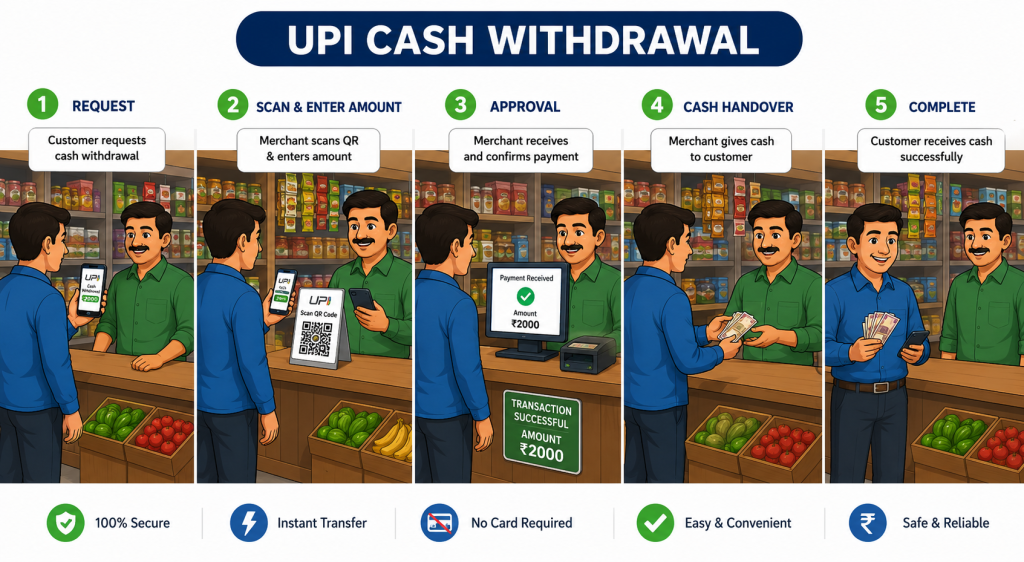

How to Withdraw Cash Using UPI Cash Point?

Withdraw cash from a UPI Cash Point (like a Bank Mitra or merchant outlet) by scanning the agent’s QR code. Inform the agent of the cash amount, scan the QR code via your UPI app (e.g., Google Pay, Paytm), and authorize the payment with your UPI PIN.

Follow these steps to complete the transaction:

- Tell the Agent: Inform the UPI Cash Point agent of the cash amount needed.

- Scan the QR Code: Open your UPI application on your smartphone and scan the agent’s unique UPI QR code.

- Verify Amount: Check the cash amount on your mobile screen.

- Enter UPI PIN: Enter your secure 4 or 6-digit UPI PIN to authorize the payment.

- Collect Cash: The agent will hand over your physical cash once the successful payment notification appears.

Why Retailers Choose UPI Cash Withdrawal Service

Retailers choose to offer UPI cash withdrawal services to increase daily foot traffic, earn direct commissions on transactions, and boost in-store sales. By acting as a local “human ATM,” merchants enhance customer engagement and encourage patrons who come for cash to also purchase everyday goods and services.

This service benefits local store owners across several key areas:

- Footfall and Cross-Selling: Operating as a UPI Cash Point guarantees increased visibility. Customers drawn to the store for cash withdrawals often stay to purchase groceries, apparel, or other products, directly increasing revenue.

- Direct Commissions: Retailers earn a fixed commission or percentage on every successful cash withdrawal they process, creating a supplementary stream of income alongside their regular business margins.

- Reduced Cash Management Costs: It provides a secure, digital method for retailers to manage and deposit surplus cash from their daily registers, saving them from the logistics and security risks of physically depositing money at a bank.

- Enhanced Customer Retention: Offering the ability to withdraw cash without searching for a traditional ATM builds customer loyalty. Shoppers prefer the convenience of neighborhood stores over travelling to distant bank ATMs.

- Minimal Hardware Requirements: Unlike traditional POS machines that require cards, maintaining a UPI cash service requires no extra hardware. Retailers can use existing business-oriented fintech applications to generate dynamic QR codes.

Perfect Business Opportunity for Retailers UPI Cash Point

A UPI Cash Point lets retailers turn their shop into a digital ATM. Customers scan the retailer’s QR code via apps like Paytm or Google Pay to withdraw physical cash. Retailers earn a direct commission (up to ₹8–₹14) on every successful transaction while increasing store visits.

Key Benefits

- Zero Device Cost: Retailers do not need expensive hardware. Transactions are managed entirely through smartphone apps.

- New Income Stream: Retailers earn an instant commission for dispensing cash from their shop’s register.

- More Customers: People visiting to withdraw cash often buy goods, which grows overall sales.

- Safe and Fast: Transactions use standard UPI security and settle instantly into the retailer’s bank wallet.

Why Customers Prefer UPI Cash Withdrawal

Customers prefer UPI cash withdrawals because they eliminate the need to carry physical debit cards, reducing the risk of card skimming and theft. This method allows for instant transactions at ATMs by simply scanning a dynamic QR code and authorizing the release of cash via a mobile UPI app.

Here are the key reasons customers prefer this method:

- Cardless Convenience: Users do not need to carry physical cards or worry about losing them.

- Enhanced Security: Transactions are authorized with a secure mobile UPI PIN, reducing the risk of card fraud.

- Multiple Account Access: Customers can easily withdraw funds from different bank accounts linked to a single UPI app.

- Speed: The transaction is fast and straightforward, requiring only a quick scan and pin entry.

Currently Active UPI & Bank Apps

UPI Cash Point lets users withdraw cash at local shops using their smartphone. You can use any major UPI app to scan a retailer’s QR code and get physical cash.

Active UPI and bank apps supporting this service include:

- Paytm

- Google Pay

- BHIM UPI

- Navi

- PayNearby (Saathi)

- Kotak 811

- HDFC PayZapp

- CRED

- BHIM UPI (iOS)

- Bhim

- SBI YONO

- INDmoney

- YES Bank IRIS

- Jio Finance

- YES Pay Next

- Popclub

- HDFC Bank App

- Freecharge

- HDFC Bank App (iOS)

- Groww (iOS)

- Axis Mobile (iOS)

Supported Banks for UPI Cash Point

Major banks supporting UPI-based ATM cash withdrawals and cash point services include Bank of Baroda, ICICI Bank, HDFC Bank, Axis Bank, Yes Bank, IndusInd Bank, and Punjab National Bank.

- Kotak Mahindra Bank

- ICICI Bank

- State Bank of India

- Union Bank Of India

- Bank of Baroda

- AIRTEL PAYMENTS BANK LIMITED

- HDFC

- Punjab national Bank

- Indusind Bank

- Axis Bank

- AU SMALL FINANCE BANK

- YES BANK LIMITED YBS

- IDBI Bank

- Baroda Gujarat Gramin Bank

- IDFC First Bank Ltd

- Federal Bank

- PUNJAB GRAMIN BANK

- Karnataka Bank

- Bandhan Bank limited

- ASSAM GRAMIN VIKASH BANK

- City Union Bank

- Central Bank of India

- Standard Chartered Bank

- HSBC Bank

Benefits of UPI Cash Point

UPI Cash Points let users withdraw physical cash at local shops using a UPI app. This removes the need to carry a debit card or find an ATM. Users scan a QR code and authorize the payment via their UPI PIN to instantly receive cash.

Benefits for Customers

- Card-Free Withdrawals: Customers get cash using just a smartphone and any UPI app (like Paytm or Google Pay).

- No ATM Lines: It is often faster to visit a local shop than to drive to a bank ATM.

- Accessibility: Customers can get money in remote areas with few ATMs.

Benefits for Shop Owners

- Extra Income: Shop owners earn a commission (up to ₹10) from Aeps india on every successful cash withdrawal.

- More Customers: Offering cash services increases foot traffic, which can boost sales for the store.

- No Equipment Needed: Shops do not need to buy or maintain expensive card machines to offer this service.

Features UPI Cash Point

UPI Cash Point allows you to withdraw cash at local shops and banking agents (Bank Mitras) without a debit card or ATM.

Key features include:

- Scan and Go: You scan a dynamic QR code generated by the agent’s app using any UPI app (like Google Pay or Paytm).

- No ATM Needed: Cash is handed to you instantly by the agent after your payment is approved.

- Limits: Transactions are usually capped at ₹5,000 per transaction and ₹10,000 per day.

- Wide Compatibility: The system supports over 200 banks and does not require special hardware.

- Agent Rewards: Shop owners and agents earn a small commission on every transaction.

How to Activate UPI Cash Point Service?

A UPI Cash Point lets retail shop owners give cash to customers from their store’s cash drawer. The customer sends money to the shop owner using a UPI app, and the owner hands the customer the cash in person.

Setup and Transaction Process

- Download an App: Install a banking or retail service app that supports UPI Cash Point services (such as Aeps india).

- Complete KYC: Register your shop details and verify your identity in the app.

- Enter Amount: Open the cash point section in your app and enter the amount the customer wants to withdraw.

- Generate QR Code: The app creates a unique digital QR code for that exact amount.

- Scan and Pay: The customer scans the QR code with their own UPI app and enters their UPI PIN.

- Hand Over Cash: Check your app for a successful payment message, then give the physical cash to the customer.

Example:

UPI Cash Withdrawal Commission Opportunities

Direct UPI cash withdrawals at ATMs carry zero direct commission or fees for users. However, the existing ATM transaction limits apply. If you use Aadhaar-enabled Payment Systems (AEPS) via local agents or banking correspondents, agents earn a fixed commission structure ranging from ₹2 to ₹15+ per transaction.

Direct UPI ATM Withdrawals

- User Fees: Nil. The National Payments Corporation of India (NPCI) levies zero charges for UPI ATM transactions.

- Bank Fees: Standard ATM rules apply. Transactions exceeding your monthly free limit will incur fees set by your issuing bank, typically around ₹21 plus applicable taxes.

- Limits: You can usually withdraw up to ₹10,000 per transaction, subject to your daily UPI limits.

AEPS Cash Withdrawal Commission Structure (For Agents)

If you are withdrawing cash through a local retailer using biometrics, the retailer earns a tiered commission from the Aeps india based on the withdrawal amount:

| Withdrawal Amount | Commission Rate | Your Earning | Credited To |

| ₹100 – ₹999 | Fixed / Per txn | ₹2 – ₹5 | Wallet — Instant |

| ₹1,000 – ₹2,499 | Fixed / Per txn | ₹5 – ₹8 | Wallet — Instant |

| ₹2,500 – ₹10,000 | Fixed / Per txn | Up to ₹10 | Wallet — Instant |

| Volume Bonus (150+ txns/month) | Extra bonus | ₹500 – ₹2,000 | Wallet — Monthly |

Monthly Income Example — Active UPI Cash Withdrawal Retailer

| Scenario | Daily Transactions | Avg Commission/Txn | Monthly Income |

| Small kirana store | 20 transactions/day | ₹5 | ₹3,000/month |

| Active CSC / mobile shop | 50 transactions/day | ₹7 | ₹10,500/month |

| High-volume UPI agent | 100 transactions/day | ₹8 | ₹24,000/month |

Retailer Commission on UPI Cash Point

One of the key benefits of becoming a UPI Cash Point retailer is the opportunity to generate extra monthly income by providing cash withdrawal services to customers. Every successful eligible transaction can help you earn commission, making it a valuable addition to your existing business.

| Retailer Category | Commission |

|---|---|

| Normal Retailer | Earn up to ₹8 on eligible transactions above ₹3,000 |

| Prime Retailer | Earn up to ₹10 on eligible transactions above ₹3,000 |

| Super Prime Retailer | Earn ₹10–₹12 per eligible transaction above ₹3,000 |

Please Note: The commission you receive may vary depending on factors such as your retailer category, monthly transaction volume, company policies, and any ongoing promotional offers.

Terms & Conditions Apply.

UPI Cash Withdrawal Earnings Structure

A UPI cash withdrawal does not generate direct earnings for the customer. Instead, it is a service that costs the user standard ATM fees. These withdrawals count toward your bank’s monthly free ATM transaction limit.

Key Fees and Limits

- Free Limit: You get 3 to 5 free ATM transactions per month, depending on your city and bank type.

- Per Transaction Fee: After you pass your free limit, banks charge about ₹23 plus taxes for each withdrawal.

- Transaction Limit: You can withdraw up to ₹10,000 per transaction.

- Daily Limit: Your daily withdrawal depends on your bank’s limits and standard UPI limits.

Important Rules to Follow UPI Cash Point

- Never share your UPI PIN: Treat your PIN like your debit card PIN. Never share it with anyone or approve unknown payment requests.

- Scan at the outlet: Do not send or accept a screenshot of a Dynamic QR code. Always generate and scan the QR code live at the ATM or Cash Point.

- Observe transaction limits: The limit is ₹10,000 per transaction. Cash withdrawals also count toward your standard daily UPI limits and ATM transaction caps.

- Maintain transaction records: If you are a retailer, you must log customer details, mobile numbers, amounts, RRN (Retrieval Reference Number), and signatures in a register.

UPI CashPoint Withdrawal Limits

The maximum cash you can withdraw using UPI at ATMs is ₹10,000 per transaction.

The overall daily limit is ₹1,000,000 per day. However, your actual daily limit depends on your bank’s specific rules and your standard daily UPI transfer limit.

- MicroATMs: Withdrawals at local agent or merchant locations have a lower limit of ₹5,000 per transaction and ₹10,000 per day.

- Transaction Fees: These transactions usually count towards your bank’s regular monthly free ATM transaction limit. Exceeding this limit will result in standard ATM fees.

- Availability: This service requires a UPI app enabled for UPI-ATM transactions. UPI Lite accounts are not supported.

Transaction Limits & Rules

To prevent misuse, UPI Cash withdrawals at retail points are structured for routing everyday usage:

- Per Transaction Limit: Up to ₹5,000

- Daily Limit: Up to ₹10,000

- Monthly Limit: Up to ₹50,000

- Frequency: Maximum of 2 transactions per day, with a 30-minute cooling period between each transaction [1, 2]

| PARAMETER | LIMIT / CONDITION |

| Transactions per Customer per Bank | Maximum 2 transactions |

| Per Transaction Limit | Minimum ₹100 – Maximum ₹5,000 |

| Per Day Transaction Limit | ₹10,000 |

| Monthly Limit per Bank | ₹50,000 |

| Cooling Period (between two transactions same Account) | 30 Minutes |

| Dynamic QR Validity | Expires in 45 Seconds |

Tips to Maximise Your UPI Cash Withdrawal Income Every Month

To maximize your income through UPI transactions, focus on earning rewards and avoiding fees rather than cash withdrawals, as withdrawing cash directly does not generate income.

1. Use UPI on RuPay Credit Cards

- Link a RuPay Credit Card to your UPI app.

- Pay for daily merchant expenses using this method to earn assured cashback (often 1% to 5%).

- Track the monthly transaction cap for each card (typically ₹200 to ₹500) and switch to another card once you hit it.

2. Use Dedicated Cashback UPI Apps

- Download and use rewards-focused Aeps india provide apps for your daily payments.

- Ensure you only scan business (merchant) QR codes, as personal transfers rarely offer rewards.

3. Avoid ATM Withdrawal Fees

- Banks including HDFC and others now count UPI-based ATM cash withdrawals toward your standard monthly free ATM transaction limit.

- Exceeding this quota results in a fee of ₹23 plus taxes per transaction.

- Avoid these charges by withdrawing cash only from your own bank’s ATM and limiting the total number of times you withdraw cash per month.

4. Route Utility and Bill Payments

- Use your linked UPI credit cards to pay recurring bills like electricity, water, and broadband.

- This builds higher transaction volumes and consistently captures the maximum available monthly reward points.

UPI Cash Withdrawal vs AEPS — What Is the Difference?

One of the most common questions retailers ask is whether they should choose UPI Cash Withdrawal, AEPS, or offer both. Let’s compare them in simple terms.

| Feature | UPI Cash Withdrawal | AEPS Cash Withdrawal |

| Authentication | Customer’s UPI PIN on their phone | Aadhaar number + fingerprint |

| Hardware needed | Your smartphone only | Smartphone + biometric scanner (₹1,500–₹3,000) |

| Customer requirement | Active UPI app on smartphone | Aadhaar-linked bank account + working fingerprint |

| Per transaction limit | Up to ₹5,000 | Up to ₹10,000 |

| Serves elderly/rural customers | Limited — needs smartphone | Yes — works for all Aadhaar holders |

| Commission per transaction | Up to ₹10 | Up to ₹15 (super prime tier) |

| Best for | Urban / semi-urban customers with smartphones | Rural customers, Jan Dhan beneficiaries, elderly |

Expert Recommendation: Aeps india offer BOTH services. UPI Cash Withdrawal serves your smartphone-savvy customers; AEPS serves your Aadhaar-linked rural customers. Together they cover 100% of your market. Aeps india all-in-one platform lets you offer both from the same login, same wallet, same app.

Why Aeps india Is India’s Best UPI Cash Withdrawal Platform

| Feature | Aeps india | Other Providers |

|---|---|---|

| Commission per transaction | Up to ₹10 per transaction | ₹3 – ₹7 (lower rates) |

| Settlement speed | T+0 — Same Day | T+1 or T+2 |

| Platform uptime | 99.9% — 24/7/365 | Varies — downtime reported |

| Technical support | 24/7 — Sundays & Holidays | Business hours only (most) |

| Multi-service platform | UPI Cash + AEPS + BBPS + DMT + Recharge | Limited to 1–2 services |

| White label / own brand | Available — launch your own brand | Not offered |

| Registration fee | Free for individual agents | Fee charged by some providers |

Why Choose Aeps india UPI Cash Point?

Key Benefits

- Withdraw cash instantly using UPI without any complicated process.

- Enjoy secure QR code-based transactions with advanced payment security.

- Earn extra income by offering UPI Cash Point services to your customers.

- Easy-to-use interface that is simple for both retailers and customers.

- Receive fast wallet settlements for smooth and hassle-free business operations.

- Access multiple bank support through a single integrated platform.

- Works seamlessly with popular UPI apps like Paytm, Google Pay, Paytm, BHIM, and other supported apps.

- Perfect for both rural and urban locations, helping businesses serve more customers with ease.

Conclusion

A UPI Cash Point is becoming one of the fastest-growing digital banking services for retailers, CSPs, and fintech businesses in India. It allows customers to withdraw cash using UPI while helping retailers earn additional commission and increase daily customer footfall.

By choosing a reliable UPI Cash Point Solution, businesses can offer secure cash withdrawal services, real-time transactions, fast settlements, and a simple customer experience. It is an excellent opportunity for retailers to expand their digital banking services without requiring customers to visit an ATM or bank branch.

A UPI Cash Point is an NPCI-backed system that allows you to withdraw cash directly from authorized retail shops, Kirana stores, or Banking Correspondents (Bank Mitras) without needing an ATM or debit card. You simply scan a store’s dynamic QR code using your UPI app, authorize the payment, and the retailer hands you the cash.

AEPS India provides a secure and scalable UPI Cash Point Solution with easy integration, high transaction success rates, advanced security, and dedicated technical support. Whether you are starting a new digital banking business or expanding your existing services, our platform helps you grow with confidence.

Get started with AEPS India today and launch your UPI Cash Point service to increase customer satisfaction, generate higher monthly income, and grow your digital banking business.

using UPI – No Card Needed!

Transaction

Secure

Required

Frequently Asked Questions — UPI Cash Withdrawal

A UPI CashPoint is an NPCI-backed system that allows you to withdraw cash directly from authorized retail shops, Kirana stores, or Bank Mitra outlets, functioning like a human ATM. Instead of visiting a bank, you scan the retailer’s dynamic QR code via a UPI app (like PhonePe or Google Pay), authorize the payment, and the retailer gives you the physical cash.

UPI CashPoint (also known as UPI Cash Withdrawal or QR ATM) allows you to withdraw physical cash at authorized local merchant shops (like kirana or medical stores) or designated UPI-enabled ATMs using your smartphone, entirely bypassing the need for a physical debit card.

Retail shops, Kirana stores, CSC centers, mobile recharge shops, distributors, fintech companies, supermarkets, and entrepreneurs can start a UPI Cash Point business after completing the required registration and KYC process.

UPI Cash Point offers instant cash withdrawal, secure QR-based transactions, fast wallet settlement, multiple bank support, compatibility with major UPI apps, and an additional source of income for retailers while providing convenient banking services to customers.

Yes. Every transaction is processed through the UPI network using encrypted payment technology and customer authentication. Since payments are completed through trusted UPI apps, the process is secure and transparent.

Most leading UPI applications are supported, including Paytm, Google Pay, Paytm, BHIM UPI, MyJio, Freecharge, and other UPI-enabled banking apps, based on the Aeps india.

Retailer earnings depend on transaction volume, commission structure policies. Businesses with regular customer traffic can generate an additional monthly income by offering UPI Cash Point services alongside other digital payment services.

No. In most cases, a smartphone with internet connectivity and a QR code is sufficient. Aeps india may also offer dedicated software or merchant applications for better transaction management.

Yes. Many fintech platforms allow retailers to offer both UPI Cash Point and AEPS services from a single dashboard, helping businesses provide multiple digital banking services from one platform.

Yes. UPI Cash Point services can be offered in both rural and urban areas, making digital cash withdrawal more accessible for customers throughout India.

After successful KYC verification and document approval, activation is generally completed within a few business days, depending on the Aeps india onboarding process.

Yes. Businesses with their own website, mobile application, or fintech platform can integrate UPI Cash Point APIs to offer QR-based cash withdrawal services to their customers.

Yes. Most UPI Cash Point platforms support transactions from multiple participating banks through the UPI ecosystem, making the service convenient for a wide range of customers.

Yes. Retailers get access to a dashboard where they can monitor cash withdrawals, transaction history, settlements, wallet balance, and reports in real time.

Wallet settlement is the process of transferring the retailer’s commission or transaction amount to their merchant wallet or linked bank account according to the settlement policy.

Transaction limits depend on the customer’s bank, the UPI application, regulatory guidelines, and the policies. The applicable limit may vary from one transaction to another.

Offering UPI Cash Point helps retailers attract more customers, increase daily footfall, generate additional income, expand digital banking services, and improve customer convenience without investing in expensive infrastructure.

Yes. We provide a free live demo so businesses can explore the dashboard, understand the transaction process, review settlement features, and evaluate the platform before making a decision.